Link: https://twitter.com/AlecStapp/status/1528859020098154496

Graphic:

Publication Date: 23 May 2022

Publication Site: Twitter

All about risk

Link: https://twitter.com/AlecStapp/status/1528859020098154496

Graphic:

Publication Date: 23 May 2022

Publication Site: Twitter

Link: https://www.sec.gov/news/press-release/2022-84

Excerpt:

The SEC’s complaint, filed in the federal district court in Manhattan, alleges that Structured Alpha’s Lead Portfolio Manager, Gregoire P. Tournant, orchestrated the multi-year scheme to mislead investors who invested approximately $11 billion in Structured Alpha, and paid the defendants over $550 million in fees. It further alleges that, with assistance from Co-Lead Portfolio Manager, Trevor L. Taylor, and Portfolio Manager, Stephen G. Bond-Nelson, Tournant manipulated numerous financial reports and other information provided to investors to conceal the magnitude of Structured Alpha’s true risk and the funds’ actual performance.

Defendants reduced losses under a market crash scenario in one risk report sent to investors from negative 42.1505489755747% to negative 4.1505489755747% — by simply dropping the single digit 2. In another example, defendants “smoothed” performance data sent to investors by reducing losses on one day from negative 18.2607085709004% to negative 9.2607085709004% — this time by cutting the number 18 in half.

Publication Date: 17 May 2022

Publication Site: SEC

Excerpt:

The star portfolio manager at the centre of a fraud at the U.S. funds unit of Allianz SE (ALVG.DE) relied on the German insurer’s good name to lure investors and thrived from a lack of oversight as he pocketed $60 million in pay, U.S. authorities said.

Gregoire “Greg” Tournant, a citizen of France and the United States, was indicted on Tuesday for securities fraud, investment adviser fraud, wire fraud and obstruction of justice in a scheme that ran from 2014 to 2020. read more

It was a major development in a two-year saga that has haunted and embarrassed Allianz, one of the globe’s biggest financial firms, and began after the $11 billion in funds managed by Tournant collapsed as markets roiled with the outbreak of the coronavirus in early 2020.

U.S. prosecutors on Tuesday said Tournant faked documents, fabricated risk reports, altered spreadsheets, and lied about the investment strategy.

Author(s): Tom Sims, Alexander Hübner and John O’Donnell

Publication Date: 18 May 2022

Publication Site: Reuters

Link: https://www.ai-cio.com/news/pbgc-approves-bailouts-for-five-more-multiemployer-plans-in-may/

Excerpt:

The Pension Benefit Guaranty Corporation has approved applications submitted to the Special Financial Assistance Program by five more struggling multiemployer plans in May alone. The PBGC has now approved more than $6.2 billion in bailout funds to plans covering close to 120,000 workers and retirees.

The PBGC said it will provide $210.4 million in SFA funding to the Local 365 UAW Pension Fund Pension Plan of Englewood Cliffs, New Jersey, which covers 3,736 participants in the manufacturing industry.

The Local 365 UAW Plan became insolvent in December 2020, at which time the PBGC began providing the plan with financial assistance. As required by law, the plan reduced participants’ benefits to the PBGC guarantee levels, which were approximately 20% below the benefits payable under the terms of the plan.

Author(s): Michael Katz

Publication Date: 23 May 2022

Publication Site: ai-CIO

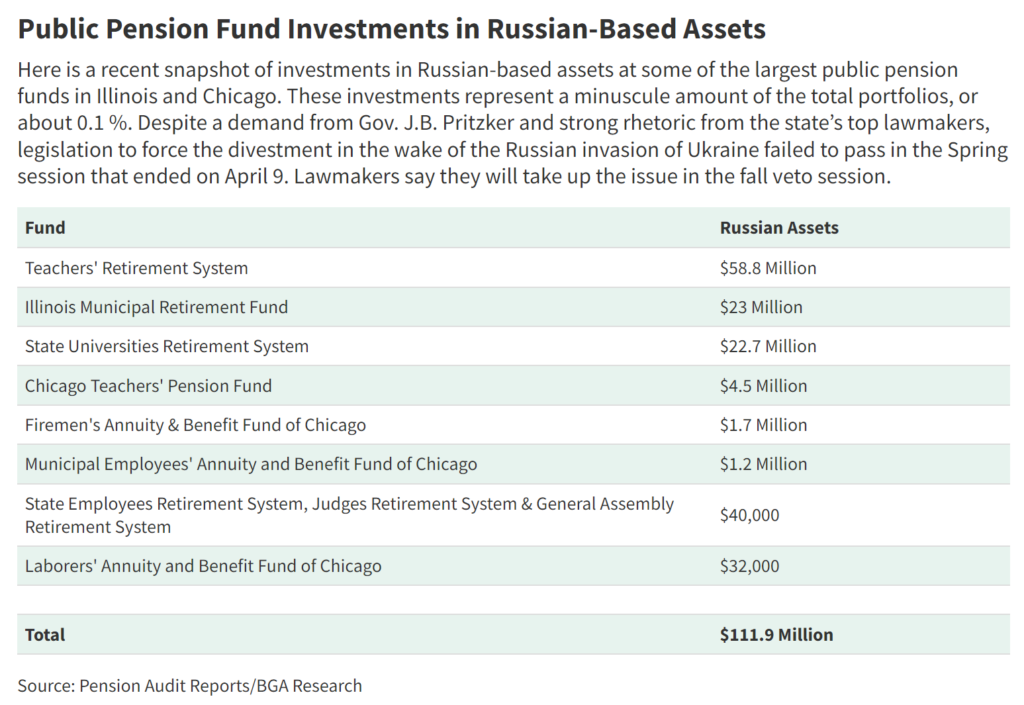

Graphic:

Excerpt:

Despite strong rhetoric from Gov. J.B. Pritzker and other top state officials demanding public pension funds divest more than $100 million in Russia-based assets, state lawmakers now say they won’t act until the Fall veto session.

A key legislative proposal to force the pullout in the wake of the Russian invasion of Ukraine died in a Senate committee awaiting a vote.

Senate President Don Harmon, D-Oak Park, declined to be interviewed for this report, but his staff suggested the Senate had too little time before the session closed on April 9. The House bill — which passed by a vote of 114-0 on April 5 — was never taken up in the Senate chamber.

….

Using pension investment decisions as a way to prompt social change has long been controversial. In the past, Illinois funds have divested from companies and funds related to Sudan, Iran and businesses that boycott Israel following direction from lawmakers.

The Illinois State Board of Investments creates a prohibited list of companies for the funds to consider. The most recent list does not contain companies or funds connected to the Russian invasion.

“How, as a society, should we think about our pension systems assets?” Amanda Kass, Associate Director of the Government Finance Research Center at the University of Illinois – Chicago, asked. “I also see this kind of scrutiny of investing in Russian assets as part of this larger movement.”

Author(s): Jared Rutecki

Publication Date: 5 May 2022

Publication Site: Better Government Association

Link: https://content.naic.org/sites/default/files/capital-markets-hot-spot-equity-markets-may2022.pdf

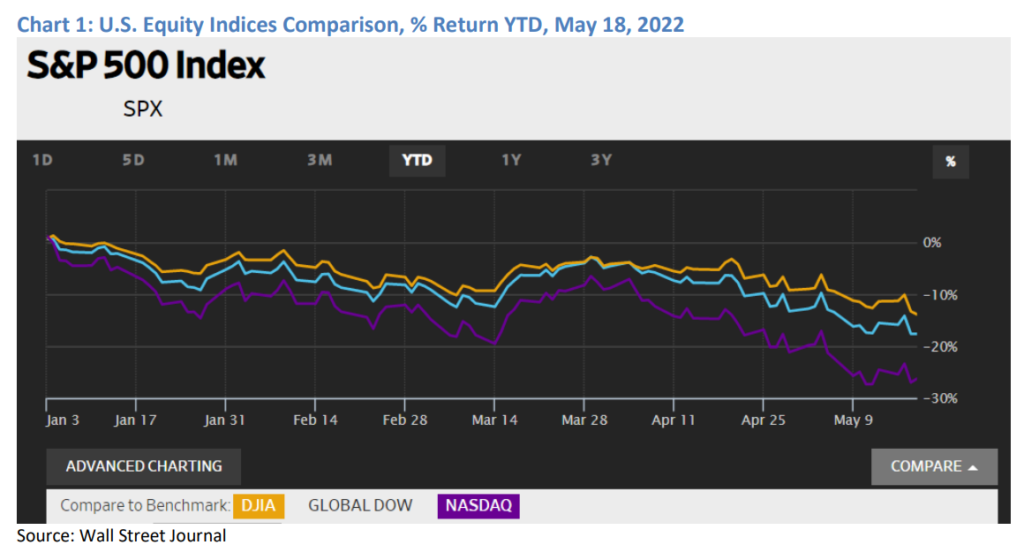

Graphic:

Excerpt:

On May 19, the S&P 500 opened the day near bear market territory; i.e., at a 20% drop from a recent

high. On May 18, the S&P 500 experienced a 4% decline—the largest single-day decrease since June 2020. The last time the S&P 500 entered bear market territory was in March 2020, albeit short-lived, as

the market turned around and headed into a two-year rally that peaked in early January 2022.

The current equity market losses (and some corporate bond losses) are primarily the result of several

factors: 1) earnings reports from large American retailers, including Walmart and Target, show evidence

that the continued high inflation rate may be affecting consumer demand; 2) the war in Ukraine has

added to inflationary pressures, prompting the Federal Reserve (Fed) to increase interest rates and

reduce bond holdings; and 3) recent COVID-19 shutdowns in China have led to a slowdown in the

world’s second largest economy.

Author(s): Jennifer Johnson and Michele Wong

Publication Date: 19 May 2022

Publication Site: NAIC Capital Markets Special Report

Excerpt:

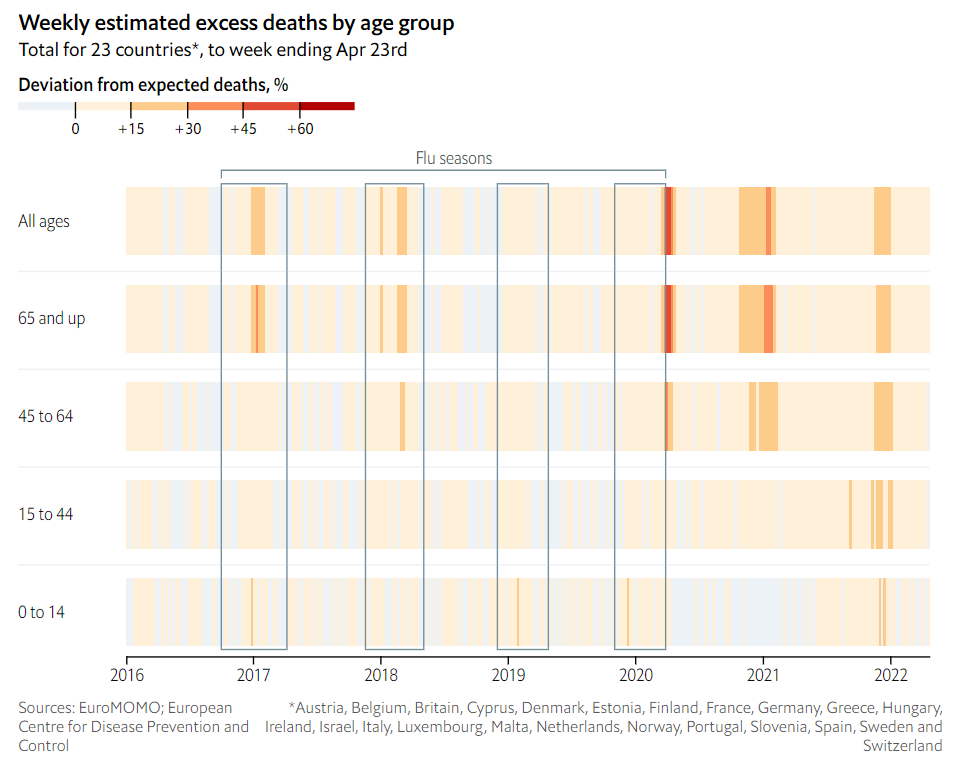

New estimates from the World Health Organization (WHO) show that the full death toll associated directly or indirectly with the COVID-19 pandemic (described as “excess mortality”) between 1 January 2020 and 31 December 2021 was approximately 14.9 million (range 13.3 million to 16.6 million).

“These sobering data not only point to the impact of the pandemic but also to the need for all countries to invest in more resilient health systems that can sustain essential health services during crises, including stronger health information systems,” said Dr Tedros Adhanom Ghebreyesus, WHO Director-General. “WHO is committed to working with all countries to strengthen their health information systems to generate better data for better decisions and better outcomes.”

Excess mortality is calculated as the difference between the number of deaths that have occurred and the number that would be expected in the absence of the pandemic based on data from earlier years.

Excess mortality includes deaths associated with COVID-19 directly (due to the disease) or indirectly (due to the pandemic’s impact on health systems and society). Deaths linked indirectly to COVID-19 are attributable to other health conditions for which people were unable to access prevention and treatment because health systems were overburdened by the pandemic. The estimated number of excess deaths can be influenced also by deaths averted during the pandemic due to lower risks of certain events, like motor-vehicle accidents or occupational injuries.

Publication Date: 5 May 2022

Publication Site: WHO

Graphic:

Excerpt:

The goal of this paper is to equip actuaries to proactively participate in

discussions and actions related to potential racial biases in insurance

practices. This paper uses the following definition of racial bias:

Racial bias refers to a system that is inherently skewed along racial lines.

Racial bias can be intentional or unintentional and can be present in the

inputs, design, implementation, interpretation or outcomes of any system.

To support actuaries and the insurance industry in these efforts, this paper

examines issues of racial bias that have impacted four areas of noninsurance financial services — mortgage lending, personal lending,

commercial lending and the underlying credit-scoring systems — as well

as the solutions that have been implemented in these sectors to address

this bias. Actuaries are encouraged to combine this information on

solutions and gaps in other industries with expertise in their practice areas

to determine how, if at all, this information could be applied to identify

potential racial biases impacting insurance or other industries in which

actuaries work.

Parallels can be drawn between the issues noted here in financial services

and those being discussed within the insurance industry. While many

states have long considered race to be a protected class which cannot be

used for insurance business decisions, regulators and consumer groups

have brought forth concerns about potential racial bias implicit in existing

practices or apparent in insurance outcomes. State regulators are taking

individual actions to address potential issues through prohibition of

certain rating factors, and even some insurers are proactively calling for

the industry to move away from using information thought to be

correlated with race. However, this research suggests that government

prohibition of specific practices may not be a silver-bullet solution.

Actuaries can play a key role as the insurance industry develops

approaches to test for, measure and address potential racial bias, and

increase fairness and equality in insurance, while still maintaining riskbased pricing, company competitiveness and solvency.

Author(s): Members of the 2021 CAS Race and Insurance Research Task Force

Publication Date: March 2022

Publication Site: CAS

Graphic:

Excerpt:

Insurance rating characteristics have come under scrutiny by legislators and

regulators in their efforts to identify and address racial bias in insurance

practices. The goal of this paper is to equip actuaries with the information

needed to proactively participate in industry discussions and actions related

to racial bias and insurance rating factors. This paper uses the following

definition of racial bias:

Racial bias refers to a system that is inherently skewed along racial lines.

Racial bias can be intentional or unintentional and can be present in the

inputs, design, implementation, interpretation, or outcomes of any system.

This paper will examine four commonly used rating factors in personal

lines insurance — credit-based insurance score, geographic location, home

ownership, and motor vehicle records — to understand how the data

underlying insurance pricing models may be impacted by racially biased

policies and practices outside of the system of insurance. Historical issues

like redlining and racial segregation, as well as inconsistent enforcement of

policies and practices contribute to this potential bias. These historical

issues do not necessarily change the validity of the actuarial approach of

evaluating statistical correlation of rating factors to insurance loss overall.

Differences in the way individual insurers build rating models may produce

very different end results for customers. More data and analyses are

needed to understand if and to what extent these specific issues of racial

bias impact insurance outcomes. Actuaries and other readers can combine

this information with their own subject matter expertise to determine if and

how this could impact the systems for which they are responsible, and what

actions, if any, could be taken as a result.

Author(s): Members of the 2021 CAS Race and Insurance Research Task Force

Publication Date: March 2022

Publication Site: CAS

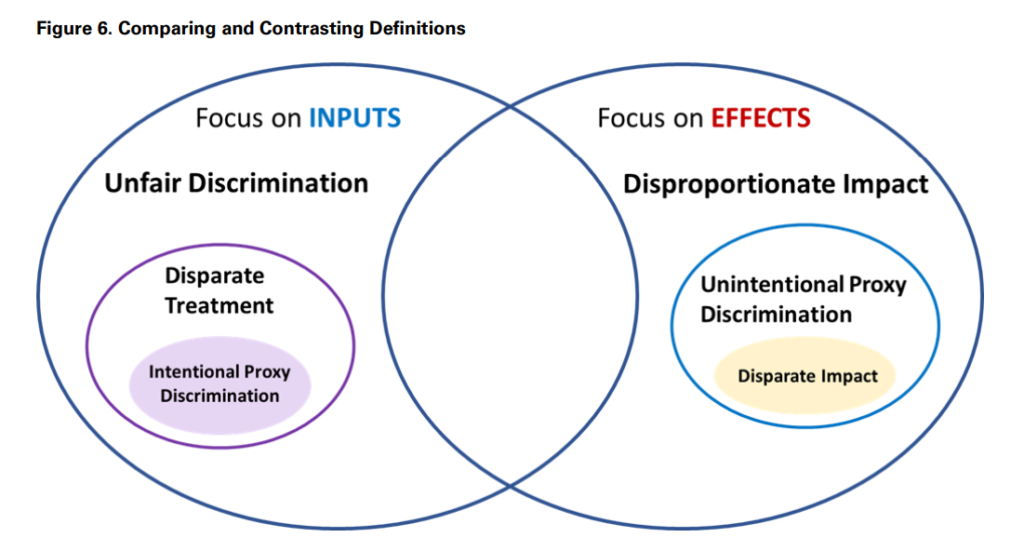

Graphic:

Excerpt:

This research paper is designed to introduce various terms used in defining

discrimination by stakeholders in the insurance industry (regulators, consumer

advocacy groups, actuaries and insurers, etc.). The paper defines protected class,

unfair discrimination, proxy discrimination, disproportionate impact, disparate

treatment and disparate impact.

Stakeholders are not always consistent in their definitions of these terms, and

these inconsistencies are highlighted and illustrated in this paper. It is essential to

elucidate key elements and attributes of certain terms as well as conflicting

approaches to defining discrimination in insurance in order to move the industry

discussion forward.

While this paper does not make a judgment on the appropriateness of the

definitions put forth, nor does it promulgate what the definitions should be,

readers will be empowered to understand the components of discrimination terms

used in insurance, as well as be introduced to the potential implications for

insurers.

Actuaries who have a strong foundational knowledge of these terms are likely to

play a key role in informing those who define and refine these terms for insurance

purposes in the future. This paper is not a legal review, and thus discusses terms

and concepts as they are used by insurance stakeholders, rather than what their

ultimate legal definition will be. However, it is important for actuaries to

understand the point of view of various stakeholders, and the potential impact it

could have on actuarial work. As the regulatory and legislative landscape

continues to shift, this brief should be considered a living document, that will

periodically require update.

Author(s): Kudakwashe F. Chibanda, FCAS

Publication Date: March 2022

Publication Site: CAS

Link: https://www.investopedia.com/race-and-insurance-5224764

Excerpt:

Two new papers from property casualty actuaries delve into issues of historical and ongoing bias in insurance pricing.

These papers are on potential Influences among four rating factors and attempts to actually define discrimination in insurance.

Factors such as geography, credit scoring, home ownership, and motor vehicle records affect homeowners and auto insurance rates and can cause Black consumers to pay higher premiums.

Actuaries and regulators are trying to untangle factors from societal prejudice for fairer pricing

AI or machine learning can augment or amplify these biases with their vast inputs, and data scientists will be analyzing outcomes for discriminatory pricing effects.

States have been taking action through regulation or pending legislation to extinguish some factors that can lead to racial bias or to examine data modeling to check for discriminatory effects.

Author(s): ELIZABETH FESTA

Publication Date: 5 April 2022

Publication Site: Investopedia

Graphic:

Excerpt:

As covid-19 has spread around the world, people have become grimly familiar with the death tolls that their governments publish each day. Unfortunately, the total number of fatalities caused by the pandemic may be even higher, for several reasons. First, the official statistics in many countries exclude victims who did not test positive for coronavirus before dying—which can be a substantial majority in places with little capacity for testing. Second, hospitals and civil registries may not process death certificates for several days, or even weeks, which creates lags in the data. And third, the pandemic has made it harder for doctors to treat other conditions and discouraged people from going to hospital, which may have indirectly caused an increase in fatalities from diseases other than covid-19.

One way to account for these methodological problems is to use a simpler measure, known as “excess deaths”: take the number of people who die from any cause in a given region and period, and then compare it with a historical baseline from recent years. We have used statistical models to create our baselines, by predicting the number of deaths each region would normally have recorded in 2020 and 2021.

Many Western countries, and some nations and regions elsewhere, regularly publish data on mortality from all causes. The table below shows that, in most places, the number of excess deaths (compared with our baseline) is greater than the number of covid-19 fatalities officially recorded by the government. The full data for each country, as well as our underlying code, can be downloaded from our GitHub repository. Our sources also include the Human Mortality Database, a collaboration between UC Berkeley and the Max Planck Institute in Germany, and the World Mortality Dataset, created by Ariel Karlinsky and Dmitry Kobak.

Publication Date: last updated 13 May 2022

Publication Site: The Economist