The state Health Department intentionally “misled the public” regarding the number of COVID-19 deaths in nursing homes under former New York Gov. Andrew Cuomo’s administration, according to a scathing audit from the Comptroller Thomas P. DiNapoli.

When the COVID-19 pandemic swept through New York, the Department of Health was not prepared to respond to the infectious disease outbreaks in nursing homes, according to the audit, which helped lead to the inaccurate virus-related death count in facilities.

Auditors found that health officials undercounted the death toll in nursing homes by at least 4,100 residents and at times more than 50 percent, despite claims from the former governor, who said the state was doing well in protecting seniors.

A new set of revisions to the National Association of Insurance Commissioners requirements that govern real estate investments on the part of life insurers could be teeing up the asset class for growth in the future, as barriers to entry are lowered.

Late last year, the NAIC released a set of changes to its risk-based capital requirements that, for life insurers, lowered the factor for life and health companies. For so-called Schedule A investments—properties owned outright by carriers—the required set-aside was lowered to 11% from 15%. In the case of Schedule BA investments, such as partnerships and funds where the carrier isn’t the sole owner, that figure went down to 13% from 23%.

George Hansen, senior industry research analyst, AM Best, said life insurers traditionally have only placed about 6% of their portfolios in Schedule BA real estate products and less than 1% in Schedule A real estate investments. Whether there’s any increase and by how much will likely be tied to which segments of the industry carriers are in, but Hansen said he doesn’t expect a huge increase.

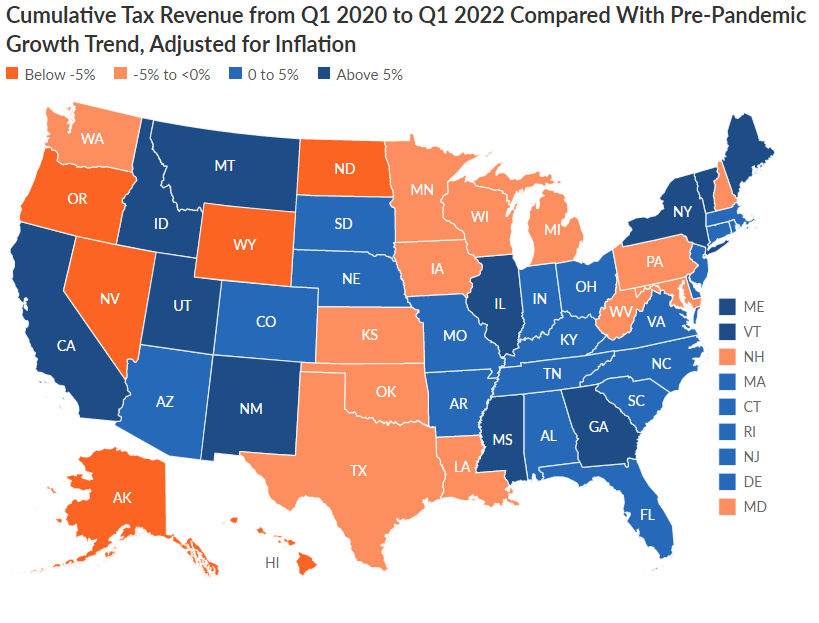

As the first quarter of 2022 came to an end and the United States passed the two-year anniversary of the start of the COVID-19 pandemic, total state tax revenue was at its highest level since just before its historic decline in early 2020. Collections were 18.1% greater than those for the final quarter of 2019, after adjusting for inflation and averaging across four quarters to smooth seasonal fluctuations. Only Wyoming and North Dakota had not taken in enough revenue to surpass their pre-pandemic levels.

Nationwide and in 31 states as of the end of the first quarter of 2022, cumulative tax receipts since the pandemic’s start, adjusted for inflation, were even higher than they would have been if pre-COVID growth trends had continued—despite fallout from the pandemic and a two-month recession. According to Pew estimates, Idaho led all states, with 16% more cumulative tax revenue than it would have collected under its pre-pandemic growth rate. New Mexico was second at 15.5% above the trend. Nationally, combined tax revenue at the end of the first quarter of 2022 was 3% above estimates of what might have been collected had the pandemic not occurred.

However, estimates also show that cumulative tax revenue fell short of its pre-COVID growth trend in slightly more than a third of states since the pandemic’s onset, and most other states’ recoveries largely followed historical trends.

Looking at cumulative totals since the start of the pandemic offers a way to identify states in which tax revenue has over- or underperformed since January 2020, based on pre-COVID trends. This approach also provides a different view of the strength of collections from the often-astonishing quarterly and annual percentage increases that were skewed by this particularly volatile period. For each of the nine quarters from Jan. 1, 2020 to March 31, 2022, Pew calculated the difference between actual tax revenue and estimates of how much each state would have collected had revenue grown at its pre-pandemic, five-year average annual growth rate.

The MBTA’s largest union is challenging an independent arbitrator’s decision that would reshape the rules of the authority’s $1.66 billion retirement system, including slashing the pensions of those who retire before the age of 65.

…..

Still, after more than four years of negotiations over a pension agreement, it’s unclear what exact changes could come to the MBTA’s retirement fund, where the number of retirees has long outpaced the amount of workers paying into it, and MBTA officials have long pressed for sweeping changes.

As of the end of last year, the fund’s unfunded liability hovered at more than $1.3 billion, and, despite changes that went into effect a decade ago to stem what were considered lavish retirement perks, younger retirees have continued to flow into the retirement system, creating more financial pressure.

….

The arbitrator’s decision included a series of changes, most notably in lifting the age at which a retiree would collect an “unreduced” pension. Under the ruling, workers who opt for early retirement — in this case, before the age of 65 — would have 6 percent deducted from their pension benefit for every year of retirement before the age of 65.

Currently, anyone who is 55 and has at least 25 years of service qualifies for a so-called normal monthly pension, calculated at 2.46 percent of the average of a person’s three consecutive highest-earning years, multiplied by years of service.

The Supreme Court’s unwillingness to intervene in a fight among states over taxing income from remote work may spark a jurisdictional revenue war. In August, the Court refused to take up a lawsuit by New Hampshire against Massachusetts’ practice of levying income taxes on Granite State residents employed by Bay State companies but working from home during the Covid lockdowns. Now New Jersey officials, who filed an amicus brief in the case because the state’s telecommuting residents are similarly taxed by New York, have proposed a law that would let the state tax telecommuters, including possibly tens of thousands of Empire State residents now working from home but employed by Garden State companies. The in-your-face legislation also provides incentives for Jersey residents to challenge New York’s law in tax court—one of the only venues left to residents after the Supreme Court decision. Given that several hundred thousand New Yorkers once commuted to other states to work and may now be staying home to telecommute, Albany risks losing revenues.

Beginning in March 2020, Covid restrictions brought a sharp rise in telecommuting, or working remotely from home. Studies have suggested that, during the pandemic’s initial phases, up to 36 percent of all private-sector employees, or about 43 million people, worked at home at least one day a week, and 15 percent, or about 18 million, telecommuted full-time. Census data before the pandemic found that as many as 6 million workers regularly cross state lines to go to their jobs. So it’s likely that several million current telecommuters have jobs with firms in another state. In New Hampshire, about 15 percent of residents with jobs—some 84,000 workers—commuted to Massachusetts pre-pandemic.

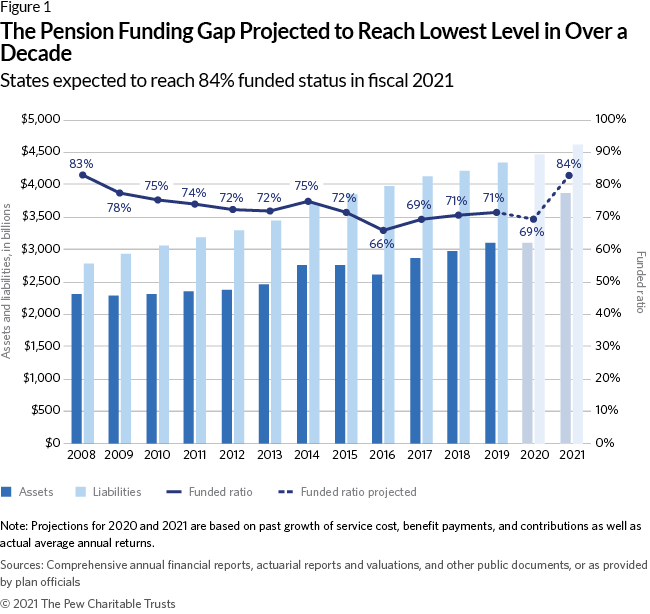

Since the fiscal 2019 reporting period ended, an unprecedented $5 trillion in federal stimulus and other government interventions have buoyed financial markets and strengthened plan balance sheets.2 As a result, state plans earned returns of over 25% in fiscal 2021—a highwater mark not seen since the 1980s. Pew estimates that total unfunded liabilities dropped below $1 trillion by the end of fiscal 2021, which would push state plans to be more than 80% funded for the first time since 2008. (See Figure 1; for more detail, see also Appendix G.) The significant improvement in plans’ fiscal position is due in large part to dramatic increases in employer contributions to state pension funds in the past decade, which boosted assets by more than $200 billion. Since 2010, annual contributions to state pensions have increased by 8% annually, twice the rate of revenue growth. And for the 10 lowest-funded states, the yearly growth in employer contributions averaged 15% over this period. As a result, after decades of underfunding and market losses from risky investment strategies, for the first time this century states are expected to have collectively achieved positive amortization in 2020—meaning that payments into state pension funds were sufficient to pay for current benefits as well as reduce pension debt.

An increase in pension contributions of the size seen over the past decade signals a shift in budget priorities by state policymakers and a recognition that the costs of postponing obligations are untenable if left unaddressed. Although this has improved the outlook for state pension plans, it has also crowded out spending on other important programs and services and left states with less budgetary space to sustain future rises in pension payments.

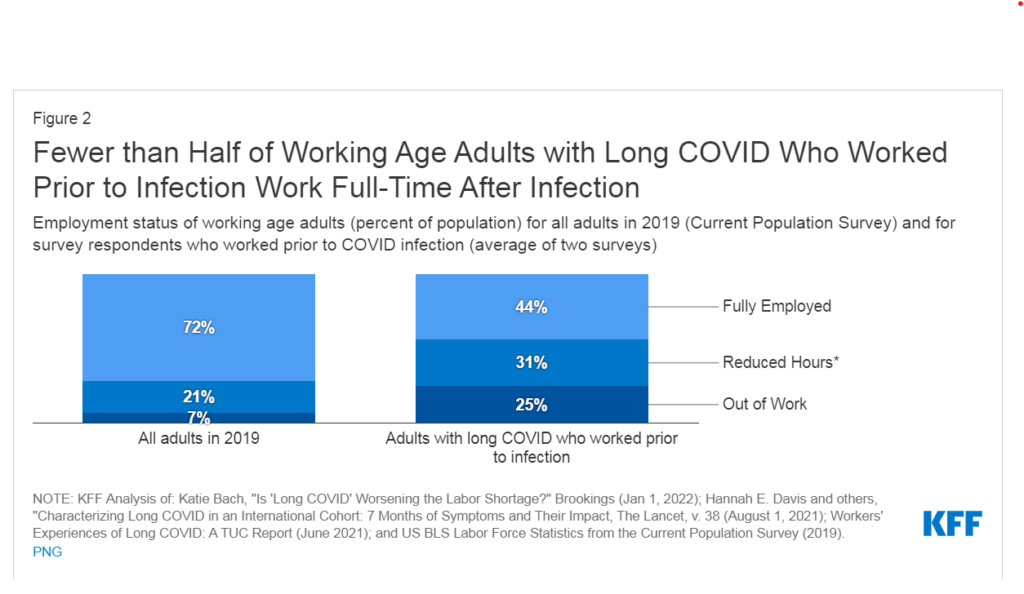

Preliminary evidence suggests there may be significant implications for employment: Surveys show that among adults with long COVID who worked prior to infection, over half are out of work or working fewer hours (Figure 2). Many conditions associated with long COVID—such as malaise, fatigue, or the inability to concentrate—limit people’s ability to work, even if they have jobs that allow for remote work and other accommodations. Two surveys of people with long COVID who had worked prior to infection showed that between 22% and 27% of those workers were out of work after getting long COVID. In comparison, among all working-age adults in 2019, only 7% were out of work. Given the sheer number of working age adults with long COVID, the employment implications may be profound and are likely to affect more people over time. One study estimates that long COVID already accounts for 15 percent of unfilled jobs.

The Wharton professor Jeremy Siegel has a big issue with the Federal Reserve’s aggressive interest-rate hikes in its bid to tame inflation, and he’s worried that the central bank is making the biggest mistake in its history and may provoke a steep recession.

Siegel said inflation is starting to come down significantly, but the Fed is still moving forward with its rate hikes.

He said it could be “one of the biggest policy mistakes in the 110-year history of the Fed, by staying so easy when everything was booming.”

…..

“I think the Fed is just way too tight. They’re making exactly the same mistake on the other side that they made a year ago,” Siegel added.

To Siegel’s point, the Fed has had a lousy record of accurately forecasting where it expects interest rates to be just a few months into the future.

….

“I am very upset. It’s like a pendulum. They were way too easy through 2020 and 2021, and now ‘we’re going to be real tough guys until we crush the economy,'” Siegel said of the Fed.

Siegel expects the Fed to “eventually see the light” as none of their recent predictions are likely to come true.

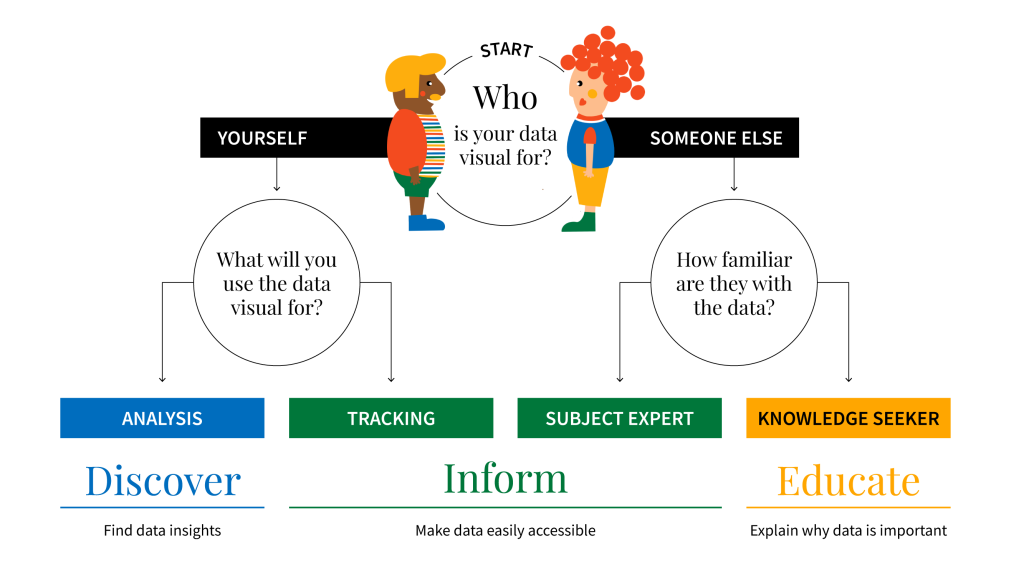

To quote Andy Kirk, “we can look at data, but we cannot really see it. To see data, we need to represent it in a different, visual form.” So, in an attempt to make data more accessible, you may create more visual representations – dots, lines, shapes, and colours. These building blocks combine to create all sorts of charts and pictures helping readers understand numbers.

Although the purpose of visualising data is clear (and universal), the reasons can be different. The reason you visualise data, will help you determine the appropriate visual.

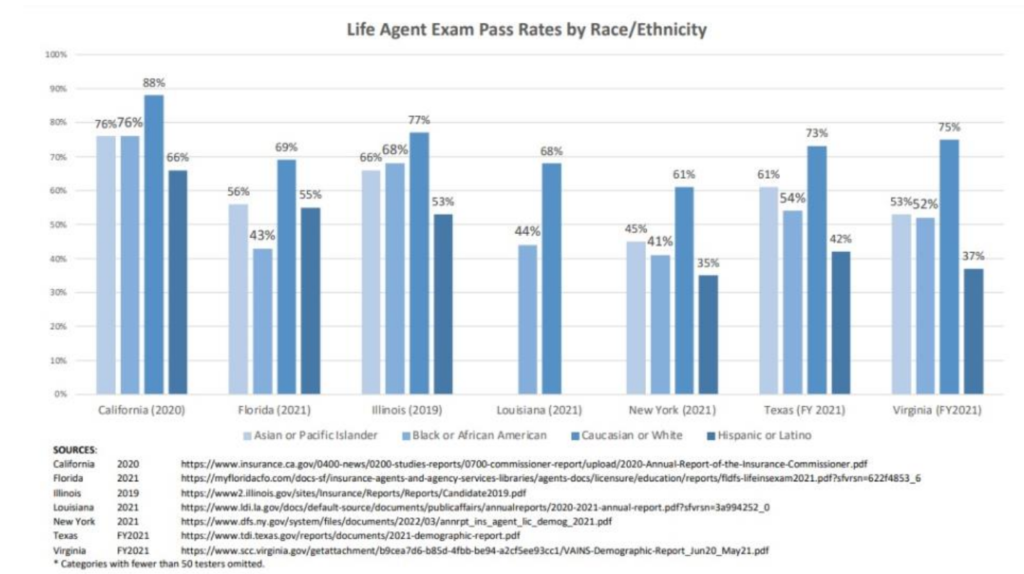

There have been recent efforts by the NAIC to report on the steps exam vendors have taken to mitigate cultural bias in producer licensing exams; however, based on state-level data, this issue deserves closer attention.

There are only seven states that annually prepare and publish licensing exam pass rates by demographic, including race/ethnicity. For more than a decade, these reports have routinely shown Caucasian/white candidates scoring higher than other demographic groups across nearly all lines.

When comparing Life Insurance Exam Pass Rates by Race/Ethnicity, an alarming trend appears. It’s clear that non-Caucasians or non-white demographics are not efficiently making it through the licensing process. This clearly suggests licensing exams warrant more scrutiny, particularly to ensure these tests are not screening diversity from the industry.

The American Council of Life Insurers has joined with two rival producer groups, the National Association of Insurance and Financial Advisors and Finseca, to send state lawmakers, insurance commissioners and other policymakers a new 10-page position paper, “A Workplan to Identify & Remove Unnecessary Barriers to Producer Licensure.”

The groups contend that better licensing rules would expand the supply of agents, brokers and other insurance producers, as well as increase producer diversity.

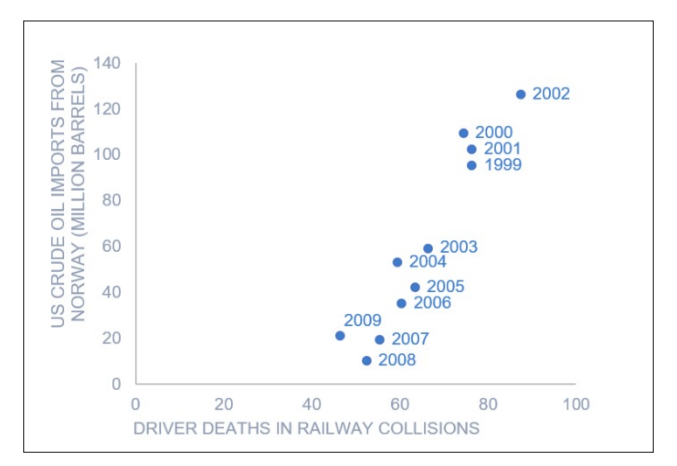

Examine the quality of the theory behind the correlated variables. Is there good reason to believe, as validated by research, the variables would occur together? If such validation does not exist, then the relationship may be spurious. For example, is there any validation to the relationship between the number of driver deaths in railway collisions by year (the horizontal axis), and the annual imports of Norwegian crude oil by the U.S., as depicted below?36 This is an example of a spurious correlation. It is not clear what a rational explanation would be for this relationship.