Blackstone loves managing assets for insurers, but it has no interest in assuming a large amount of investment risk itself.

Blackstone Executives talked about the skin-in-the-game idea Thursday, during a conference call the company held to go over first-quarter earnings with securities analysts.

Patrick Davitt, an analyst with Autonomous Research, asked Blackstone executives Thursday about reports that some insurance regulators have concerns about independent money managers’ role in handling insurers’ investments.

“Some observers have suggested that an outcome of these reviews could be a requirement of more skin in the game for the managers, particularly those that aren’t consolidated with their insurance counterparties,” Davitt said. “So, first, what is your position on this focus? Do you think there’s a risk that regulators will require more skin in the game?”

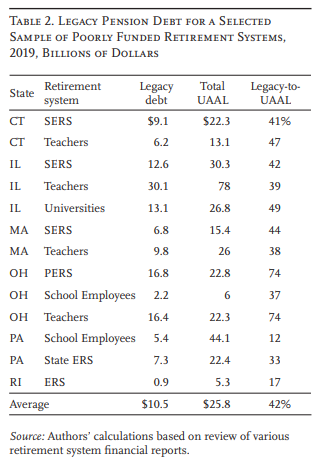

State and local policymakers face a growing pension cost burden, but often lack understanding of the root causes.

One underappreciated cause is “legacy debt” – unfunded liabilities accumulated long ago, before plans adopted modern funding practices.

Legacy debt still exists today because historical unfunded liabilities were ultimately paid in full using some of the money intended to fund later benefits.

In a sample of plans with particularly low funded ratios, legacy debt averaged more than 40 percent of unfunded liabilities.

A failure to recognize the legacy debt has provided misleading information about benefit generosity, hindering progress toward effective solutions.

Author(s): Jean-Pierre Aubry

Publication Date: April 2022

Publication Site: Center for Retirement Research at Boston College

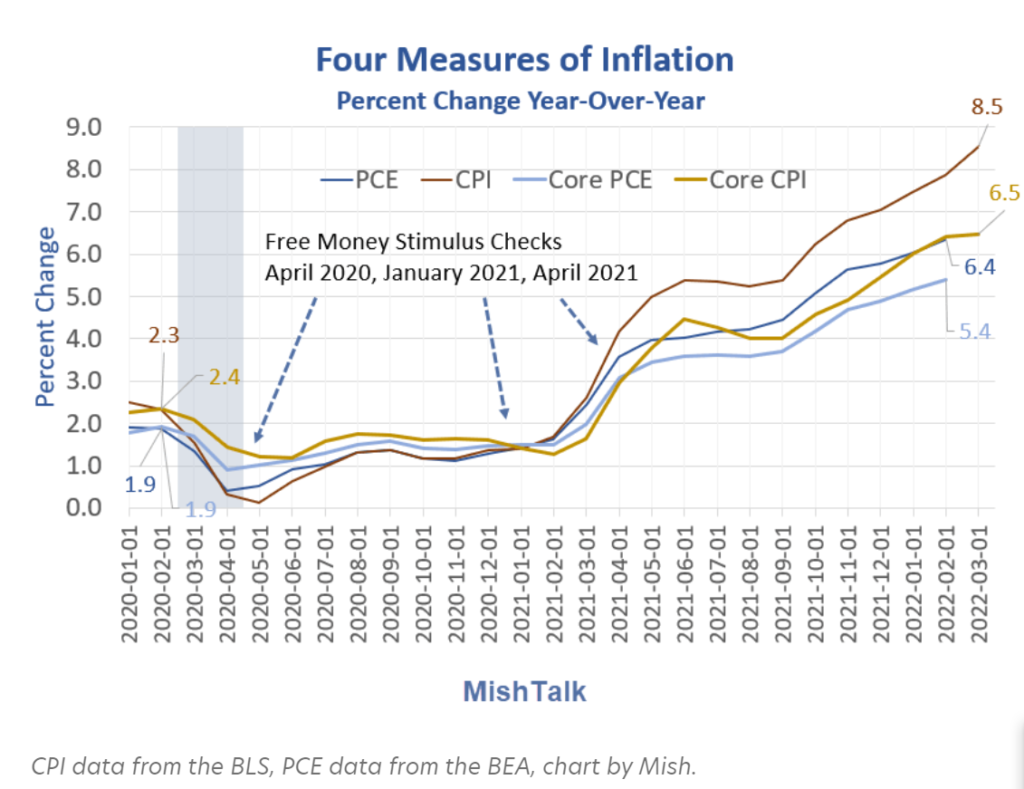

The question is not as straight forward as it looks. The gap between spending and income isn’t constant.

Free money that goes to bottom rung households tends to immediately get spent. The higher the rung, the more the savings. This is complicated by the fact that most of the money was supposed to go to lower tiers, and further complicated by corporate fraud, especially in round one.

More importantly, personal spending does not count mortgage paydowns, stock market or Bitcoin purchases, capital expenses for businesses, drug money, other illegal uses, or money sent to relatives overseas.

….

The Peterson Foundation reports direct checks were $292 billion in round one, $164 billion in round two, and $411 billion in round three.

There was $850 billion of direct payments to taxpayers with the biggest and most unwarranted round the last.

Spending data suggests free money, at least most of direct payments, already did enter the economy.

However, that does not factor in unpaid rent via eviction moratoriums or SNAP (Supplemental Nutrition Assistance Program), formerly Food Stamps, which I will address in a separate post.

So yes, there still could be a pile of unspent stimulus savings, possibly much higher than my $2 trillion summation estimate, again with my caveats on investments, sending money overseas, etc.

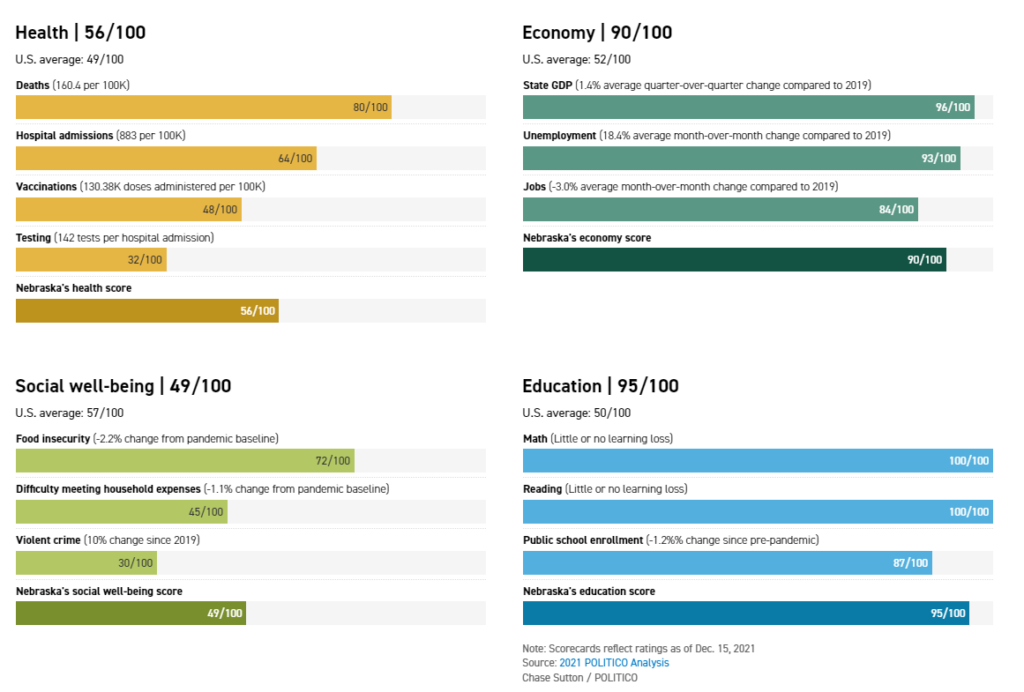

This conversation about protecting hospitals, back in the era when New Yorkers were still being encouraged to go to restaurants, well before the coasts’ contagion began closing in on the Midwest in earnest, helped define what became, by some measures, one of the most effective and balanced Covid responses in the United States. Ricketts is a mandate-shunning Republican who runs a heavily Republican and rural state with a middling vaccination rate — factors that have been linked to worse pandemic health outcomes in other states. He never ordered a statewide shutdown when 43 other governors, Democrats and Republicans, did so; he has stood against, or even supported lawsuits over, local mask requirements; he has told state agencies not to comply with federal vaccine mandates and gotten scolded by the U.S. secretary of defense for objecting to such requirements for the National Guard. And yet by the fall of last year, when POLITICO crunched the data of state pandemic responses on a combination of health, economic, social and educational factors, one state came out with the best average: Nebraska.

The state had the best economic performance of any in the pandemic up to that point, and its students, according to available data, appear to have suffered little to no learning loss. Whereas many states saw a trade-off between health and wealth in the pandemic — often corresponding to more-restrictive Democratic leadership and less-restrictive Republican leadership, respectively — Nebraska also scored above the national average for health outcomes POLITICO evaluated last year (20th of 50 states). Nebraska was the first state to accumulate a 120-day stockpile of PPE in the nationwide scramble for supplies; was a national leader in opening schools; and was among the quickest getting federal aid to small businesses. As of now, its cumulative pandemic death toll per capita is near the lowest of all 50 states, according to the Kaiser Family Foundation. This, however, is grading on a hideous curve in a country that hasn’t managed the pandemic well in general: More than 4,000 Nebraskans have lost their lives to Covid. Lawler of the University of Nebraska Medical Center, who helped design the state’s early Covid response but has since grown critical of Nebraska’s approach, notes that South Korea has 14 times lower per capita Covid mortality than Nebraska. “Nobody,” he told me via text, “should be patting themselves on the back for doing 14 [times] worse.”

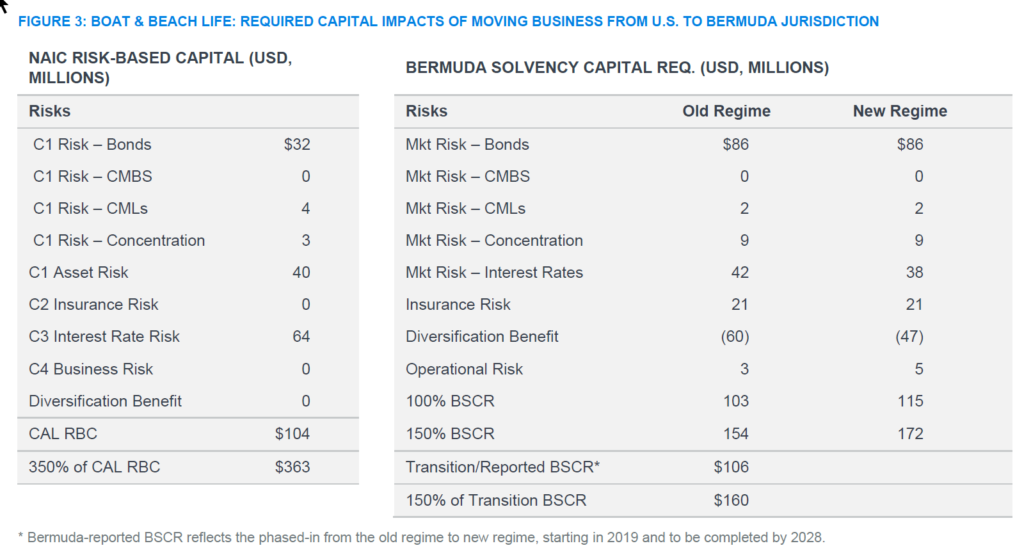

We review the history of life insurance in Bermuda, reflect on how we have gotten to where we are today, and look forward to what may be ahead. We present a hypothetical—yet realistic—case study to illustrate some of the factors that can lead to a strategic decision do business Bermuda. From an embedded-value perspective, we highlight potentially considerable benefits from a move from a U.S. statutory basis to a Bermudian economic balance sheet.

Author(s): Tony Dardis, William C. Hines, and Su Meng Lee

Total Russian and Ukraine sovereign and corporate debt was $813.3 million at year-end 2021, representing 97% of total exposure; the remainder comprised $28.8 million in stocks (see Table 2). While life companies accounted for the majority of the bond exposure at $683.9 million (or 84% of total Russia and Ukraine bonds), property/casualty (P/C) companies accounted for almost all the Russia and Ukraine stock exposure at $28 million. About 90% of U.S. insurers’ exposure to Russia and Ukraine bonds and stocks was held by large companies, or those with more than $10 billion assets under management.

Author(s): Jennifer Johnson, Michele Wong, Jean-Baptiste Carelus

Publication Date: 14 Apr 2022

Publication Site: NAIC Capital Markets Special Reports

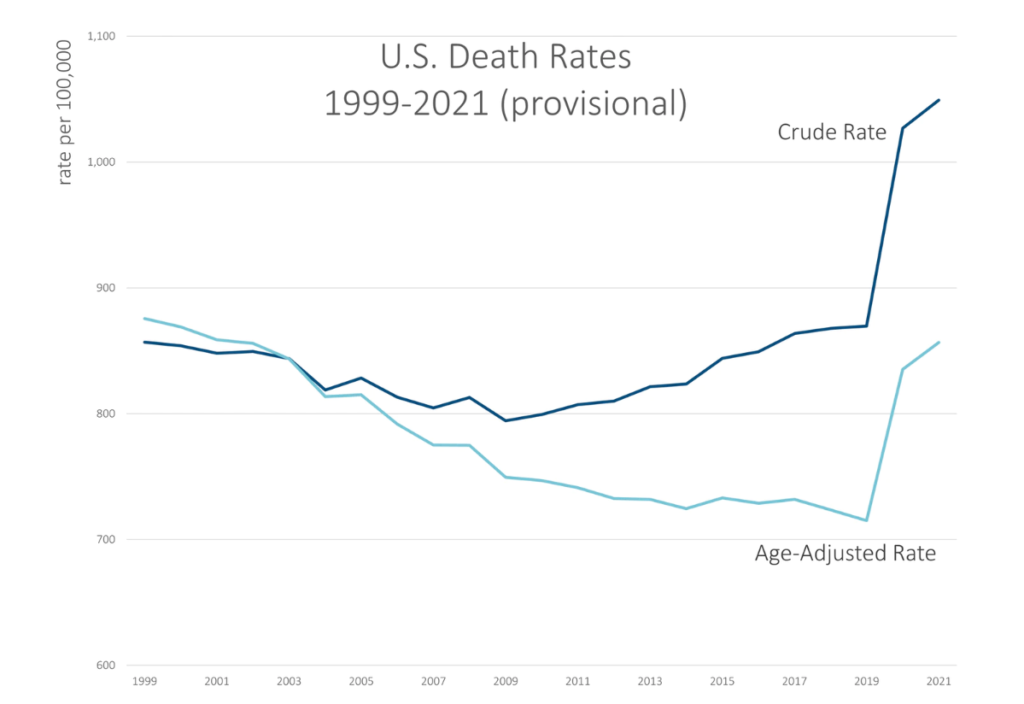

Here’s a graph for 1999 through the provisional 2021 result (as of 3 April 2022 data from CDC WONDER):

You can see the crude rate is higher than the age-adjusted rate for most of the years, and that’s due to the aging of the population. Basically, the Boomers have been getting older, and their older ages (and higher mortality compared to where they were in 2000), have an effect on how many deaths there are overall — thus the crude rate continually increasing as there are more and more old people.

However, until the pandemic hit, the age-adjusted death rate in general decreased, though we had a few years in the 2010s in which the age-adjusted death rate did increase… and yes, that was due to drug overdoses. We will get to that in a bit.

In any case, both the crude rate and age-adjusted rates did jump up by a lot in 2020 due to the pandemic, and COVID deaths were even higher in 2021. But there were other causes of death also keeping mortality rates high in 2021.

I will point out that even with all this extra mortality, the age-adjusted death rate in 2021 is still below where it was in 1999.

That does not mean things are hunky-dory.

This is one of the dangers of collapsing death rates into a single number. The increase in death rates has differed by age group, and it has been far worse for teens and young adults through even young middle-age than it has been for the oldest adults.

Yes, COVID has killed the oldest adults the most, but their death rates have increased the least. It’s all relative.

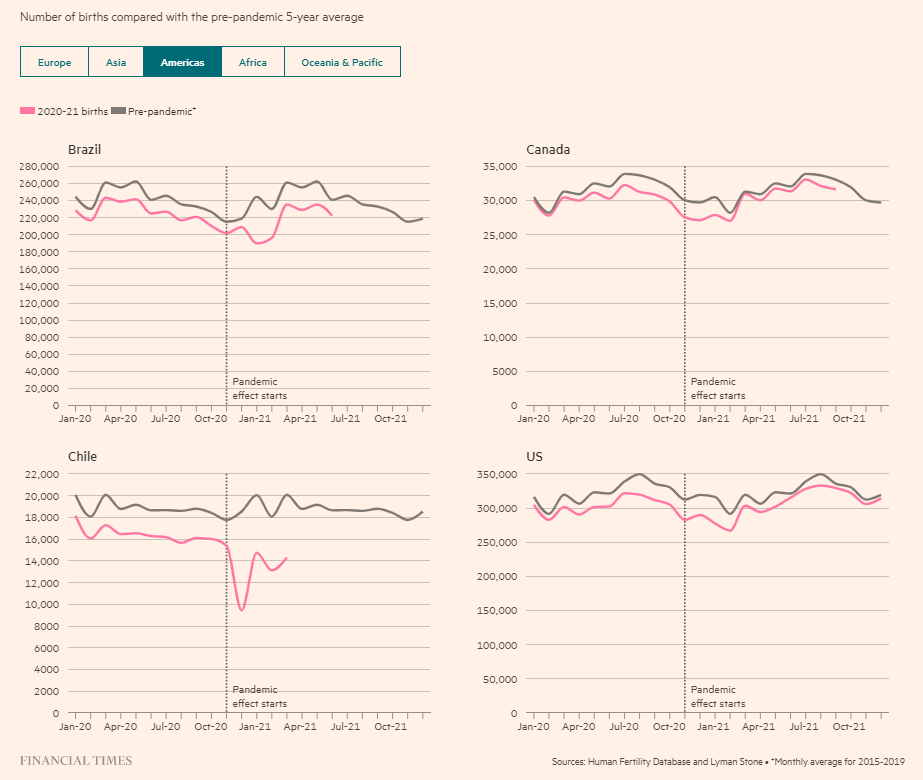

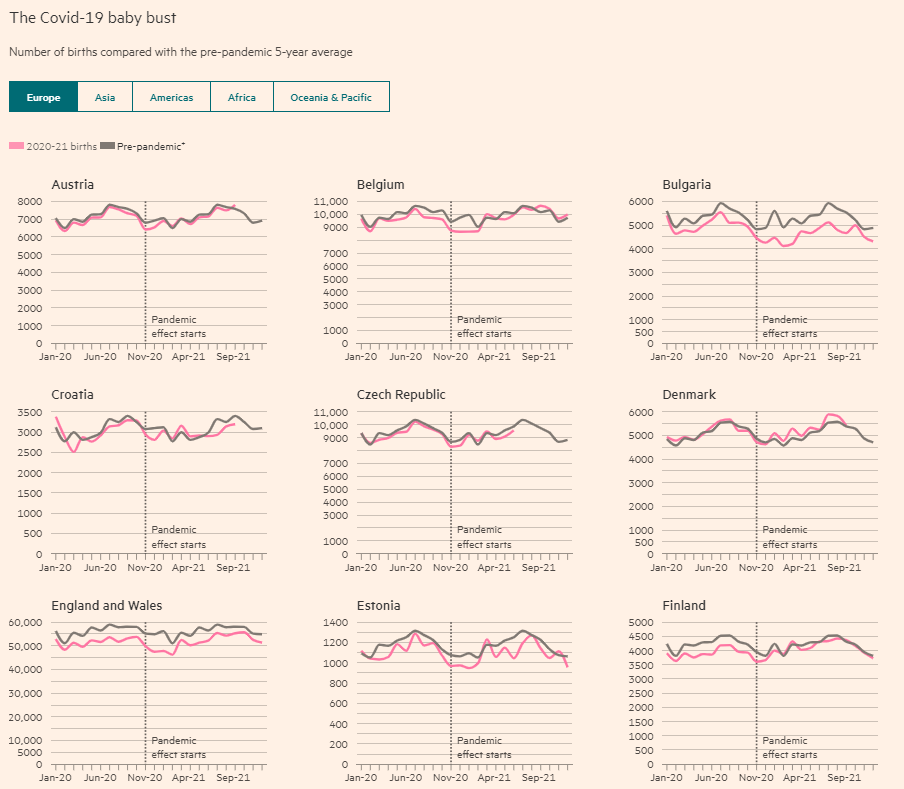

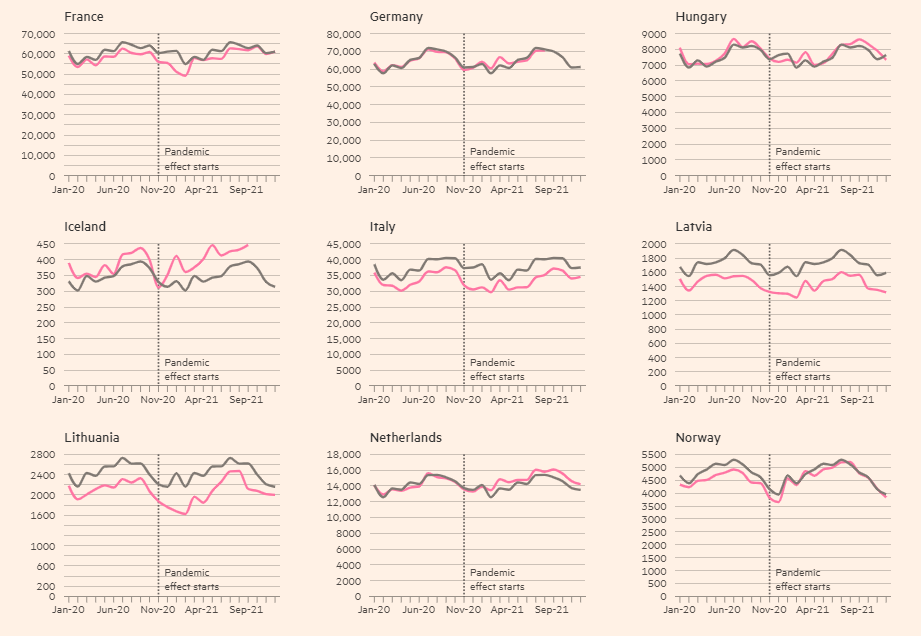

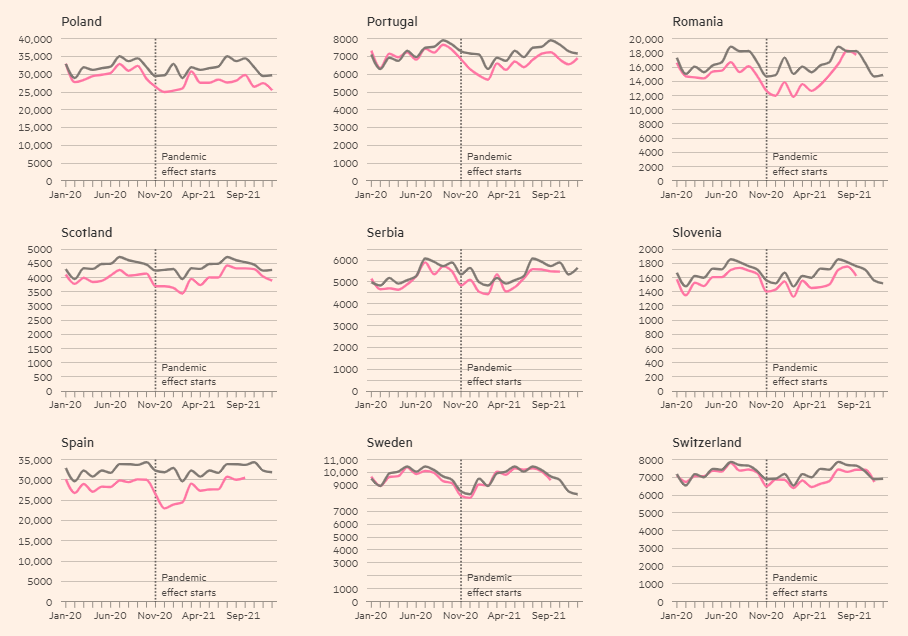

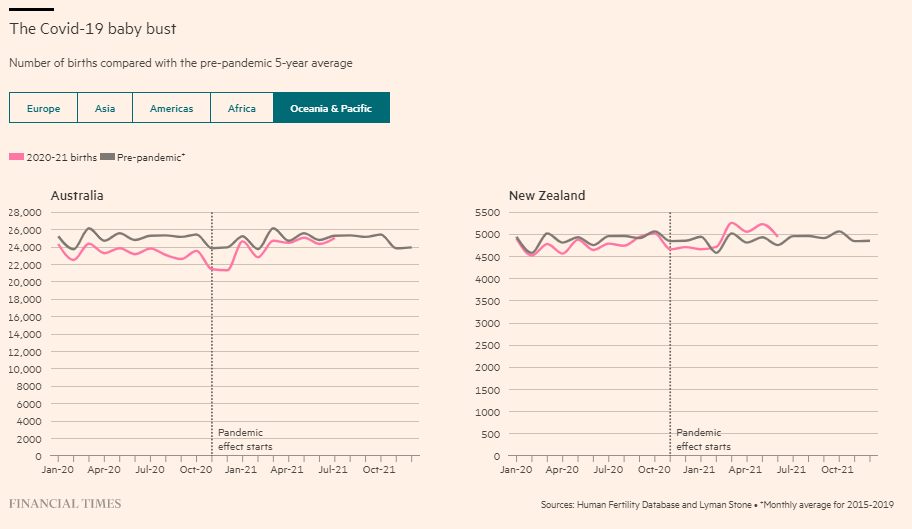

The number of births in advanced economies has largely rebounded to levels before the coronavirus pandemic, a Financial Times analysis shows, a recovery that experts say was partly because of stimulus policies deployed to mitigate the economic impact of the crisis.

Births began to fall sharply in late 2020 after Covid-19 took hold and people were confined to their homes in lockdown, worsening an already perilous demographic trend of population decline in wealthy nations.

The trend mirrored drops during the 1918 flu pandemic, the Great Depression and the global financial crisis in 2008. But an analysis of national data shows a rapid rebound in most developed countries.

…..

The global fertility rate peaked at five in 1960 and has since been in freefall. As a result, demographers believe that, after centuries of booming population growth, the world is on the brink of a natural population decline.

According to a Lancet paper published in 2020, the world’s population will peak at 9.7bn in about 2064, dropping to 8.7bn around the end of the century. About 23 nations can expect their populations to halve by 2100: Japan’s population will fall from a peak of 128mn in 2017 to less than 53mn; Italy’s from 61mn to 28mn.

Low fertility rates set off a chain of economic events. Fewer young people leads to a smaller workforce, hitting tax receipts, pensions and healthcare contributions.

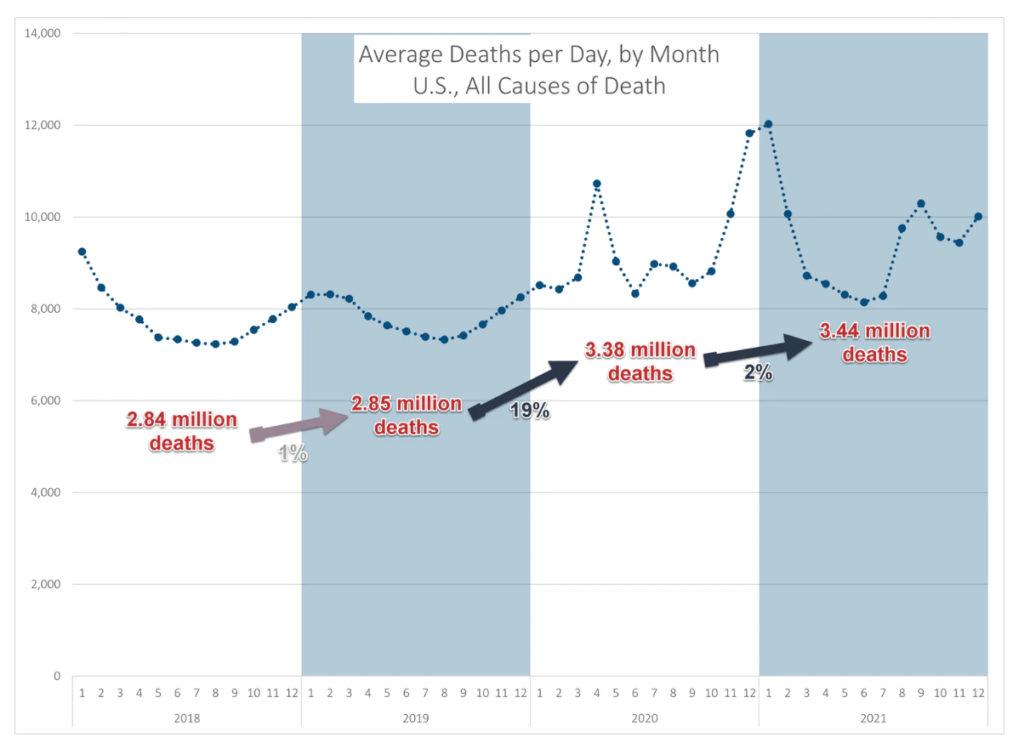

As you can see from the annotation on the graph, so far there have been 2% more deaths reported in 2021 compared to 2020. You can see that there had been a spike of deaths at the beginning of 2021, then a quiet spring/early summer. I did not extend my graph into 2022, but the heightened mortality of later/summer fall into winter has continued into winter at the beginning of 2022.

For the record, the 1% increase in deaths from 2018 to 2019 was pretty common before, driven by regular growth of the aging population of the U.S.

The insurance industry is unique in that the cost of its products—insurance policies—is unknown at the time of sale. Insurers calculate the price of their policies with “risk-based rating,” wherein risk factors known to be correlated with the probability of future loss are incorporated into premium calculations. One of these risk factors employed in the rating process for personal automobile and homeowner’s insurance is a credit-based insurance score.

Credit-based insurance scores draw on some elements of the insurance buyer’s credit history. Actuaries have found this score to be strongly correlated with the potential for an insurance claim. The use of credit-based insurance scores by insurers has generated controversy, as some consumer organizations claim incorporating such scores into rating models is inherently discriminatory. R Street’s webinar explores the facts and the history of this issue with two of the most knowledgeable experts on the topic.

Featuring:

[Moderator] Jerry Theodorou, Director, Finance, Insurance & Trade Program, R Street Institute Roosevelt Mosley, Principal and Consulting Actuary, Pinnacle Actuarial Services Mory Katz, Legacy Practice Leader, BMS Group

R Street Institute is a nonprofit, nonpartisan, public policy research organization. Our mission is to engage in policy research and outreach to promote free markets and limited, effective government.

We believe free markets work better than the alternatives. We also recognize that the legislative process calls for practical responses to current problems. To that end, our motto is “Free markets. Real solutions.”

We offer research and analysis that advance the goals of a more market-oriented society and an effective, efficient government, with the full realization that progress on the ground tends to be made one inch at a time. In other words, we look for free-market victories on the margin.