The Bank of England has fined Standard Chartered £46.5m for repeatedly misreporting its liquidity position and for “failing to be open and cooperative” with the regulator.

The Bank’s Prudential Regulation Authority (PRA) said Standard Chartered had made five errors in reporting an important liquidity metric between March 2018 and May 2019, which meant the watchdog did not have a reliable overview of the bank’s US dollar liquidity position.

…..

One of the errors occurred in November 2018, as a result of a mistake in a spreadsheet entry. A positive amount was included when a zero or negative value was expected, leading to an $7.9bn (£6bn) over-reporting of the bank’s dollar liquidity position.

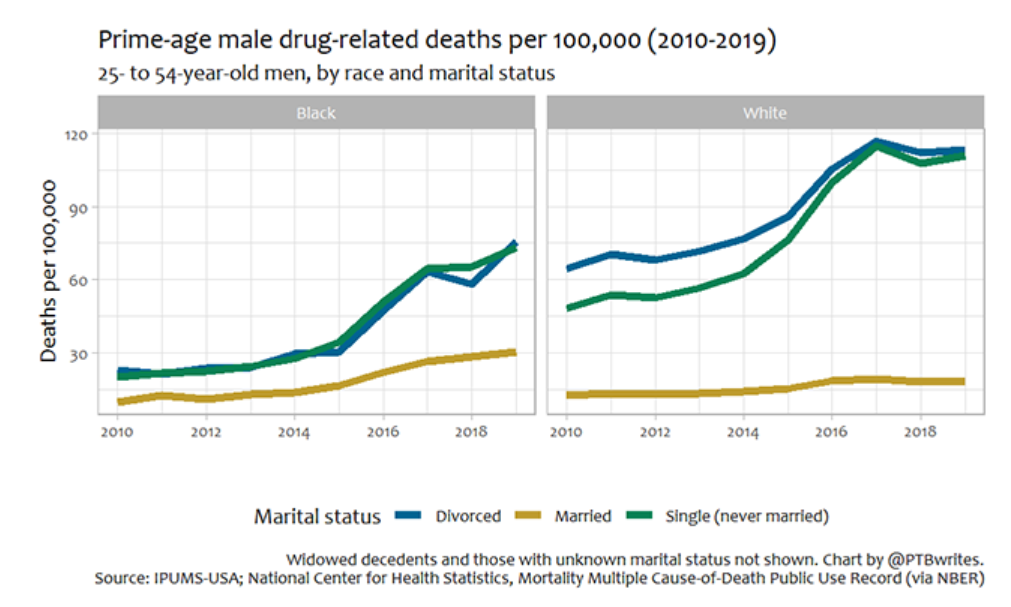

From 2010 to 2019, the drug-related death rate among never-married prime-age white men increased some 125 percent: from 52 deaths per 100,000 to 117 (including 2020 would show an even steeper rise, but the pandemic affected Census data collection). If single and divorced prime-age white men had seen opioid deaths rise by only the same rate as those deaths rose among their married counterparts, the U.S. would have seen 38,800 fewer deaths from drug-related causes over the past decade just among this demographic group.

A marriage certificate is no prophylactic against the scourge of drug overdoses, of course. Marital status is correlated with income, race, and age; while death certificates don’t report income, we know that married decedents are more likely to be white, older, and better-educated. Controlling for those factors still shows single men to be at greater risk of dying from drug-related causes than married ones.

The number of COVID-19 deaths in Michigan nursing homes is 42 percent larger than Democratic governor Gretchen Whitmer’s administration disclosed, according to a state auditor general’s report reviewed by the Washington Free Beacon.

The report, which Auditor General Doug Ringler is set to release in full next week, shows 8,061 COVID-19 deaths in the state’s long-term care facilities from Jan. 1, 2020, to July 2, 2021. That number is 42 percent larger than the 5,675 deaths Whitmer’s health department reported.

A requirement to have paid into the system is characteristic of a social insurance program, and the 10 year contribution requirement is essentially the same as the eligibility requirement for Old Age benefits in Social Security. However, true social insurance programs pay out benefits to those eligible regardless of residence — again, once you’ve paid into Social Security long enough to have earned your benefit, you can collect regardless of where you live, even if you have moved abroad. In fact, even noncitizens who worked in the United States long enough to have accumulated sufficient Social Security credits, can receive benefits after having moved back to their home countries. What’s more, many social insurance systems provide some sort of refund mechanism for workers who do not accumulate enough contribution years to be eligible.

And this hybrid system will likely prove to be unsustainable politically. Even if ordinary Washingtonians are not well-versed in social insurance concepts and theories, it will not sit right with them that those who retire with 10 years of payroll taxes have “earned” their benefits but those with 9 years have not, and, likewise, that those who have “earned” benefits would lose those “earned” benefits merely by moving out of state. How precisely this will play out over the long term remains to be seen, but the new bills are not likely to be the end of the story.

In any case, these problems will not be easy to remedy.

But one of my very smart readers did go through it and reached out to me yesterday…

Hi Rich,

Long time follower, first time writer. In full disclosure, I recently retired from the [redacted] after more than [redacted] years. I just read the COGFA article today and was encouraged about the State’s finances yet again.

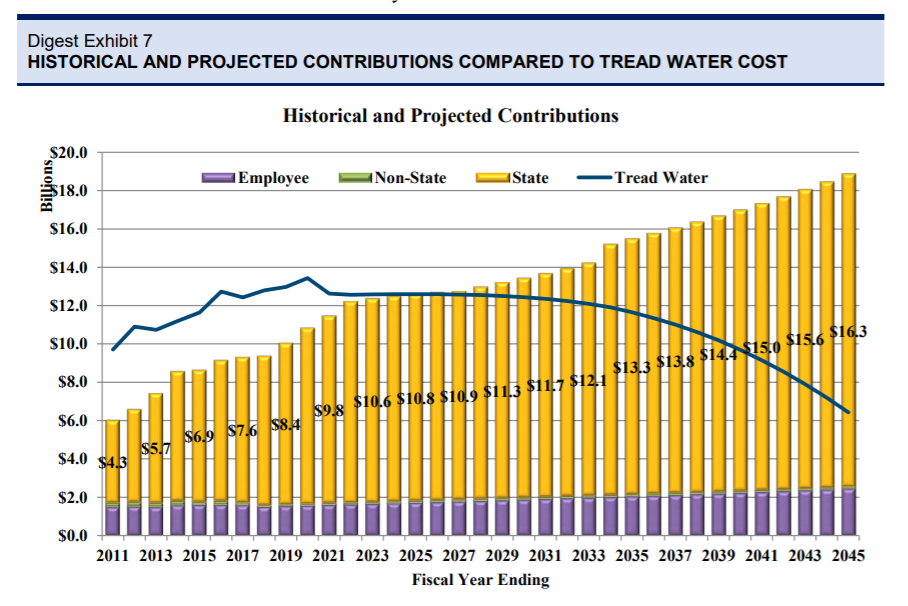

Another report that came out in late December that received no coverage was the State Actuary Report (see link below). The unheralded news in this report was that there were several State pension systems that passed the “Tread Water” point in FY21; meaning we are now paying in more than we owe and reducing the liability for those systems.

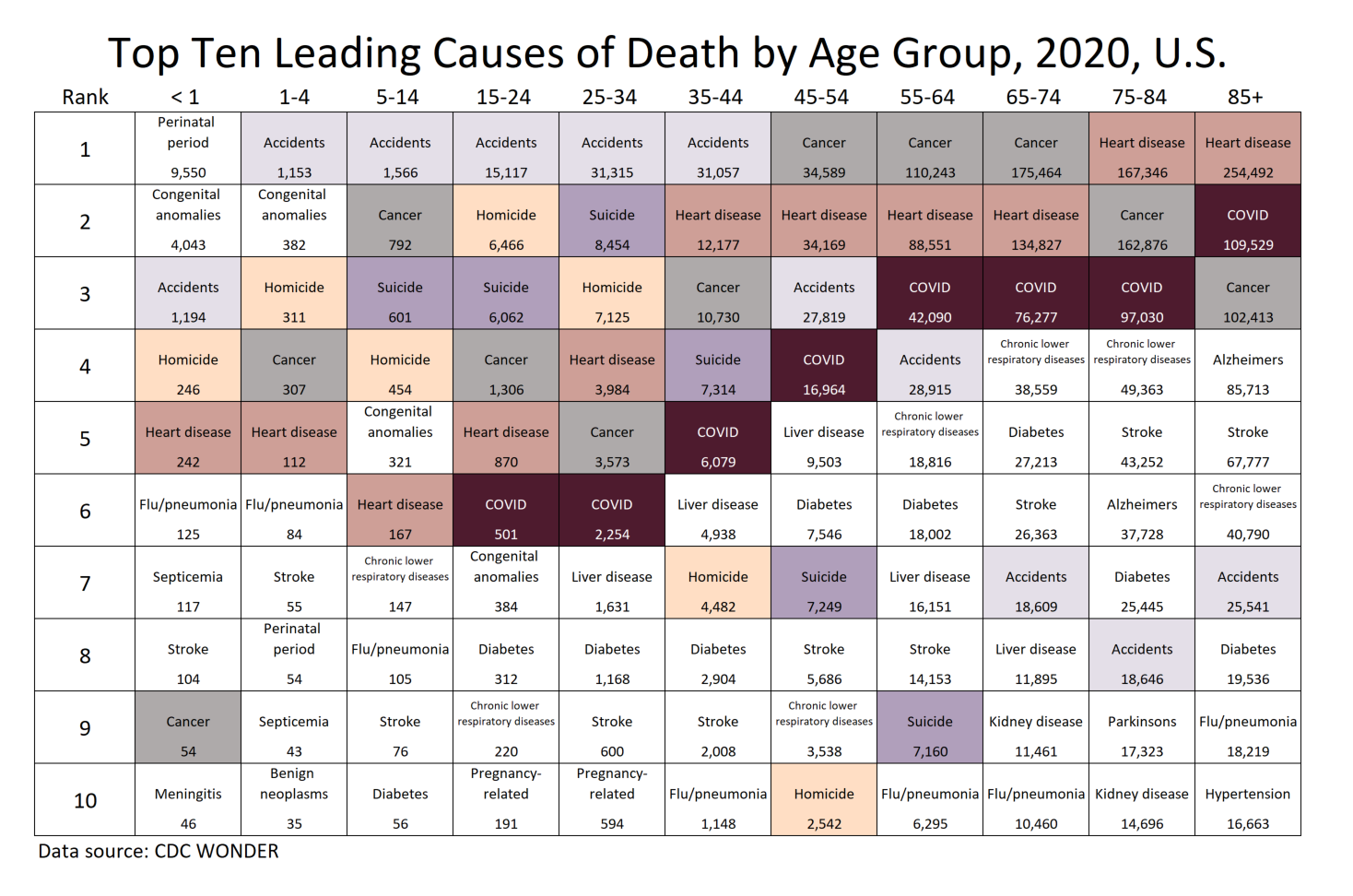

The numbers below each cause are the total number of finalized deaths in CDC Wonder as of 11 January 2022 for the completed calendar year 2020.

COVID deaths for under age 15 weren’t in the top 10 causes for those age groups, which is why they aren’t seen in the table. But you may be interested in those numbers: at #12 for ages 5-14, with 49 deaths at #12 for ages 1-4, with 19 deaths at #13 for infant mortality (<1 year), at 35 deaths

In general, other than the new cause of COVID, most of the causes of death were in the same rank order as in 2019, with a few switches for causes that tend to be close in numbers.

If we’re trying to prevent Covid surges and end the pandemic, then we need to center the population in our thinking. Health authorities need to get tools like rapid tests and better masks to as many people as possible, especially those who are more likely to spread disease, even if they’re at low risk themselves. People need to be persuaded or incentivized to vaccinate to protect others.

If you are sick, even with severe Covid, you want someone with a doctor’s viewpoint caring for you. America, however, is not a patient. And we’d all be better off, as a society and as individuals, if those in control of our country’s health stopped thinking of it that way.

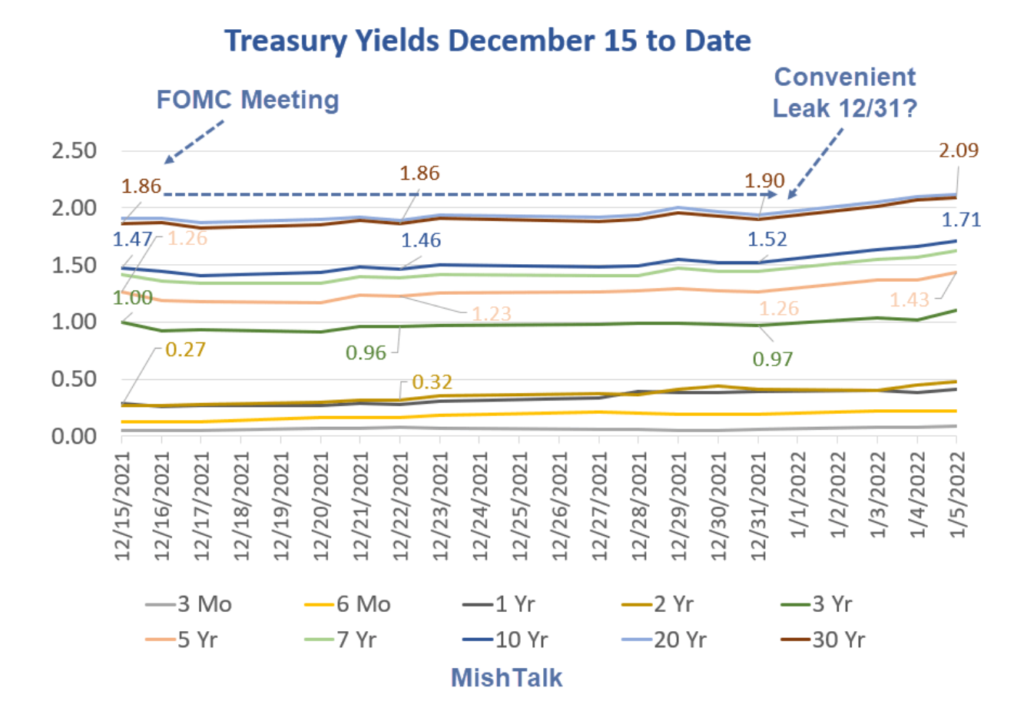

In what is the product of the sustained low-rate environment, many municipalities are considering addressing their pension position through bonds. This should be encouraged by policymakers and explored by pension systems.

Bond markets are offering municipalities the opportunity to exchange discount rates of 6, 7 and sometimes even 8 percent for bonds with yields below 3 percent. The spread between the discount rate and the bond yield is the root of the appeal of pension obligation bonds.

A U.S. judge on Wednesday narrowed but refused to dismiss a Securities and Exchange Commission lawsuit accusing Morningstar Inc. of letting analysts adjust credit rating models for about $30 billion of mortgage securities, resulting in lower payouts to investors.

U.S. District Judge Ronnie Abrams in Manhattan said the SEC plausibly alleged that Morningstar Credit Ratings failed to provide users with a general understanding of its methodology for rating commercial mortgage-backed securities and lacked effective internal controls over its ratings process.