Graphic:

Publication Date: 22 Sept 2022

Publication Site: Dept of Treasury

All about risk

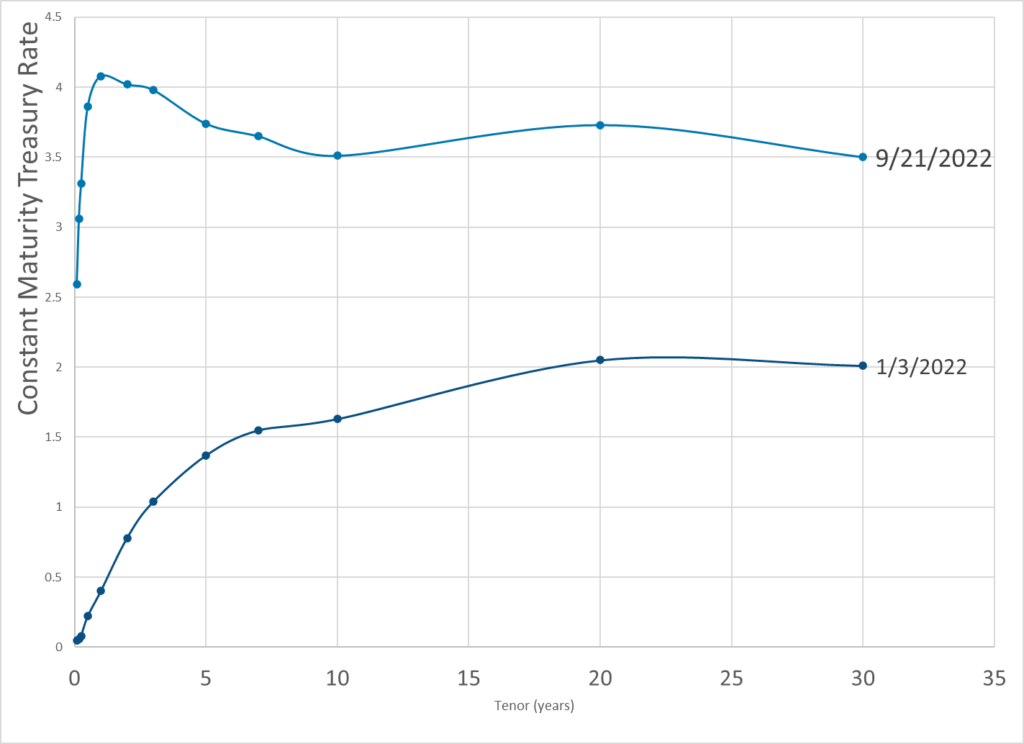

Graphic:

Publication Date: 22 Sept 2022

Publication Site: Dept of Treasury

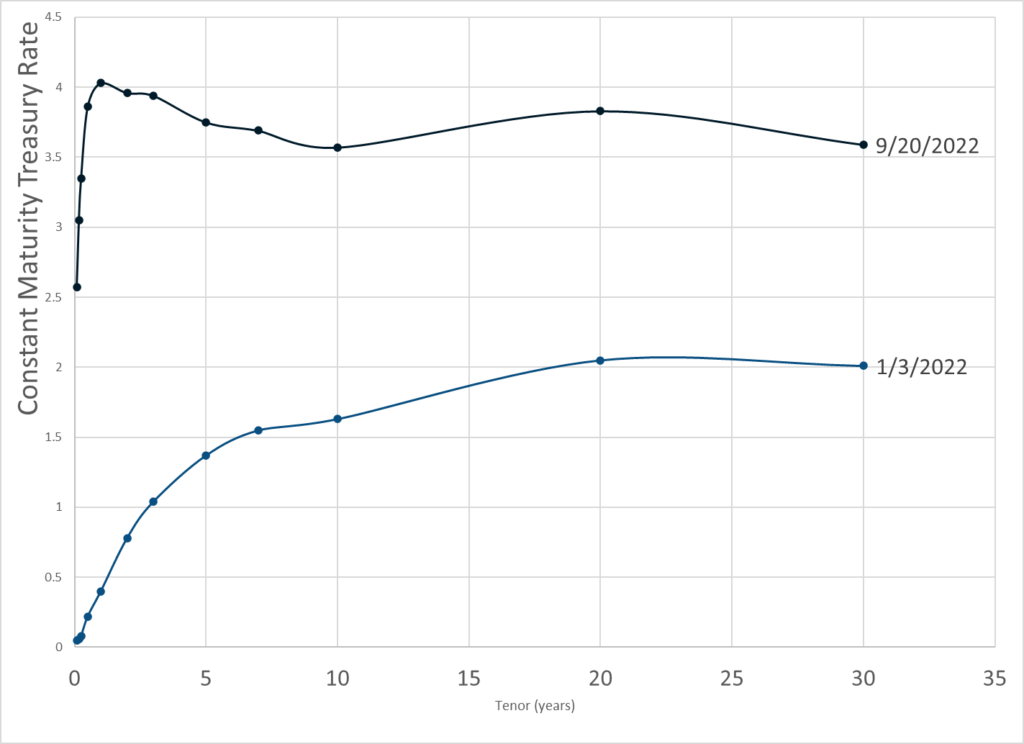

Graphic:

Excerpt:

The curve has been inverted in places for over a year. This is a recession signal and I believe the economy went into recession in May.

The Fed is merrily hiking away and is likely to keep doing so until it breaks something big time. The Fed will hike 75 basis points tomorrow and the market thinks another 75 basis points is coming in November.

If so, it is doubtful the markets will like it much.

Author(s): Mike Shedlock

Publication Date: 20 Sept 2022

Publication Site: Mish Talk

Graphic:

Excerpt:

Treasury Par Yield Curve Rates: These rates are commonly referred to as “Constant Maturity Treasury” rates, or CMTs. Yields are interpolated by the Treasury from the daily par yield curve. This curve, which relates the yield on a security to its time to maturity, is based on the closing market bid prices on the most recently auctioned Treasury securities in the over-the-counter market. These par yields are derived from indicative, bid-side market price quotations (not actual transactions) obtained by the Federal Reserve Bank of New York at or near 3:30 PM each trading day. The CMT yield values are read from the par yield curve at fixed maturities, currently 1, 2, 3 and 6 months and 1, 2, 3, 5, 7, 10, 20, and 30 years. This method provides a par yield for a 10-year maturity, for example, even if no outstanding security has exactly 10 years remaining to maturity.

Treasury Par Yield Curve Methodology: The Treasury par yield curve is estimated daily using a monotone convex spline method. Inputs to the model are indicative bid-side prices for the most recently auctioned nominal Treasury securities. Treasury reserves the option to make changes to the yield curve as appropriate and in its sole discretion. See our Treasury Yield Curve Methodology page for details.

Author(s): Treasury Dept

Publication Date: 21 Sept 2022

Publication Site: Treasury Dept

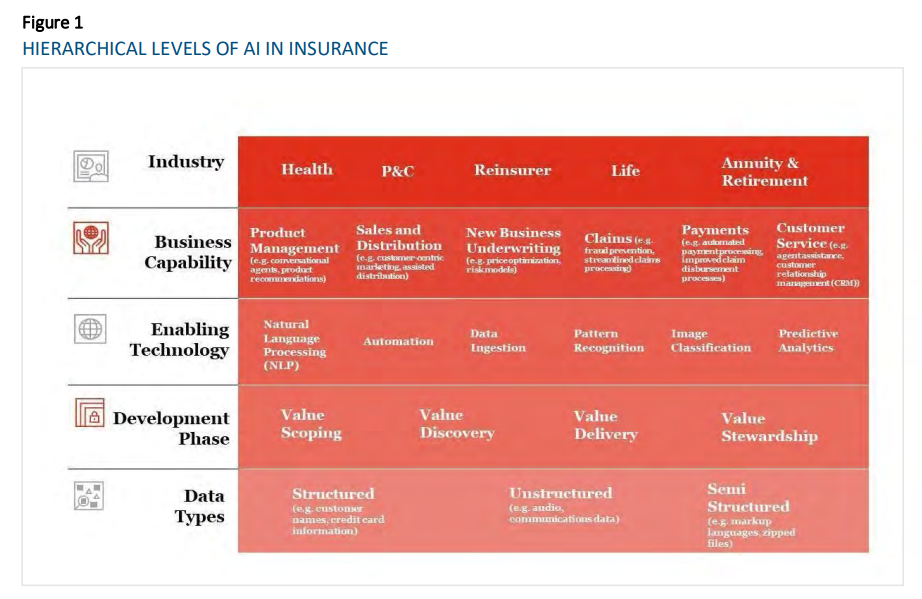

Link: https://www.soa.org/resources/research-reports/2022/avoid-unfair-bias-ai/

Graphic:

Excerpt:

Artificial intelligence (“AI”) adoption in the insurance industry is increasing. One known risk as adoption of AI increases is the potential for unfair bias. Central to understanding where and how unfair bias may occur in AI systems is defining what unfair bias means and what constitutes fairness.

This research identifies methods to avoid or mitigate unfair bias unintentionally caused or exacerbated by the use of AI models and proposes a potential framework for insurance carriers to consider when looking to identify and reduce unfair bias in their AI models. The proposed approach includes five foundational principles as well as a four-part model development framework with five stage gates.

Smith, L.T., E. Pirchalski, and I. Golbin. Avoiding Unfair Bias in Insurance Applications of AI Models. Society of Actuaries, August 2022.

Author(s):

Logan T. Smith, ASA

Emma Pirchalski

Ilana Golbin

Publication Date: August 2022

Publication Site: SOA Research Institute

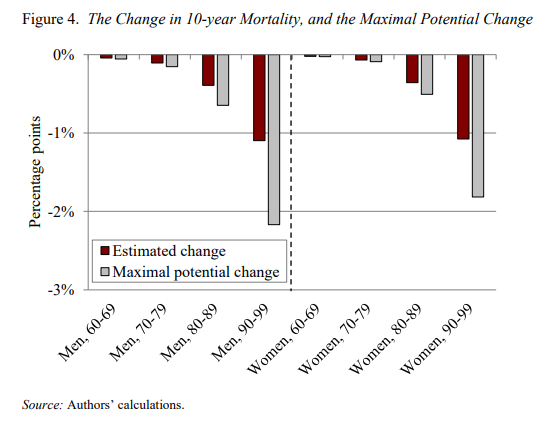

Report: https://crr.bc.edu/wp-content/uploads/2022/08/wp_2022-10.pdf

Graphic:

Abstract:

The mortality burden of the COVID-19 pandemic was particularly heavy among older adults, racial and ethnic minorities, and those with underlying health conditions. These groups are known to have higher mortality rates than others even in the absence of COVID. Using data from the 2019 American Community Survey, the 2018 Health and Retirement Study, and the 2020 National Vital Statistics System, this paper estimates how much lower the overall mortality rate will be for those who lived through the acute phase of the early pandemic after accounting for this selection effect of those who died from COVID. Such selection may have implications for life insurance and annuity premiums, as well as assessments of the financial standing of Social Security – if the selection is large enough to substantially alter projected survivor mortality.

The paper found that:

The policy implications of the findings are:

Author(s): Gal Wettstein, Nilufer Gok, Anqi Chen, Alicia H. Munnell

Publication Date: August 2022

Publication Site: Center for Retirement Research at Boston College

Link: https://marypatcampbell.substack.com/p/geeking-out-over-terminology

Graphic:

Excerpt:

In which I promote Dominic Lee’s new site Maverick Actuary, but also look at how we geeks can be more effective in communicating with the non-geeks.

Author(s): Mary Pat Campbell

Publication Date: 19 Sept 2022

Publication Site: STUMP on substack

Link: https://theactuarymagazine.org/volunteer-with-soa-education/

Excerpt:

As you begin (or consider) volunteering with Society of Actuaries (SOA) Education, you may have questions. As a long-time SOA Education volunteer and past general chairperson of SOA Education, perhaps I have answers that will help.

My volunteer journey began in 1993. I had just obtained my FSA when I got a call from SOA volunteer Bruno Gagnon, FCIA, asking if I wanted to get involved in SOA Education. It’s been an incredible journey of learning, support and networking since. I hope your volunteer journey is just as rewarding.

……

WHAT BENEFITS DOES VOLUNTEERING BRING?

The most interesting aspects of this endeavor are of a different nature. For example, the first privilege was to work with subject-matter experts who were highly regarded and respected in the industry and learn from them. This could be from a technical and leadership point of view. It was rewarding to see a group of volunteers with similar interests working together efficiently while having fun. The members had specific roles and would not hesitate to help their colleagues when needed. Over the years, SOA Education volunteers have shown they can adapt to change quickly. The adjustments that were put in place during the pandemic are a great example.A member volunteer can gain experience and look for opportunities to grow in their role and take on different responsibilities. The possibilities are diverse, allowing a member to become an expert in their role or a leader within the exam team, depending on their interests, skills and circumstances.

Having participated in all the possible levels within the SOA Education volunteer structure, I honestly can say the experience has been challenging at times—but always highly rewarding. I would relive the journey at any time, as I made very dear friends along the way.

Author(s): STELLA-ANN MÉNARD

Publication Date: Sept 2022

Publication Site: The Actuary, SOA

Link: https://www.dig-in.com/opinion/5-use-cases-for-machine-learning-in-the-insurance-industry

Excerpt:

4. Fraud detection

Unfortunately, fraud is rampant in the insurance industry. Property and casualty insurance alone loses about $30 billion to fraud every year, and fraud occurs in nearly 10% of all P&C losses. ML can mitigate this issue by identifying potential claim situations early in the process. Flagging early allows insurers to investigate and correctly identify a fraudulent claim.

5. Claims processing

Claims processing is notoriously arduous and time-consuming. ML technology is a tool to reduce processing costs and time, from the initial claim submission to reviewing coverages. Moreover, ML supports a great customer experience because it allows the insured to check the status of their claim without having to reach out to their broker/adjuster.

Author(s): Lisa Rosenblate

Publication Date: 9 Sept 2022

Publication Site: Digital Insurance

Link: https://www.soa.org/resources/research-reports/2022/determinants-life-insurance/

Graphic:

Excerpt:

The authors examine 19 factors to determine which were most closely linked to permanent and term life insurance premiums sold in the United States in 2020. With spatial regression analysis using multi-scale geographically weighted regression (MGWR) approach, the authors find the following 5 covariates to be the most statistically significant for and positively correlated with permanent insurance sold: household income, percentage of the population that is African American, education, health insurance, and Gini index (a statistical measure of wealth inequality). For term insurance sold, the 5 most significant covariates are household income, education, Gini index, percentage of households with no vehicles, and health insurance. Their relationships with term insurance sold are positive except for the percentage of households with no vehicles.

Author(s):

Wilmer Martinez

Kyran Cupido

Petar Jevtic

Jianxi Su

Publication Date: August 2022

Publication Site: SOA

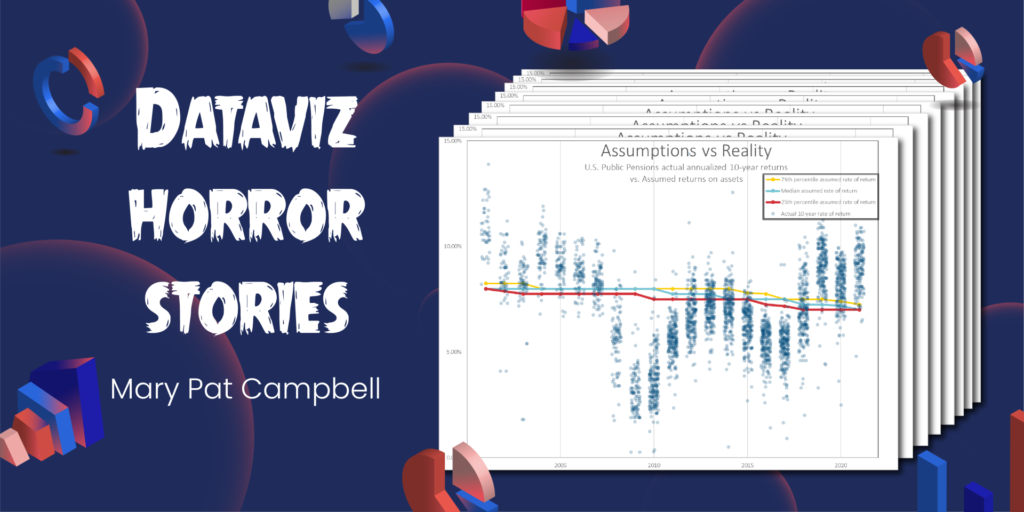

Link: https://nightingaledvs.com/dataviz-horror-story-how-i-crashed-the-top-execs-email/

Graphic:

Video:

Excerpt:

In my case, the graphs I made looked just fine—it’s just that I didn’t understand how copy/pasting graphs between Excel and Word worked (at the time). This was in the mid-2000s, when memory wasn’t quite so plentiful, so many corporate email accounts had memory quotas. If you hit that quota, you would be locked out of your email account. You had to call IT and actually talk to a person!

I was a lowly entry-level person at a financial services company and had done some Monte Carlo modeling involving 1,000,000 scenarios. We were developing a new mutual fund project, based on changing allocations over time as people moved towards retirement, and the company wanted me to model outcomes for different allocation trajectories. After a “full” model run of one million scenarios, I made diagnostic graphs showing the distribution of key metrics (such as the annual accumulation of the fund, how many times the fund decreased while the owner was in retirement, and whether – and when – the money in the fund ran out) so that we could analyze different potential fund strategies. The graphs themselves were fairly simple.

Author(s): Mary Pat Campbell

Publication Date: 31 Aug 2022

Publication Site: Nightingale

Link: https://marypatcampbell.substack.com/p/data-visualization-lessons-jitter

Video:

Excerpt:

Jitter charts are my new favorite tool for displaying how distributions change over time.

I used them to great effect in my recent post One Bad Year? Comparing the Long-Term Public Pension Fund Returns Against Assumptions.

I’m often looking at distributions, and wanting to communicate something about how those distributions change over time, or how distributions compare. Often, I have to simply pick out key percentiles in those distributions, or key aspects, such as mean and standard deviation.

But why not graph all the points in one’s sample directly, if one has them?

That’s where jitter charts can help.

Author(s): Mary Pat Campbell

Publication Date: 16 Sep 2022

Publication Site: STUMP at substack

Link: https://www.banking.senate.gov/hearings/current-issues-in-insurance

Excerpt: https://www.banking.senate.gov/imo/media/doc/Brown%20Statement%209-8-22.pdf

Statement from Chair Sherrod Brown (D-OH)

Every American needs insurance – whether it’s auto insurance to protect us when we’re on the

road, or homeowners’ insurance to protect the biggest investment for most families, or life

insurance to cement your family’s financial security in the event of a tragedy.

It’s our job to make sure that the industry is protecting Americans’ hard-earned money – not

putting it at risk.

American insurance companies are regulated by state insurance commissioners. The state-based

system of insurance regulation is historic, and ensures local markets and needs are taken into

consideration.

The National Association of Insurance Commissioners coordinates state commissioners across

all jurisdictions, to identify and address risks to the entire system.

In the Wall Street Reform Act, Congress created the Federal Insurance Office within the

Treasury Department to promote national coordination in the insurance sector. It’s common

sense – insurers operate across all state jurisdictions and internationally.

I’m pleased to have both the Maryland Commissioner Kathleen Birrane on behalf of the NAIC,

and Director Seitz of FIO testify today.

If we’re going to keep Americans’ hard-earned money safe, it is more important than ever that

they work together.

Today we’ll explore many important topics.

For example, three months ago, Lockheed Martin transferred $4.3 billion of its pensions to

Athene Holding – an insurance holding company specializing in life insurance and owned by the

private equity firm, Apollo Global Management.

Overnight, Lockheed Martin employees and retirees were notified that their pensions would be

managed by Athene and no longer governed by ERISA or the Pension Benefit Guaranty

Corporation.

This is just one recent example of private equity giants’ expansion into people’s pensions and the

insurance industry.

We know that workers end up worse off when Wall Street private equity firms get involved.

We’ve seen it over and over, in industry after industry.

In March, I asked the NAIC and FIO to look into private equity’s expansion into similar pensionrisk transfer transactions. We need to understand the risks to workers whose financial security

depends on pension and retirement programs.

The NAIC and FIO provided thoughtful responses to my letter. The NAIC has been monitoring

the risk-taking behavior of private equity-owned insurers.

FIO has done similar work, and also looked at the wider interconnectedness of insurance and

reinsurance markets across the world. Those connections have added to systemic risk concerns,

because U.S. insurance companies depend even more on the financial health of insurance

companies outside the U.S.

Taken together, our insurance authorities are focused on these emerging and complex risks to

safeguard our economy.

Our communities and families rely on insurance companies to protect their loved ones, their

homes, small business, and so many parts of our lives. We can’t ignore when risks build up, or

firms behave irresponsibly.

And we know who always pays the price when they do. It’s not insurance executives. It’s not

private equity executives. It’s not Wall Street.

It’s workers and their families. And it’s taxpayers, who were forced to bail out AIG 15 years ago.

That should never happen again.

That also means looking around the corner to make sure the industry and agencies are prepared

for risks as they develop. As more Americans face increasingly severe climate catastrophes like

wildfires and hurricanes each year, we need to help communities prepare – and we need to

ensure insurance watchdogs and the companies they oversee are prepared.

In the aftermath of some of these natural disasters, we have seen instances where insurers either

raise prices or stop offering insurance altogether, leaving families and businesses struggling to

find affordable coverage as they rebuild their lives and communities.

We also know this industry has a long history of racial discrimination, just like so many big

industries.

Black and brown families face more difficulty in getting insurance across the board. We’ve seen

this happen in auto insurance.

Earlier this year, The New York Times also reported that customers, insurance agents, and

employees sued State Farm for discrimination in the workplace and in paying out claims.

My colleague Chairwoman Waters has been working on learning more about this as well. Her

committee recently requested information about large life and P&C insurers’ involvement in

financing chattel slavery.

And I’m glad FIO and NAIC are also working on this. NAIC is investigating through its Special

Committee on Race and Insurance.

And I look forward to reviewing FIO’s upcoming report on availability and affordability of auto

insurance, and hope it will shed more light on racial equity in accessing this insurance.

Finally, later this year, the International Association of Insurance Supervisors will meet to

consider whether the U.S. insurance system’s review of capital adequacy standards meets

international criteria.

Because we regulate insurance differently here in the U.S., where state and local markets and

international markets are served by the same companies, it’s important that representatives of the

U.S. system like FIO and the NAIC advocate for fair treatment by the international regulators.

And now that the Fed Vice Chair for Supervision has been confirmed, Michael Barr and the

offices testifying here today will get to work with our international counterparts in this process.

All of these issues show how critical the work of FIO and NAIC is to our economy’s health and

stability. I expect FIO and NAIC to prioritize monitoring these risks in their ongoing work.

Publication Date: 8 Sept 2022

Publication Site: COMMITTEE ON BANKING, HOUSING, AND URBAN AFFAIRS of the U.S. Senate