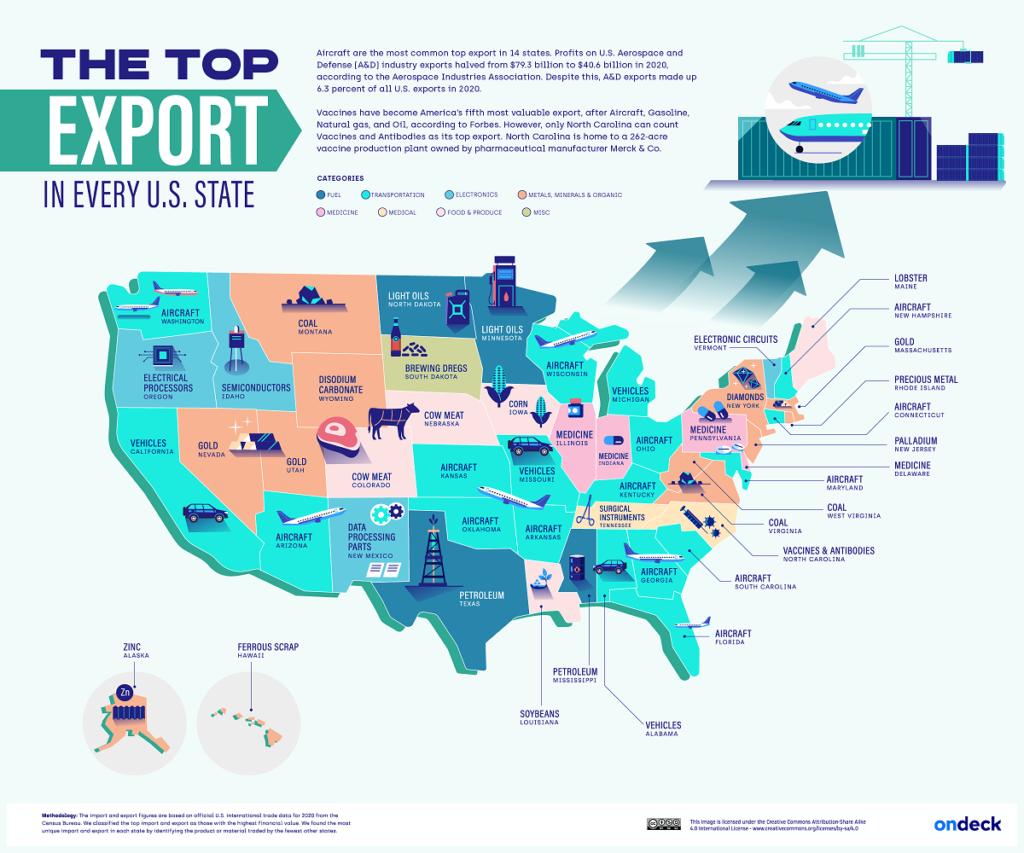

The U.S. exported over $1.3 trillion in goods in 2020, the second-highest amount worldwide.

While refined petroleum was the top export overall at $58.4 billion, aircraft exports were actually the highest across 14 states—more than any other form of export.

This infographic from OnDeck shows America’s top exports by state, using January 2022 data from the U.S. Census Bureau.

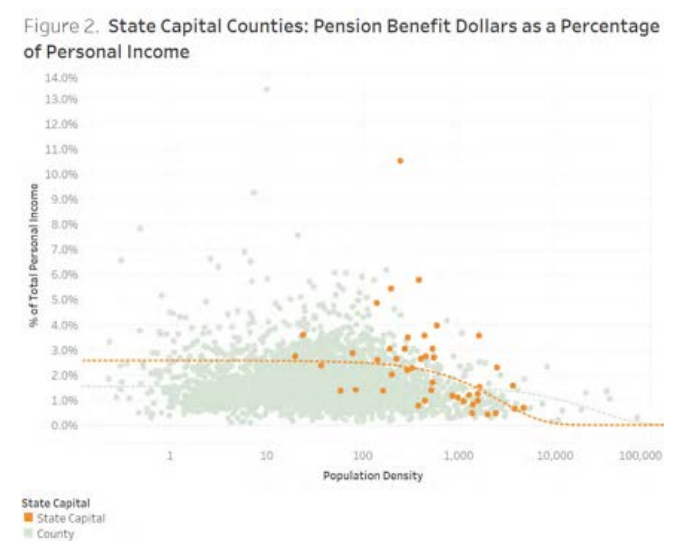

Public pension benefit dollars represent between one and three percent of GDP on average in the 2,922 counties studied.

Rural counties have the highest percentages of their populations receiving public pension benefits.

Small town counties experience a greater relative impact in terms of both GDP and total personal income from pension benefit dollars than rural or metropolitan counties.

Rural counties see more of an impact in terms of personal income than metropolitan counties, while metropolitan counties and rural counties see an equivalent impact in terms of GDP.

Counties that contain state capitals are outliers from other metropolitan counties, likely because there is a greater density of public employees in these counties, most of whom remain in these counties in retirement.

On average, rural counties have lost population while small town counties and metropolitan counties have gained population in the period between 2000 and 2018, but the connection between population change and the relative impact of public pension benefit dollars is weak.

Author(s): Dan Doonan and Tyler Bond from NIRS, Nathan Chobo from Linea Solutions Inc.

Publication Date: July 2022

Publication Site: National Institute on Retirement Security

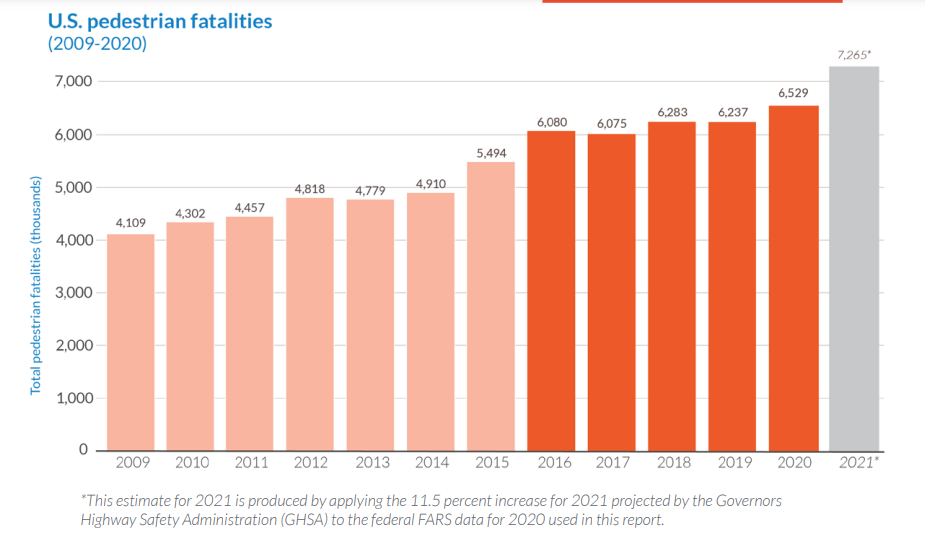

While the unprecedented COVID-19 pandemic upended many aspects of daily life, including how people get around, one terrible, long-term trend was unchanged: the alarming increase in people being struck and killed while walking. The number of people struck and killed while walking has been steadily increasing since 2009, reaching another new high in 2020 and likely a historic one in 2021.

More than 6,500 people— nearly 18 per day— were struck and killed while walking in 2020, a 4.7 percent increase over 2019, even as driving decreased overall because of the pandemic’s unprecedented disruptions to travel behavior.1

When thinking of traffic accidents, it would be an understandable reaction to imagine a car crash: the National Highway Traffic Safety Administration estimates that nearly 43,000 people died in 2021 on US roads. That’s a 10.5 percent jump from 2020 and the most fatalities since 2005. But pedestrian deaths are another form of traffic accident—and those rates are rising, fast.

A new study from Smart Growth America, an urban development-focused nonprofit, found that the number of pedestrian fatalities spiked more than 60 percent in the last decade. In 2020 alone, more than 6,500 people were struck and killed by vehicles—a record high that equates to nearly 18 people dying every day. And despite fewer cars on the road during the COVID-19 pandemic, the number of pedestrian deaths might have been even higher in 2021, according to the Governors Highway Safety Association. Preliminary data from GHSA suggests that roughly 7,500 people were killed last year. If confirmed, this would be the highest number in 40 years.

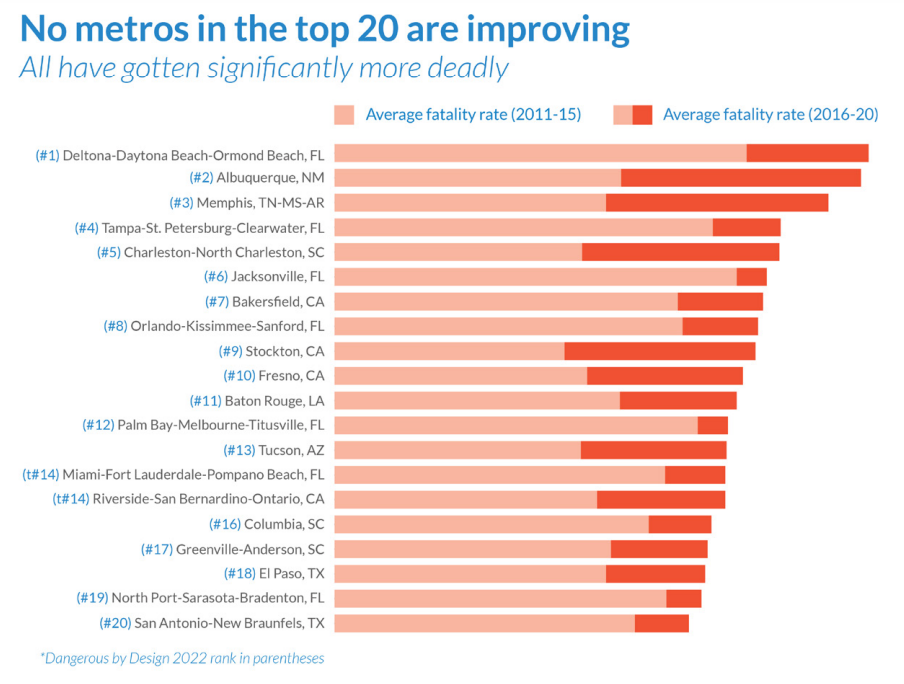

The study also presents new data identifying the deadliest metro areas and states for pedestrians. That the US experiences more pedestrian deaths than any other high-income nation isn’t random, researchers from Smart Growth America say. It’s by design.

The C$539 billion ($431.7 billion) Canada Pension Plan Investment Board has invested $334 million to acquire a 19.3% stake in Colombia-based discount grocery store chain D1, formerly known as Koba Colombia. The deal marks the pension giant’s first direct private equity investment in the country.

D1, which first opened for business in 2009 and officially took on its new name last month, recently announced it has become Colombia’s main food retailer. Citing findings from Nielsen, the company said it had a 9.7% share in the retail market and a 74% share in the so-called “hard discount” sector at the end of 2021. D1 has over 2,000 stores and reported 2021 operating income of more than $10.9 billion, which was a 32% increase from 2020. It also said this year.

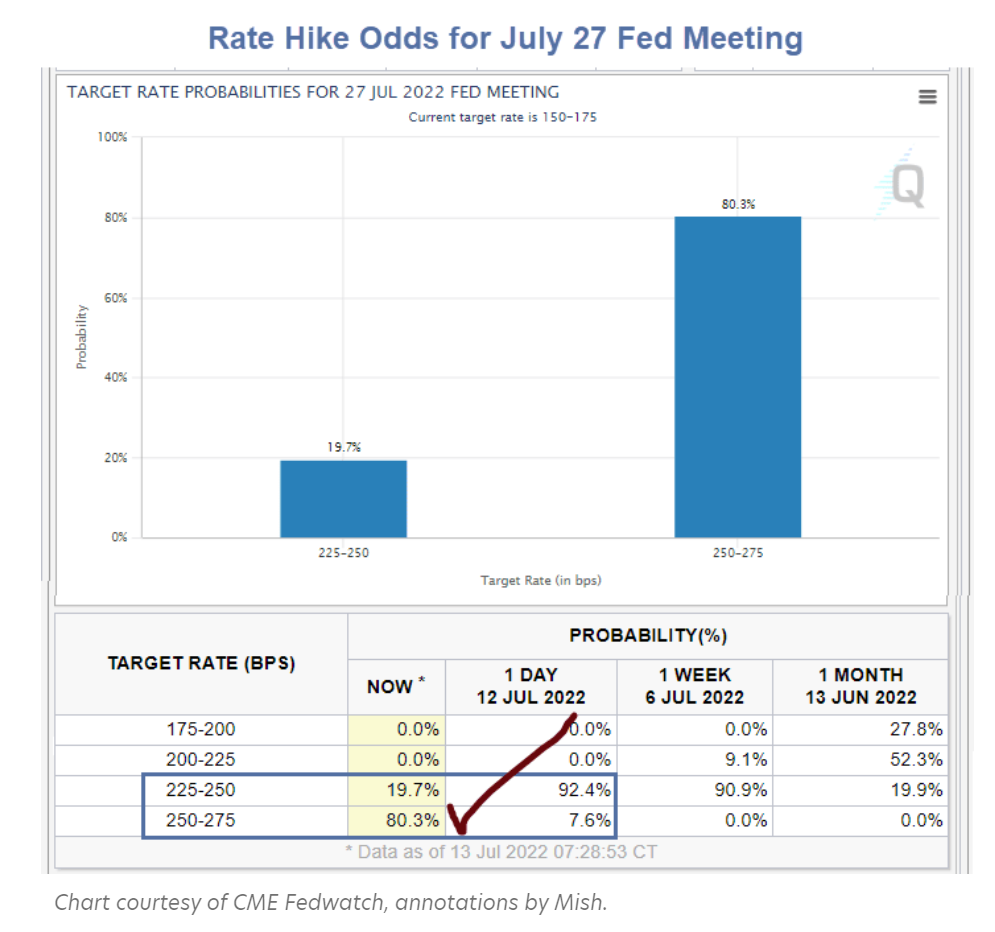

Yesterday, the market penciled in a three-quarter point hike. Today, the market expectation is for a full point hike.

The WSJ notes that would be the largest hike since the Fed started directly using overnight interest rates to conduct monetary policy in the early 1990s.

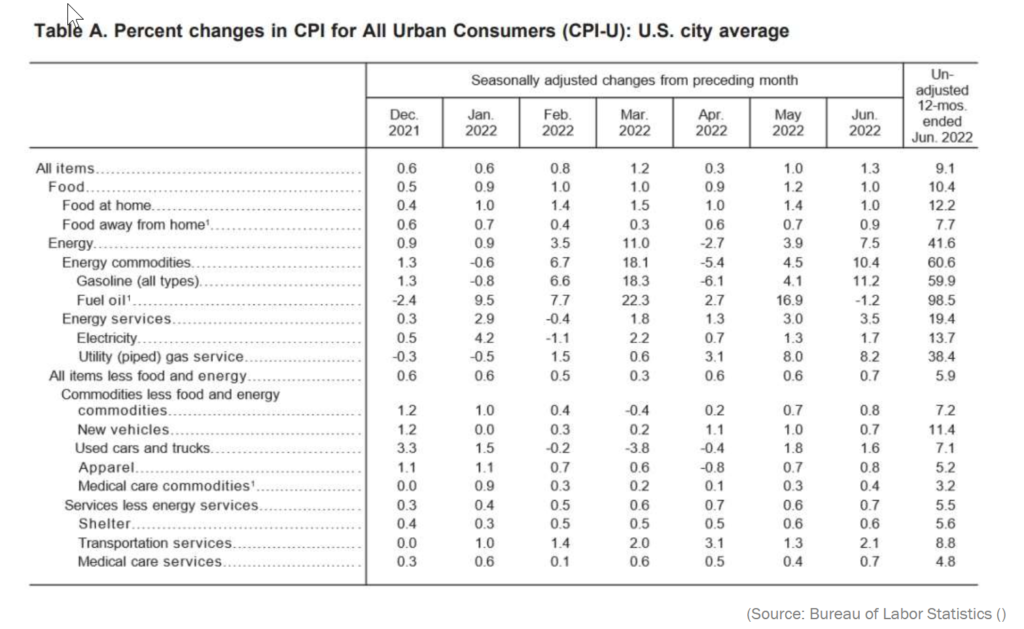

Prices were 9.1 percent higher in June than a year before, exceeding expectations and surging to a 41-year high.

Department of Labor data released Wednesday morning showed that inflation picked up speed in June, rather than slowing. Prices rose by 1.3 percent during the month, up from a 1 percent increase in May. A sharp rise in energy prices, and gasoline prices particularly, helped power the annualized inflation rate to its highest levels in more than four decades. Food prices rose by 1 percent during June, and are up 10.4 percent over the past year.

CalPERS is up to its old crooked, value-destroying ways. Its sale of $6 billion in private equity positions, at a big discount….because CalPERS was in a hurry despite no basis for urgency, shows yet again the sort of thing the giant fund routinely does that puts it at the very bottom of financial returns for major public pension funds.

In Dawm Lim’s Bloomberg story, Calpers Unloads Record $6 Billion of Private Equity at Discount, CalPERS admits to cooking the books. Not recognizing the sale (the loss in value) in the same fiscal year can only be to play shenanigans with the rate of return. So if, or more likely when, CalPERS again does badly in comparison to CalSTRS and similar funds, remember it would be even worse if CalPERS was accounting honestly.

RETHINKING UNINSURABILITY While many have viewed insurability as a binary choice with respect to a risk (i.e., insurable or uninsurable), insurability is more appropriately considered on a continuum, ranging from easy-to-insure, such as automobile or life insurance, to difficult-to-insure, such as pandemic, loss of the electrical grid, and other extreme catastrophic risks.

FRAMEWORK The role of private and public sectors in dealing with risks that are difficult-to-insure should be to develop strategies that enable a greater degree of insurability. To do so, the framework suggests that policymakers consider three fundamental options in dealing with the insurance industry:

Status Quo (SQ) –This option (SQ) contemplates a similar dynamic to that experienced with COVID-19, wherein businesses, nonprofits, and local governments found limited (if any) insurance coverage for their losses and ex post relief programs funded by the government.

Service Provider (SP) – This option (SP) contemplates an administrative, non-risk-bearing role for the insurance industry while the entire cost of claims would be publicly financed.

Service and Risk (SR) –In addition to its role as a service provider as characterized by SP, this option (SR) would expect insurers to commit capital – in an amount that does not threaten their financial viability – to cover a specified layer or other defined element of losses.

Despite significant changes in the economy since the onset of the Great Attrition (or what many call the Great Resignation), the share of workers planning to leave their jobs remains unchanged from 2021, at 40 percent. That’s two out of five employees in our global sample who said that they are thinking about leaving in the next three to six months.

However, the past year has revealed nuances of the larger trend:

Reshuffling. Employees are quitting and going to different employers in different industries (48 percent of the job leavers in our sample). Some industries are disproportionately losing talent, others are struggling to attract talent, and some are grappling with both.

Reinventing. Many employees leaving traditional employment are either going to nontraditional work (temporary, gig, or part-time roles) or starting their own businesses. Of the employees who quit without a new job in hand, 47 percent chose to return to the workforce. However, only 29 percent returned to traditional full-time employment.

Reassessing. Many people are quitting not for other jobs but because of the demands of life—they need to care for children, elders, or themselves. These are people who may have stepped out of the workforce entirely, dramatically shrinking the readily available talent pool.

Author(s): Aaron De Smet, Bonnie Dowling, Bryan Hancock, and Bill Schaninger

We study aggregate lapsation risk in the life insurance sector. We construct two lapsation risk factors that explain a large fraction of the common variation in lapse rates of the 30 largest life insurance companies. The first is a cyclical factor that is positively correlated with credit spreads and unemployment, while the second factor is a trend factor that correlates with the level of interest rates. Using a novel policy-level database from a large life insurer, we examine the heterogeneity in risk factor exposures based on policy and policyholder characteristics. Young policyholders with higher health risk in low-income areas are more likely to lapse their policies during economic downturns. We explore the implications for hedging and valuation of life insurance contracts. Ignoring aggregate lapsation risk results in mispricing of life insurance policies. The calibrated model points to overpricing on average. In the cross-section, young, low-income, and high-health risk households face higher effective mark-ups than the old, high-income, and healthy.

Author(s): Ralph S. J. Koijen, Hae Kang Lee & Stijn Van Nieuwerburgh

USAA — a policyholder-owned insurer that has historically focused on serving military veterans and their relatives — may be the big U.S. life insurer with the lowest policy lapse rate.

A team of researchers led by Ralph S.J. Koijen has presented data supporting that conclusion in a new analysis of how economic slumps affect which insureds drop their life insurance.

To conduct that analysis, the Koijen team crunched data from the public financial reports of the 30 biggest U.S. life insurer groups, for a period from 1996 through 2020.

….

Overall, a severe crisis, such as the 2007-2009 Great Recession, might increase a company’s life policy lapse rate by about 1 percentage point or more, after holding other factors considered equal, the researchers concluded.

The researchers found that, after holding factors such as risk class, smoking use and type of coverage equal, being under age 35 increased the risk of letting a life policy lapse by 46%, and being ages 25 through 34 during an economic slump increase lapse risk by an additional 15%.