The latest excessive fee suit targets “wildly excessive compensation,” an allegedly imprudent stable value offering, and the unmonitored use of “float” income.

More specifically, the participant-plaintiffs of Miami, Florida-based Lennar Corp. are raising issues with the recordkeeping/administrative fees (“wildly excessive compensation”) paid by the plan, the prudence of retaining Prudential’s stable value fund, and the use of float income by Prudential (the plan’s recordkeeper).

The lawsuit, filed in the U.S. District Court for the Southern District of Florida (Catenac v. Lennar Corp., S.D. Fla., No. 1:22-cv-23232, complaint 10/5/22), is directed at a plan with approximately $1.2 billion in assets and nearly 13,000 participants. The participant-plaintiffs are represented here by Morgan & Morgan PA.

Meanwhile, in Congress the Retirement Savings Modernization Act was just introduced to allow cryptocurrency and just about anything short of lottery tickets into America’s 401(k) accounts. The alternative asset industry — private equity, hedge funds, venture capital, real estate, and more — has been trying for years to offer their speculative products — and reap huge fees in the process — through personal retirement accounts as they are already able to do in some public pensions, such as Ohio’s.

There has been no legal barrier to these investments, and the Trump administration’s Department of Labor went so far as to specify that alternative investments could be part of 401(k)s, a decision affirmed by the Biden Administration. But companies administering 401(k) accounts are fiduciaries, and they’ve avoided alternative investments in fear of getting sued for breach of fiduciary duty for offering them to workers. For decades, prudence has prevailed and 401(k) retirement accounts have not allowed high-fee, illiquid funds as a 401(k) option.

The proposed bill simply states that alternative investments, despite the higher fees associated with them, are “covered” investments that do not establish fiduciary breach by their presence in a 401(k) plan. The cloak of congressionally created cover for alternative investments is needed because the current commonsense assumption is that the mere presence of these investments is strong evidence fiduciary duty has been breached.

Although employer-provided retirement plans are a relatively recent phenomenon in the private sector, dating from the late nineteenth century, public sector plans go back much further in history. From the Roman Empire to the rise of the early-modern nation state, rulers and legislatures have provided pensions for the workers who administered public programs. Military pensions, in particular, have a long history, and they have often been used as a key element to attract, retain, and motivate military personnel. In the United States, pensions for disabled and retired military personnel predate the signing of the U.S. Constitution.

Like military pensions, pensions for loyal civil servants date back centuries. Prior to the nineteenth century, however, these pensions were typically handed out on a case-by-case basis; except for the military, there were few if any retirement plans or systems with well-defined rules for qualification, contributions, funding, and so forth. Most European countries maintained some type of formal pension system for their public sector workers by the late nineteenth century. Although a few U.S. municipalities offered plans prior to 1900, most public sector workers were not offered pensions until the first decades of the twentieth century. Teachers, firefighters, and police officers were typically the first non-military workers to receive a retirement plan as part of their compensation.

By 1930, pension coverage in the public sector was relatively widespread in the United States, with all federal workers being covered by a pension and an increasing share of state and local employees included in pension plans. In contrast, pension coverage in the private sector during the first three decades of the twentieth century remained very low, perhaps as low as 10 to 12 percent of the labor force (Clark, Craig, and Wilson 2003). Even today, pension coverage is much higher in the public sector than it is in the private sector. Over 90 percent of public sector workers are covered by an employer-provided pension plan, whereas only about half of the private sector work force is covered (Employee Benefit Research Institute 1997).

Author(s): Lee A. Craig, North Carolina State University

Publication Date: 16 March 2003, accessed 8 Oct 2022

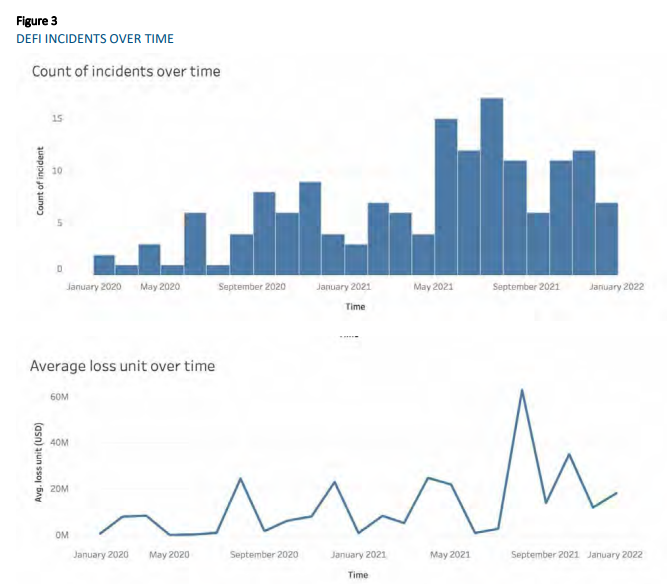

Decentralized finance (DeFi) is an emerging and rapidly growing financial ecosystem with the defining feature that it is powered by blockchain technology. The focus of this paper is on risks for DeFi protocols that could lead to economic losses that could be insurable. This framework was designed around the risks associated with the existing and emerging DeFi protocols.

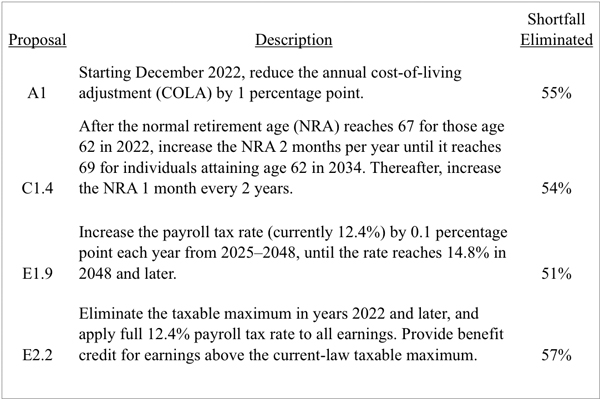

As seen from subtracting the total cost shown in Table 2 from the total income shown in Table 1, Social Security paid out $56.3 billion more in benefits and expenses than it collected in income.

Because Social Security has trust funds, the total costs of 2021 were still met. However, the trust funds declined in 2021 by the $56.3 billion that costs exceeded income. At the end of 2020, the trust funds totaled $2,908.3 billion, and at the end of 2021, the trust funds totaled $2,852.0 billion.

Social Security costs continue to be projected to exceed the income of the program, until the trust funds are projected to become depleted during 2035.

If changes to the program are not implemented before 2035, 80% of scheduled benefits would be payable after depletion of the trust funds in 2035, declining to 74% by 2096.

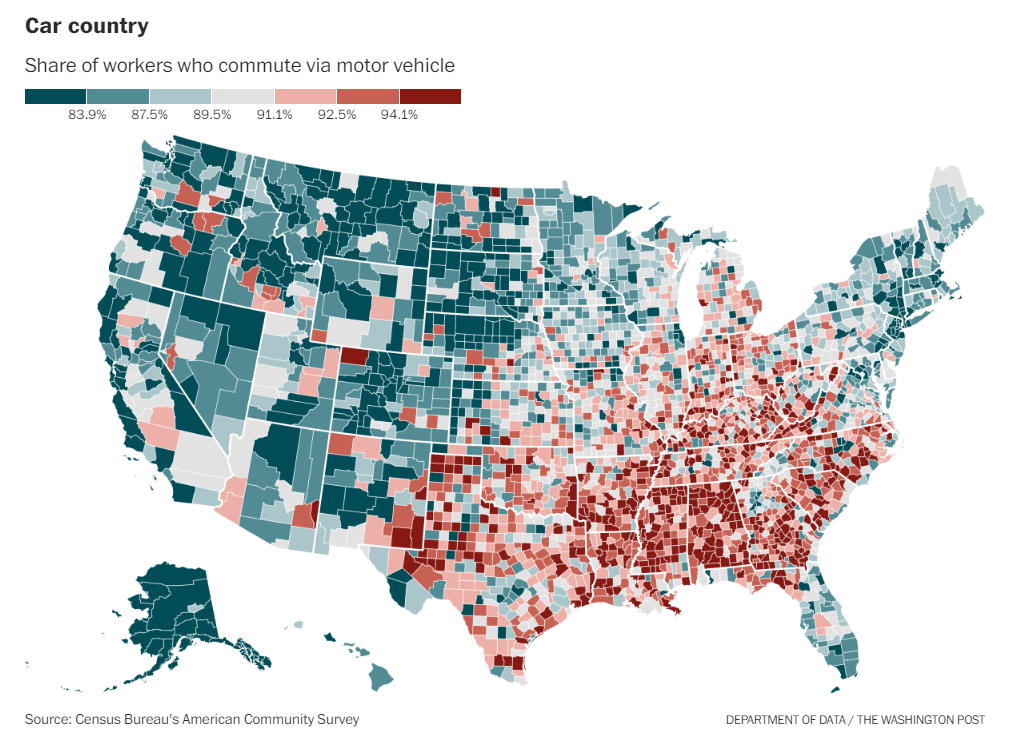

The places that drive the most tend to have the same high share of chain restaurants regardless of whether they voted for Trump or Biden. As car commuting decreases, chain restaurants decrease at roughly the same rate, no matter which candidate most residents supported.

If the link between cars and chains transcends partisanship, why does it look like Trump counties have more chain restaurants? It’s at least in part because he won more of the places with the most car commuters!

About 83 percent of workers commute by car nationally, but only 80 percent of folks in Biden counties do so, compared with 90 percent of workers in Trump counties. The share of car commuters ranges from 55 percent in the deep-blue New York City metro area to 96 percent around bright red Decatur, Ala.

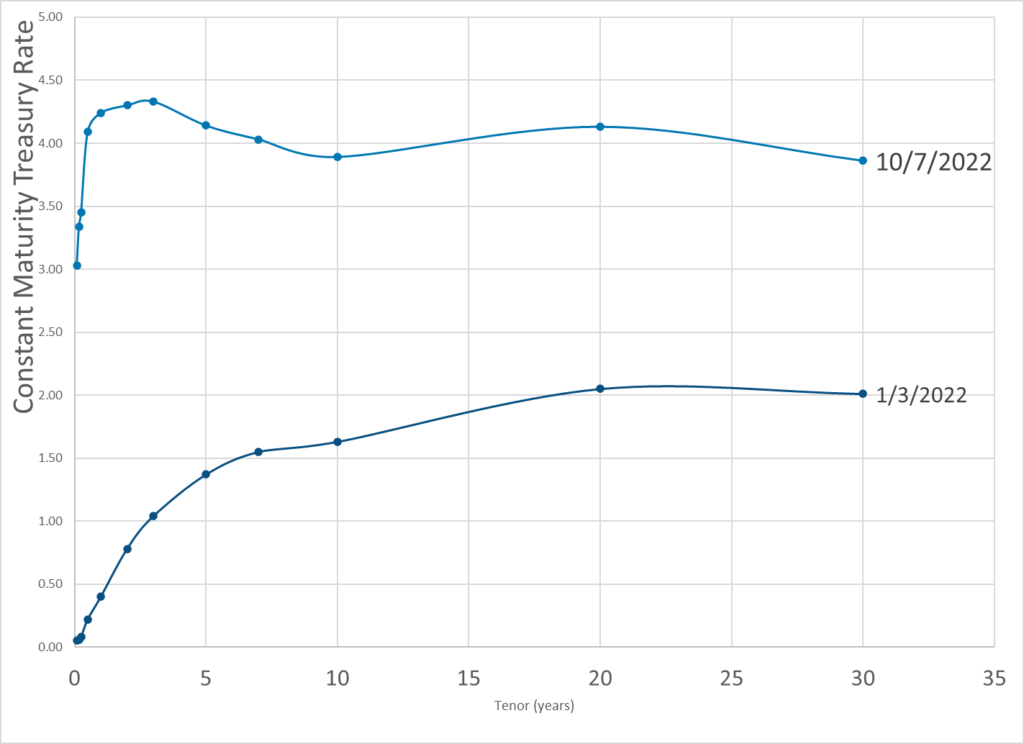

The central bank’s Financial Policy Committee stepped in after a massive sell-off of U.K. government bonds — known as “gilts” — following the new government’s fiscal policy announcements on Sept. 23.

The emergency measures included a two-week purchase program for long-dated bonds and the delay of the bank’s planned gilt sales, part of its unwinding of Covid pandemic-era stimulus.

The 30-year gilt yield fell more than 100 basis points after the bank announced its emergency package on Wednesday Sept. 28, offering markets a much-needed reprieve.

Cunliffe noted that the scale of the moves in gilt yields during this period was “unprecedented,” with two daily increases of more than 35 basis points in 30-year yields.

“Measured over a four day period, the increase in 30 year gilt yields was more than twice as large as the largest move since 2000, which occurred during the ‘dash for cash’ in 2020,” he said.

In June 2021 I co-authored an article with drowning prevention parent advocate Nicole Hughes on the subject of water competency in 1-4 year old children and which national swim lesson program methodology aimed to teach this highest risk age group survival skills to best protect against an unplanned submersion.

The purpose of this article was to provide parents and primary care pediatricians with a direct comparison of popular formal swim lesson curriculums of the American Red Cross, YMCA, and Infant Swim Resource (ISR) to inform them on which program better aligns with the parent’s goals for water competency for their young child.

A secondary objective of this commentary was to highlight the methodology of survival swim as a type of formal swim program that in many ways appears superior for this high risk age group due to its ability to teach independent back floating and swim float swim without flotation devices. Despite being the only prominent formal swim lesson program that does this for the under 4 year olds, the AAP without any evidence has come out guns blazing against it.

This is evidenced by the recent parent article in JAMA Pediatrics which states: “Teaching children to swim is important, and the American Academy of Pediatrics has recommended swim lessons as early as age 1 year to provide another protection layer. However, infant swim classes such as Infant Swimming Resource have not been shown to lower the risk of drowning. As an alternative, families may seek out parent-child water play classes to gain familiarity and comfort with being around water together.”

Yet despite the lack of data on benefit vs. harm for each type of formal swim lessons, the AAP feels justified to advocate against ISR survival swim while advocating for Mommy and Me group swim lessons with the goal of comfort over survival.

One year after the publication of our article, the American Academy of Pediatrics authors of the 2019 Policy on Drowning Prevention submitted a Letter to the Editor to Contemporary Pediatrics criticizing our article to which we responded in an Author Response. For unexplained reasons neither letter was published by the journal of record.

Due to the importance of advancing this conversation to better understand the likely benefit and lack of harm of survival swim as a crucial layer of drowning prevention protection, I will publish both the AAP Letter to Editor and Author Response below. It is my hope that you read both. When reading, please do so within the context of an AAP that willingly advocates for non-pharmacological interventions (NPI) such mandatory masking of children for prevention of COVID-19 – stating that there is no evidence that it causes harm or developmental delays while willingly advocating against ISR survival swim – stating that it is harmful and lacks evidence of benefit without any such evidence to make either claim.

Author(s): Todd R Porter

Publication Date: 1 Oct 2022

Publication Site: Authentic Pediatrics at substack

Younger workers are mostly excluded from those benefits, and few believe pension funds will be around to pay them at retirement time anyway. So younger workers want salary increases rather than promises. Also, portable, employee-directed accounts like 401(k)s rather than large and ever-increasing contributions to black-hole public pension systems. The fight in 2023 may be more between younger and older public employees than between united public employees and taxpayers.I think young employees will score their first victory after many years of getting pushed down. It will be short-term inflation then that applies lethal pressure in a tight labor market, not stock prices, interest rates or even longer-term expectations of price increases. Wages will have to be raised for public employees, who will refuse burdens from past underfunding or benefit cuts that apply only to them. The alternative is unacceptable declines in public services as the best employees quit, job openings go unfilled and qualifications for new hires are lowered.The most heavily indebted states, with the worst credit ratings and biggest pension funding shortfalls, may not be able to pay these increases. While 2022 should be a good revenue year for a majority of state and local governments, heavily indebted states with big pension-funding gaps need to brace for some serious headwinds. Illinois already spends 11% of its revenue to service debt. Increased yields on its bonds could double that to 22% as debt is refinanced, even if the state runs balanced budgets.

The temptation to cut benefits for retirees may be overwhelming. While these people can (and will) yell and scream, that’s easier to accept than a teachers’ strike or a police slowdown. Current employees can be offered generous wage increases and portable pensions. Reducing actuarial pension liabilities will please creditors and rating agencies. Taxpayers will appreciate being spared. In many states, cutting benefits will require a constitutional amendment or other legal heavy lifting, but with enough incentive, that can be done.

I expect something like Social Security reforms. A cap will cut benefits for people receiving the highest pensions, and states will put tax surcharges on benefits for high-income people even if they have moved out-of-state. Copays and deductibles will be increased for health coverage.

The first state to try this will face strong legal challenges, a nationwide union counteroffensive and significant in-state political resistance. But with enough fiscal pressure it may happen. If state administrations can keep current public employees on the sidelines, via wage increases and benefit restructuring, it might succeed.

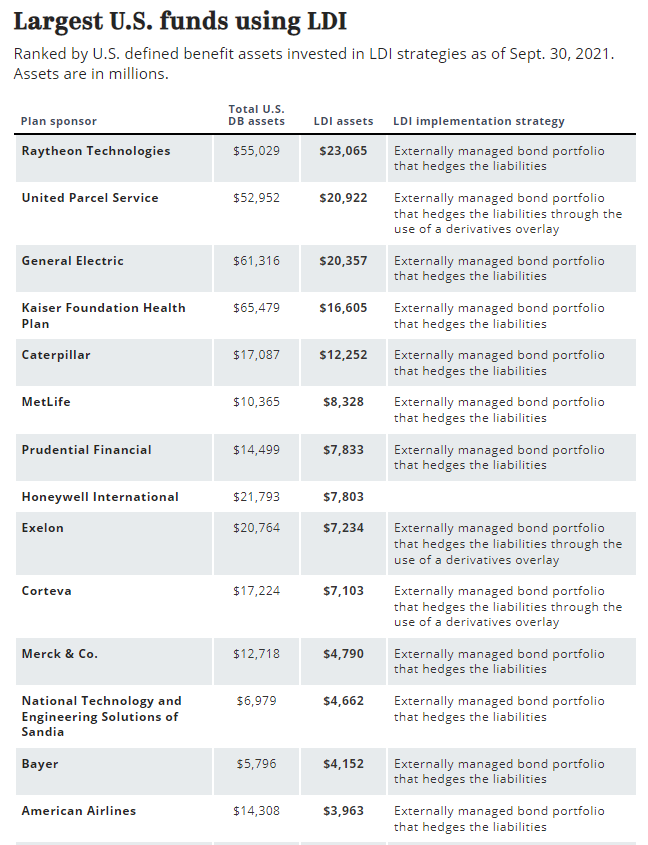

The Bank of England’s emergency bond-buying last week helped shore up U.K. pension funds and threw a spotlight on a popular strategy among corporate plans known as LDI – or liability-driven investing.

Total assets in LDI strategies in the U.K. rose to almost £1.6 trillion ($1.8 trillion) at the end of 2021, quadrupling from £400 billion in 2011, according to the Investment Association, a trade group that represents U.K. managers. Many LDI mandates allow for the use of derivatives to hedge inflation and interest rate risk.

….

Here’s how LDI works: Liability-driven investing is employed by many pension funds to mitigate the risk of unfunded liabilities by matching their asset allocation and investment policy with current and expected future liabilities. The LDI portion of a pension fund’s portfolio utilizes liability-hedging strategies to reduce interest-rate risk, which could include long government and credit bonds and derivatives exposure.

Jeff Passmore, LDI solutions strategist at MetLife Investment Management, said the situation with U.K. pension plans “has been challenging, and the heavy use of derivatives in the U.K. LDI model has made the current situation worse than it would otherwise be.”

While most U.S. LDI portfolios rely on bonds rather than derivatives, ‘”those U.S. plan sponsors who have leaned heavily on derivatives and leverage should take a cautionary lesson from what we’re seeing currently across the Atlantic.”

….

The U.K. pension debacle “is a plain-and-simple problem of leverage,” Charles Van Vleet, assistant treasurer and chief investment officer at Textron, said in an email.

Many U.K. pension plans were interest rate-hedged at 70%, while also holding 60% in growth assets, suggesting 30% leverage, he said. The portfolio’s growth assets have lost around 20% of value if held in public equities and fixed income or about 5% down if held in private equity, he noted.

“Therefore, to make margin calls on their derivative rate exposure they had to sell growth assets – in some cases, selling physical-gilts to meet derivative-gilt margin calls,” Mr. Van Vleet said.

“The problem is worse for plans who gain rate exposure with leveraged ETFs. The leverage in those funds is commonly via cleared interest rate swaps. Margin calls for cleared swaps can only be met with cash – not posted collateral. Therefore, again selling physical-gilts to meet derivative-gilt margin calls.”

Author(s):

BRIAN CROCE COURTNEY DEGEN PALASH GHOSH ROB KOZLOWSKI

State executives and lawmakers from both major political parties have recently threatened to use public retirement plan assets to address political grievances or push political agendas. Issues ranging from guns to oil and climate change to social media are all being suggested as political targets that should dictate investment strategies for public pension funds. When making arguments for their activist agendas, proponents of these various positions rarely mention how investment restrictions or demands will aid in the basic retirement plan objective of supporting public employees in their retirement years.

To be clear, public retirement plan assets should never be utilized for political purposes.

Trustees of these public pension plans, and others of influence, are under a clear fiduciary obligation to make decisions with the sole purpose of best meeting the pension plans’ objectives for the benefit of that plan’s participants. There is no ambiguity about this: Activist political agendas have no place in public pensions. To be effective in meeting their objectives, public pension systems must be completely apolitical in their decision-making and in their operations. They cannot be beholden to shifting political winds.

While this idea seems straightforward, the thought of using these massive investment portfolios to leverage certain political agendas is often too enticing for some politicians to pass up. It is incumbent upon governors, other key stakeholders, and legislative representatives in all states to step up and acknowledge that public retirement assets are out-of-bounds for activist maneuvering. This is critical regardless of where these figures fall on the political spectrum. It is equally important for retirement system trustees and leaders, as well as state treasurers, to stand firm as plan fiduciaries and vigorously oppose any attempts to use plan assets in a way that is not solely directed at benefitting the plan’s participants.