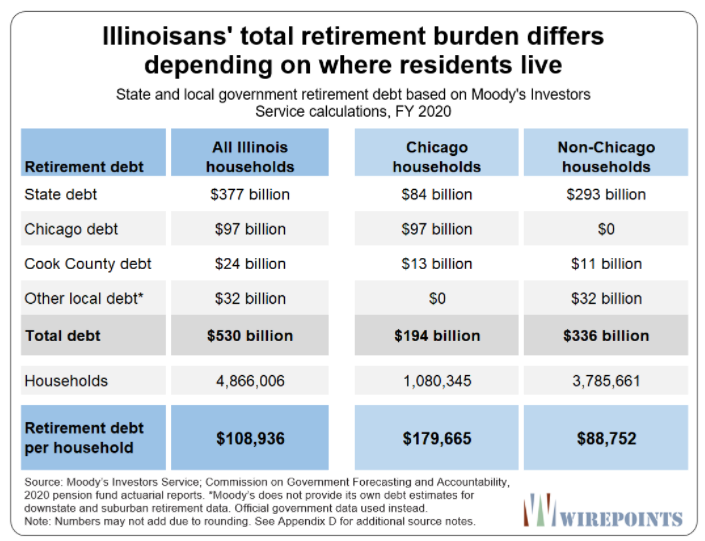

The $110,000 per household is an average across the entire state, but the precise burden for Illinoisans differs depending on where they live. The debt burden on Chicago’s one million households is larger because of the city’s deeper debt crisis. There, each household is on the hook for $180,000 for their share of state and local retirement debts.

Illinoisans living outside of Chicago, meanwhile, face an overall average burden of $90,000 per household. For comparison purposes, the burdens for Chicago and non-Chicago households, based on official state and local retirement debts, are $95,000 and $53,000, respectively.

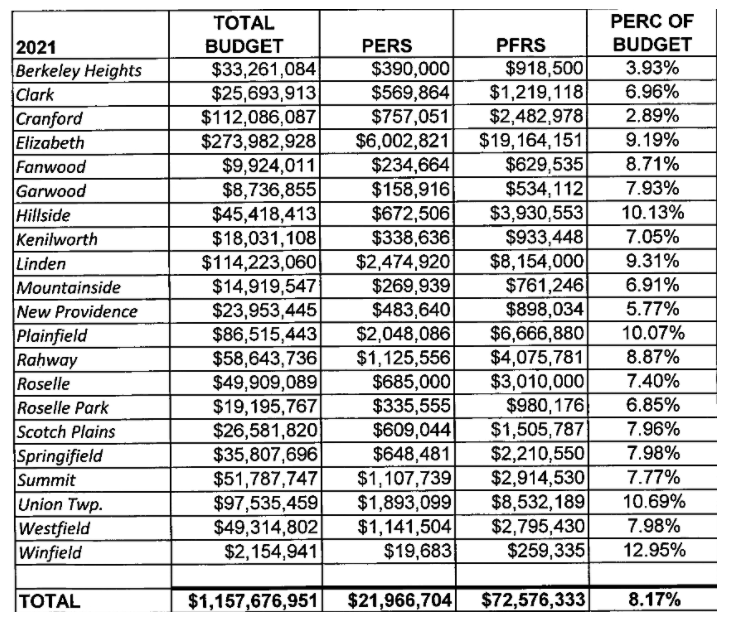

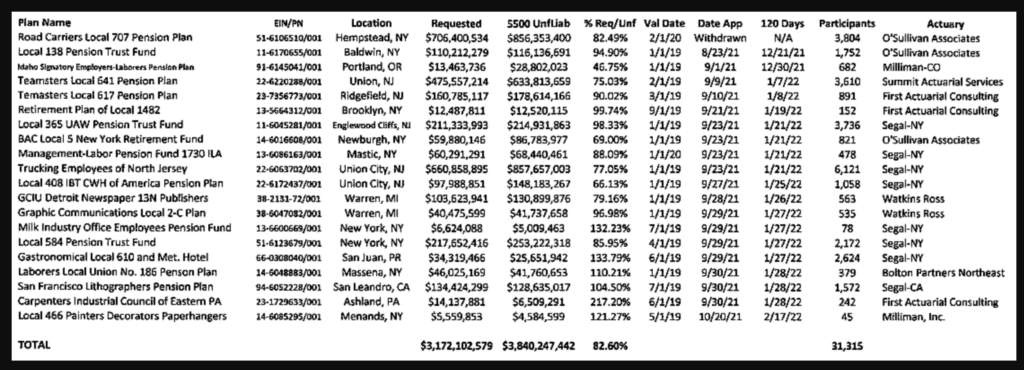

Over at countywatchers I have a series comparing 2021 budget items for the municipalities in Union County and part 4 relates to this blog so here it is.

Comparing pension records to 2021 budget allocations that municipalities in Union County made for their contributions to the New Jersey Public Employees Retirement System (PERS) and Police and Firemen’s Retirement System (PFRS) shows that, on average, PERS and PFRS contributions made up 8.17% of total budgets, representing $170 per resident. The average contribution as a percentage of a participant’s salary came to 25.03% with $19,942 as the average contribution per participant.

Green bonds. Issuance is expected to hit a record high this year and so are municipal green bond offerings. My friend and colleague Mark Funkhouser explains why local leaders should take advantage of this alignment of financial interests and moral ones.

More spending flexibility in the American Rescue Plan. Legislation now making its way through Congress would allow governments to use some of their ARP funds for highway and transit projects and to address natural disasters.

Rising income tax revenue. The K-shaped recovery and federal stimulus has resulted in the largest median state personal income jump in 14 years. According to Fitch Ratings, state income tax revenues increased by 6.3% last year and this year is expected to produce similar growth. This has implications for public pensions, tax cuts and — of course — the 2022 midterms.

For nearly two decades, alternative investment managers have been permitted to handle public pension money while they refuse to play by the rules applicable to these funds and submit to public scrutiny.

Wall Street alternative managers have successfully argued that the very same investment information widely distributed to wealthy individuals somehow amounts to “trade secrets” exempt from public records laws… when requested by state workers.

While it’s not surprising Wall Street’s biggest gamblers want to keep investors in the dark as to their misdeeds, it’s unconscionable that STRS Ohio and other public pensions around the nation are willing to abandon transparency, exposing workers to unfathomable risks and jeopardizing their retirement security.

Alternative investment managers may seek to keep secrets, but it’s no secret what’s often in these well-guarded documents: excessive and illegal fees; outrageous conflicts of interest and self dealing; fiduciary breaches and outright violations of law—even criminal conduct. For example, eight years ago the SEC staff found that a majority of private equity firms inflate fees and expenses charged to companies in which they hold stakes.

Private equity firms widely distribute their prospectuses and offering materials to prospective wealthy investors as they trawl globally to raise capital for their costly, high-risk funds. Yet when state and local government pension stakeholders request prospectuses of the funds in which their pensions invest, PE firms claim these very same broadly disseminated documents are “trade secrets” exempt from disclosure under state public records laws. On the one hand, PE risks, fees, and questionable business practices are fully disclosed via prospectus to wealthy investors who can afford to gamble. On the other, government workers in severely underfunded pensions (many of whom have already seen their retirement benefits cut) and taxpayers who are on the hook for any public pension gambling losses, are intentionally kept in the dark. SEC and state securities regulators should demand that every PE investor, including public pension stakeholders, be provided with all material investment information related to these risky investments and end PE secret fleecing of government workers’ pensions.

Our view of the current level of vulnerabilities is as follows:

Asset valuations. Prices of risky assets generally increased since the previous report, and, in some markets, prices are high compared with expected cash flows. House prices have increased rapidly since May, continuing to outstrip increases in rent. Nevertheless, despite rising housing valuations, little evidence exists of deteriorating credit standards or highly leveraged investment activity in the housing market. Asset prices remain vulnerable to significant declines should investor risk sentiment deteriorate, progress on containing the virus disappoint, or the economic recovery stall.

Borrowing by businesses and households. Key measures of vulnerability from business debt, including debt-to-GDP, gross leverage, and interest coverage ratios, have largely returned to pre-pandemic levels. Business balance sheets have benefited from continued earnings growth, low interest rates, and government support. However, the rise of the Delta variant appears to have slowed improvements in the outlook for small businesses. Key measures of household vulnerability have also largely returned to pre-pandemic levels. Household balance sheets have benefited from, among other factors, extensions in borrower relief programs, federal stimulus, and high aggregate personal savings rates. Nonetheless, the expiration of government support programs and uncertainty over the course of the pandemic may still pose significant risks to households.

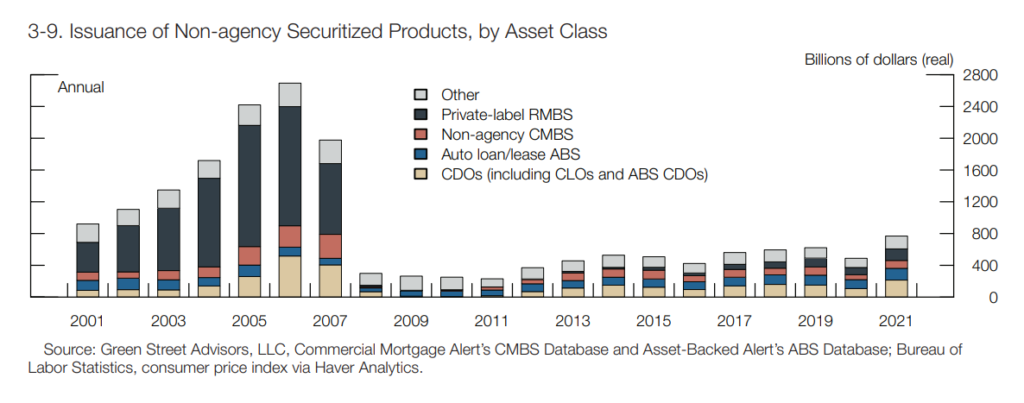

Leverage in the financial sector. Bank profits have been strong this year, and capital ratios remained well in excess of regulatory requirements. Some challenging conditions remain due to compressed net interest margins and loans in the sectors most affected by the COVID-19 pandemic. Leverage at broker-dealers was low. Leverage continued to be high by historical standards at life insurance companies, and hedge fund leverage remained somewhat above its historical average. Issuance of collateralized loan obligations (CLOs) and asset-backed securities (ABS) has been robust.

Funding risk. Domestic banks relied only modestly on short-term wholesale funding and continued to maintain sizable holdings of high-quality liquid assets (HQLA). By contrast, structural vulnerabilities persist in some types of MMFs and other cash-management vehicles as well as in bond and bank loan mutual funds. There are also funding-risk vulnerabilities in the growing stablecoin sector.

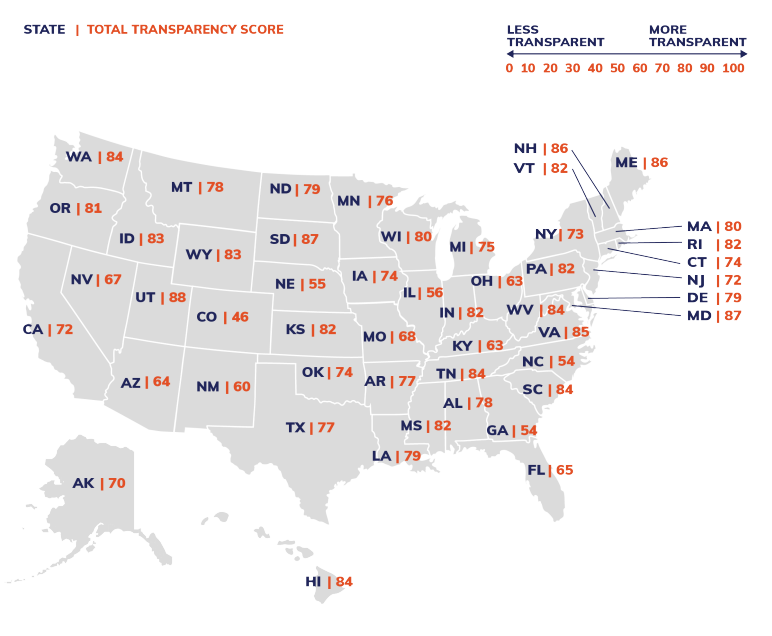

To encourage the publication of transparent and accurate government financial information, Truth in Accounting has created a transparency score for financial reporting by the states. This report focuses on important-but-obscure annual financial reports on file in statehouses across the country and measures their contents against widely accepted best practices from the private sector. This report is based on fiscal year (FY) 2020, which includes the onset of the pandemic and the most recent reports available for all 50 states.

The Financial Transparency Score Report measures the states on an easily understandable 0-100 scoring scale, with a perfect score of 100 signifying an ideal timely, truthful, and transparent performance. While no state earned a perfect score in this year’s analysis, TIA regards a score of 80 or above as noteworthy.

The California State Teachers’ Retirement System (CalSTRS) is now expected to hit full funding in 2041, five years ahead of last year’s prediction of reaching that level in 2046, according to a presentation from CalSTRS Deputy System Actuary David Lamoureux at the fund’s most recent board meeting on Friday. Additionally, board members anticipate that CalSTRS will hit 80% funding in 2024, 10 years ahead of schedule.

The timeline shift is due to the unexpectedly high 27% return CalSTRS earned in the most recent year. The CalSTRS board plans to release the excess funds from this year’s record return over the course of three years. This means that this year, only one-third of the excess funds will be used to alleviate the funded rate. “Because of that, our funding levels will improve, but they will improve slowly over time,” Lamoureux said at the board meeting.

For those wondering when payments under the PBGC Special Financial Assistance program will be coming, the International Foundation of Employee Benefit Plans blog has some guidance.

…..

The Pension Benefit Guaranty Corporation (PBGC) and Treasury officials have delivered a new briefing on the special financial assistance (SFA) program for financially troubled multiemployer plans under the American Rescue Plan Act of 2021 (ARPA). During the briefing on July 22, 2021, PBGC officials walked through the e-filing process, application instructions, assumption changes and what to expect after submitting the application. A recording and slides of the briefing are available here.

….

During the 120-day window, plans must notify PBGC about any facts or data submitted in the application that are no longer accurate. By day 120, PBGC will make a determination to approve or deny the SFA application.

The New York State Common Retirement Fund and the Fire and Police Pension Association of Colorado (FPPA) agreed to a $237.5 million settlement with Boeing’s board after they sued the aerospace company’s board for failing to protect against safety risks related to its 737 Max jets. The money will be paid by the board director’s insurance companies to Boeing itself.

….

The exact reasons why NYS Common chose to hold the stock after suing the company are unknown, as the fund did not respond to a request for comment. However, it’s possible that the pension maintained its shares in order to play a role in restructuring Boeing. It’s taken that approach in the past with companies such as ExxonMobil. In part of the recent settlement between NYS Common and Boeing, the company has agreed to implement new safety measures, including an ombudsman program for employees.

The high vaccination rate stands in contrast to Puerto Rico’s initial vulnerability to the coronavirus. Four years after Hurricane Maria destroyed the electricity grid, power outages still occur regularly. Many municipalities face a shortage of health care facilities and workers.

The U.S. territory responded with some of the strictest pandemic measures in the country, including nonessential-business closures, stay-at-home orders and mask mandates.

……

Its successes aside, Feliú-Mójer noted that COVID-19 has still killed over 3,200 people in Puerto Rico. And she remains concerned about vaccine equity — particularly in rural communities or among older adults who can’t get out of their homes or don’t know how to make an appointment. She says the high overall vaccination rate can hide gaps in coverage.

“You have to look beyond that big number,” she said in a separate interview with NPR. “But then you look at certain municipalities like Loíza, a town in coastal northern Puerto Rico that’s predominantly Black and [a] very poor municipality. Their vaccination rate is about 55%. And so when you look at some of the social determinants that impact communities like Loíza, then they’re not doing as well.”

Author(s): PATRICK JARENWATTANANON, AYEN BIOR, SARAH HANDEL

Last week, real yields, which take into account the corrosive effects of inflation, hit some of their lowest levels on record. One measure of real yields, 10-year Treasury inflation-protected securities, fell to minus 1.2%, according to Tradeweb. That is the lowest on record, according to data going back to February 2003.

In essence, with real yields negative, the purchasing power of money invested will decline over the lifetime of those bonds.

Real yields have fallen because of colliding factors. These include the highest inflation rate in over three decades combined with nominal bond yields that have risen only modestly as central banks hold back from raising rates.

The prospect of negative returns on super safe inflation-protected bonds has pushed investors to buy riskier assets.