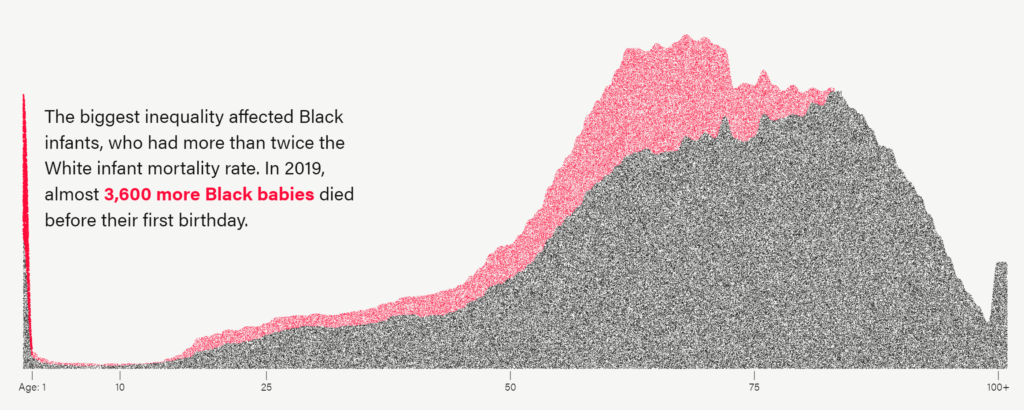

Black Americans die at higher rates than White Americans at nearly every age.

In 2019, the most recent year with available mortality data, there were over 62,000 such earlier deaths — or one out of every five African American deaths.

The age group most affected by the inequality was infants. Black babies were more than twice as likely as White babies to die before their first birthday.

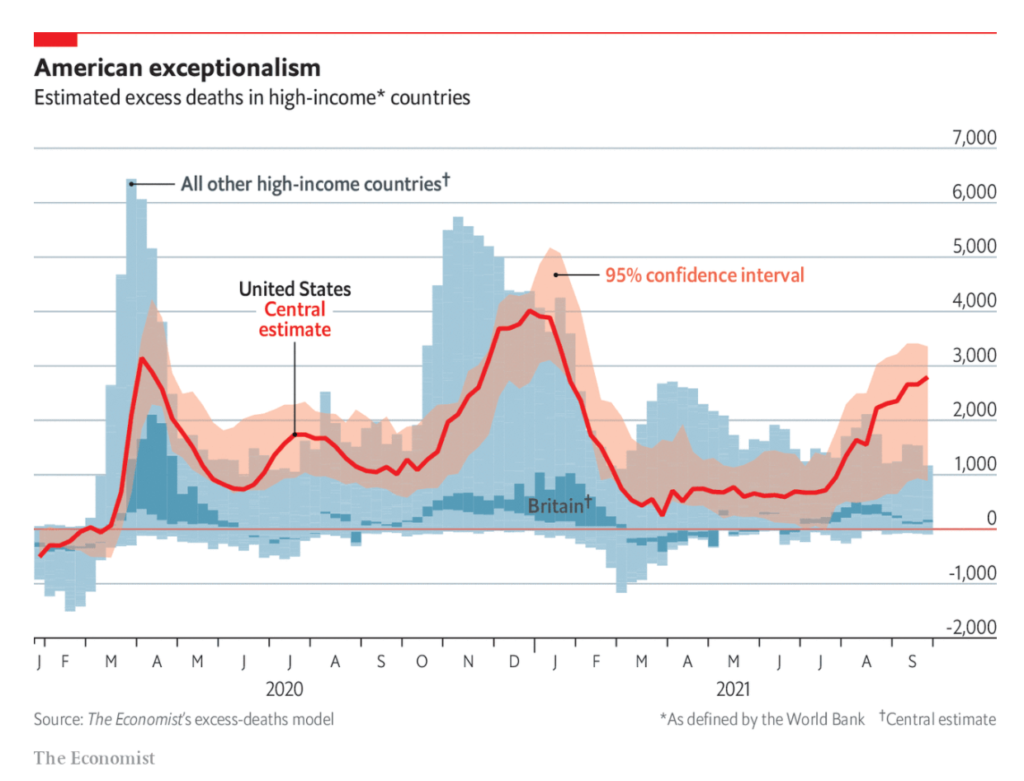

America is recording nearly 2,000 covid-19 deaths a day, according to a seven-day average compiled by Johns Hopkins University. That is only 40% below the country’s January peak. But the true death toll is even worse. The Economist’s excess-deaths model, which estimates the difference between the actual and the expected number of deaths recorded in a given period, suggests that America is suffering 2,800 pandemic deaths per day, with a plausible range of 900 to 3,300, compared with 1,000 (150 to 3,000) in all other high-income countries, as defined by the World Bank. Adjusting for population, the death rate is now about eight times higher in America than in the rest of the rich world.

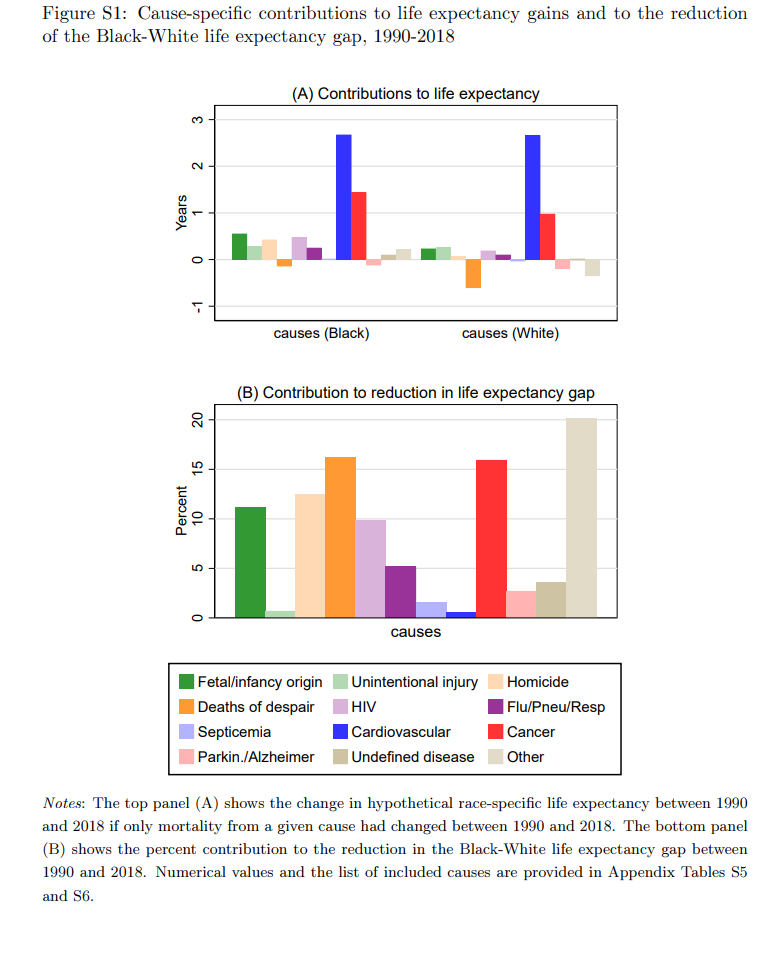

Although there is a large gap between Black and White American life expectancies, the gap fell 48.9% between 1990-2018, mainly due to mortality declines among Black Americans. We examine age-specific mortality trends and racial gaps in life expectancy in rich and poor U.S. areas and with reference to six European countries. Inequalities in life expectancy are starker in the U.S. than in Europe. In 1990 White Americans and Europeans in rich areas had similar overall life expectancy, while life expectancy for White Americans in poor areas was lower. But since then even rich White Americans have lost ground relative to Europeans. Meanwhile, the gap in life expectancy between Black Americans and Europeans decreased by 8.3%. Black life expectancy increased more than White life expectancy in all U.S. areas, but improvements in poorer areas had the greatest impact on the racial life expectancy gap. The causes that contributed the most to Black mortality reductions included: Cancer, homicide, HIV, and causes originating in the fetal or infant period. Life expectancy for both Black and White Americans plateaued or slightly declined after 2012, but this stalling was most evident among Black Americans even prior to the COVID-19 pandemic. If improvements had continued at the 1990-2012 rate, the racial gap in life expectancy would have closed by 2036. European life expectancy also stalled after 2014. Still, the comparison with Europe suggests that mortality rates of both Black and White Americans could fall much further across all ages and in both rich and poor areas.

Author(s): Hannes Schwandt, Janet Currie, Marlies Bär, James Banks, Paola Bertoli, Aline Bütikofer, Sarah Cattan, Beatrice Zong-Ying Chao, Claudia Costa, Libertad Gonzalez, Veronica Grembi, Kristiina Huttunen, René Karadakic, Lucy Kraftman, Sonya Krutikova, Stefano Lombardi, Peter Redler, Carlos Riumallo-Herl, Ana Rodríguez-González, Kjell Salvanes, Paula Santana, Josselin Thuilliez, Eddy van Doorslaer, Tom Van Ourti, Joachim Winter, Bram Wouterse & Amelie Wuppermann

“Between 1990 and 2018,” the paper reports, “the U.S. White-Black life expectancy gap decreased from 7.0 to 3.6 years.” A black person born in the U.S. in 1990 could be expected to live to about age 69, compared to 76 for a white person. In the intervening generation, black life expectancy rose about twice as fast as white life expectancy. A black person born in 2018 could be expected to live just over age 75, compared to just under 79 for a white person.

The drivers, the authors say, are primarily “greater reductions in Black relative to White death rates due to cancer, homicide, HIV, and causes originating in the fetal or infant period.” The most pronounced reductions in black mortality are among children and adults under age 65, rather than the elderly.

“Deaths of despair” (deaths from suicide, drug overdoses, and alcohol-related disease) increased among black and white Americans, especially in the last decade, but took a larger toll on white life expectancy. That accounted for 16.2% of the narrowing of the racial gap. The linear extension of life expectancies for both races stopped after 2012, meaning that it’s hard to see much effect from ObamaCare’s health insurance expansion in the data.

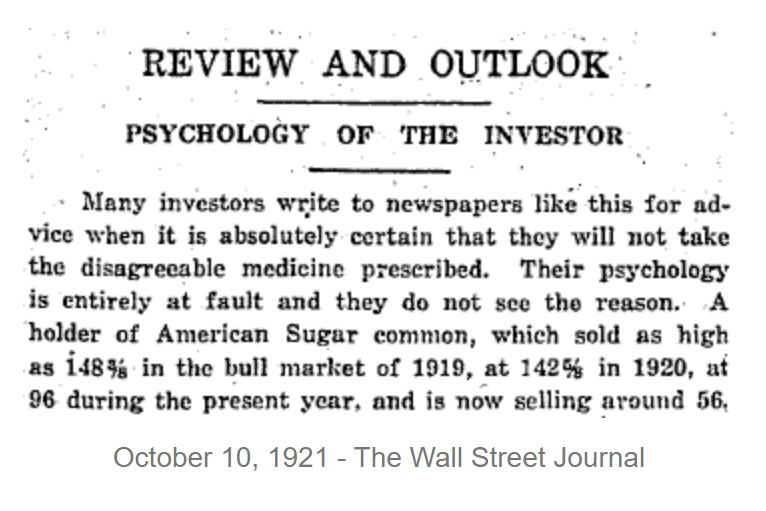

Historical Fact: Replace American Sugar with Apple or Tesla, and this entire column could be published during the next bear market. Human psychology hasn’t changed in 100 years. Central banks cannot prevent a bear market once optimism has been exhausted.

Research has also found being extroverted or introverted affects how people make decisions about Covid-19 precautions. A recent study of more than 8,500 people in Japan published in the journal PLOS One in October 2020 found that those who scored high on a scale of extraversion were 7% less likely to wear masks in public and avoid large gatherings, among other precautions.

Scientists believe that a person’s propensity to take risks is partly genetic and partly the result of early life experiences. Studies of twins have generally found that about 30% of the difference in individual risk tolerance is genetic. Certain negative childhood experiences including physical, emotional or sexual abuse, parental divorce, or living with someone who was depressed or abused drugs or alcohol are linked to risky behavior in adulthood like smoking and drinking heavily, other research has found.

And scientists have discovered that the brains of people who are more willing to take risks look different than those of people who are more cautious. In a study published in the journal Neuron in 2018 that involved scanning the brains of 108 young adults, scientists at the University of Pennsylvania found that participants who made riskier choices on a gambling task had differences in the structure and function of the amygdala, a part of the brain involved in detecting threats, and the prefrontal cortex, a region involved in executive functioning.

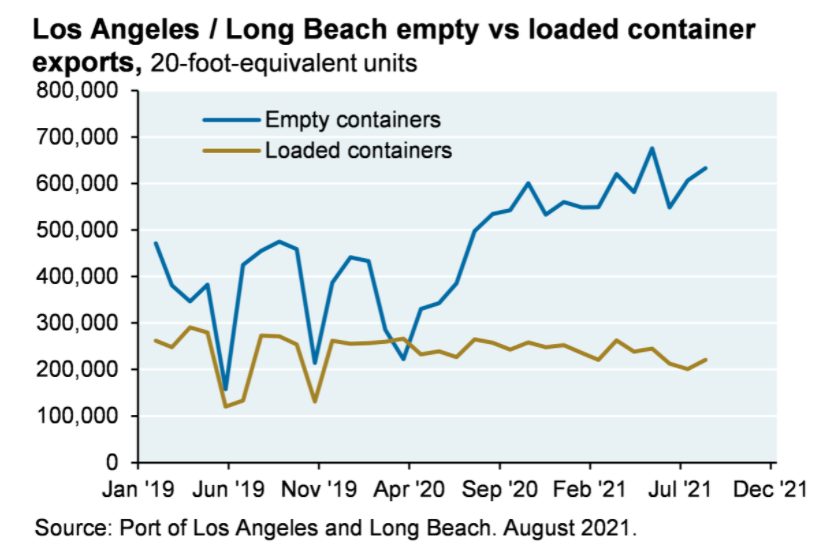

COVID has disrupted supply chains in two major ways: surging demand for imported consumer goods in the West due to pandemic work from home trends and other home improvement spending, and a decline in workers required to maintain and operate these supply chains. The surge in US import demand has led to a sharp rise in eastbound freight rates (see charts for Shanghai->LA and Shanghai->Rotterdam). However, westbound freight rates have not risen nearly as much, leading to an odd and problematic phenomenon: incentives for container owners to move them back to China empty to accelerate receipt of eastbound freight rates, instead of waiting for containers to be refilled to earn westbound freight rates as well. This is illustrated in the fourth chart which shows departing containers from LA/LB: a lot of them started leaving empty once eastbound freight rates surged. This further exacerbates supply chain issues, since US goods (i.e., grains) that were supposed to depart US railcars and warehouses for export remain in place, occupying space that US imported goods were destined for.

Author(s): Michael Cembalest, Chairman of Market and Investment Strategy

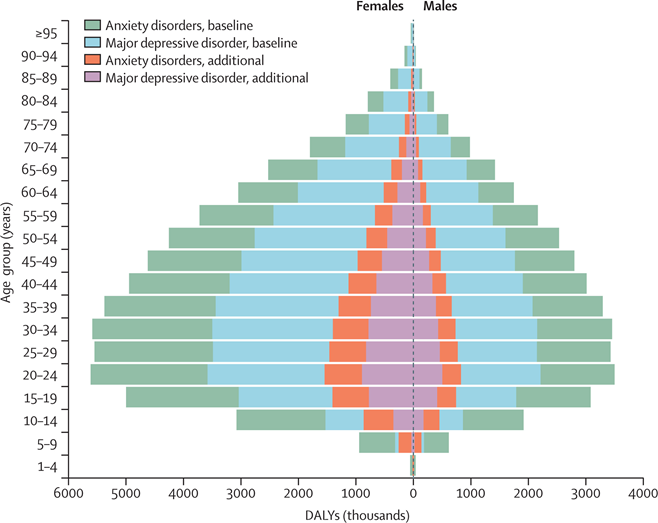

We identified 5683 unique data sources, of which 48 met inclusion criteria (46 studies met criteria for major depressive disorder and 27 for anxiety disorders). Two COVID-19 impact indicators, specifically daily SARS-CoV-2 infection rates and reductions in human mobility, were associated with increased prevalence of major depressive disorder (regression coefficient [B] 0·9 [95% uncertainty interval 0·1 to 1·8; p=0·029] for human mobility, 18·1 [7·9 to 28·3; p=0·0005] for daily SARS-CoV-2 infection) and anxiety disorders (0·9 [0·1 to 1·7; p=0·022] and 13·8 [10·7 to 17·0; p<0·0001]. Females were affected more by the pandemic than males (B 0·1 [0·1 to 0·2; p=0·0001] for major depressive disorder, 0·1 [0·1 to 0·2; p=0·0001] for anxiety disorders) and younger age groups were more affected than older age groups (−0·007 [–0·009 to −0·006; p=0·0001] for major depressive disorder, −0·003 [–0·005 to −0·002; p=0·0001] for anxiety disorders). We estimated that the locations hit hardest by the pandemic in 2020, as measured with decreased human mobility and daily SARS-CoV-2 infection rate, had the greatest increases in prevalence of major depressive disorder and anxiety disorders. We estimated an additional 53·2 million (44·8 to 62·9) cases of major depressive disorder globally (an increase of 27·6% [25·1 to 30·3]) due to the COVID-19 pandemic, such that the total prevalence was 3152·9 cases (2722·5 to 3654·5) per 100 000 population. We also estimated an additional 76·2 million (64·3 to 90·6) cases of anxiety disorders globally (an increase of 25·6% [23·2 to 28·0]), such that the total prevalence was 4802·4 cases (4108·2 to 5588·6) per 100 000 population. Altogether, major depressive disorder caused 49·4 million (33·6 to 68·7) DALYs and anxiety disorders caused 44·5 million (30·2 to 62·5) DALYs globally in 2020.

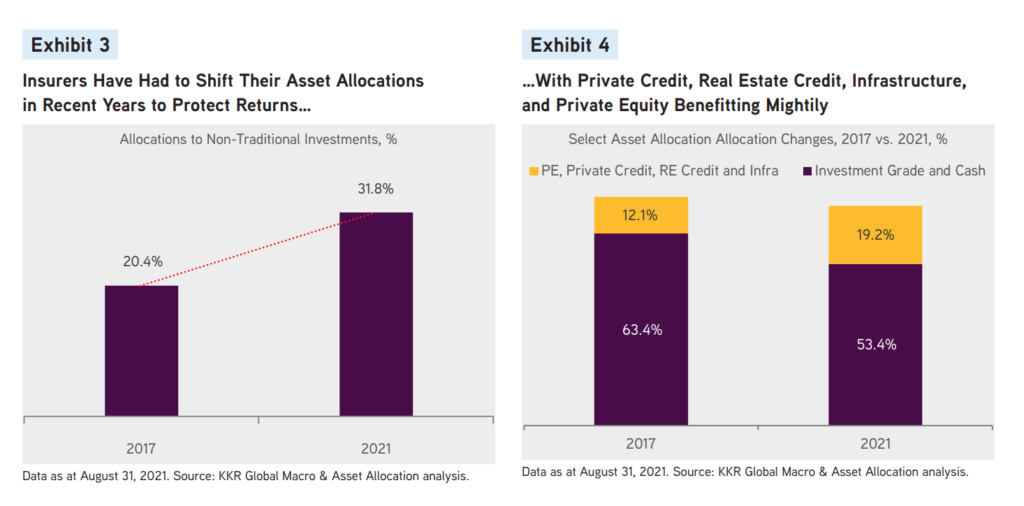

To compensate for the ongoing pressure on interest rates, CIOs participating in our survey have made substantive, structural shifts in their asset allocations. Why did they make this transition? We believe that CIOs are embracing complexity and the thoughtful use of illiquidity, as public market assets roll off and excess cash builds up. Improved asset-liability matching and more robust risk management have also helped, we believe. Reflective of these shifts, non-traditional investments, including Real Estate Credit and Structured Credit, collectively experienced almost a 1,200 basis point increase in market share. As a result, total

non-traditional investments now account for 31.8% of total portfolios surveyed, compared to 20.3% in 2017. As we detail below and in Exhibit 21, our work shows that 100% of the gain came at the expense of traditional public credit, which fell to 48.5% of portfolios surveyed, compared to 60.7% in 2017. Meanwhile, the allocation to Liquid Equities (predominantly by Property & Casualty and Reinsurers that typically favor Public Equities for liquidity) slipped to 5.5% from 9.1% over the same period. Cash as a percentage of assets is now at 4.9%, which is almost double the level it was the last time we did the survey. See below for full details on this increase but we think high cash balances are fueling thoughtful moves into longer duration assets. However, there is obviously more work to be done, as the supply of yielding, long-term assets remains limited.

Allstate Corp. plans to sell its headquarters building, marking the U.S. finance industry’s firmest endorsement yet of the desire to offer hybrid work after the pandemic.

With many employees choosing to work remotely, the insurance giant will sell its offices in Northbrook, Illinois, according to an emailed statement Friday. The complex in a Chicago suburb has several buildings that total 1.9 million square feet on a 186-acre (75 hectares), Allstate has said in regulatory filings.

Methods: We quantified COVID-19-associated caregiver loss and orphanhood in the US and for each state using fertility and excess and COVID-19 mortality data. We assessed burden and rates of COVID-19-associated orphanhood and deaths of custodial and co-residing grandparents, overall and by race/ethnicity. We further examined variations in COVID-19-associated orphanhood by race/ethnicity for each state.

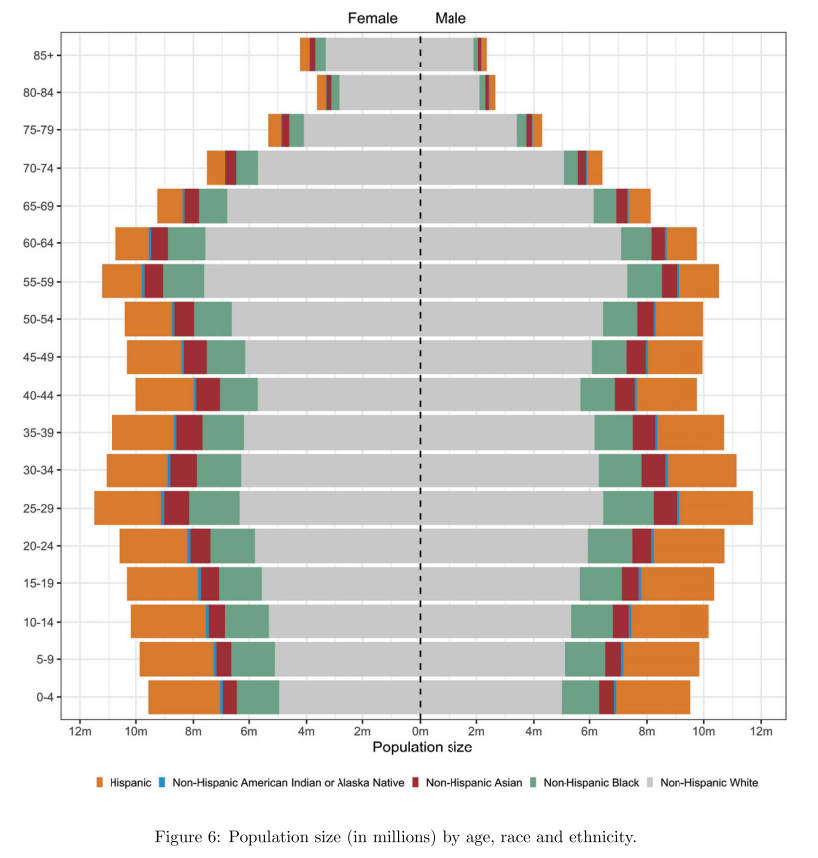

Results: We found that from April 1, 2020 through June 30, 2021, over 140,000 children in the US experienced the death of a parent or grandparent caregiver. The risk of such loss was 1.1 to 4.5 times higher among children of racial and ethnic minorities, compared to Non-Hispanic White children. The highest burden of COVID-19-associated death of parents and caregivers occurred in Southern border states for Hispanic children, Southeastern states for Black children, and in states with tribal areas for American Indian/Alaska Native populations.

Author(s): Hillis SD, Blenkinsop A, Villaveces A, et al.

Publication Date: 2021, accessed 12 Oct 2021

DOI: 10.1542/peds.2021-053760

Citation: Hillis SD, Blenkinsop A, Villaveces A, et al. COVID-19-associated orphanhood and caregiver death in the United States. Pediatrics. 2021; doi: 10.1542/peds.2021-053760

Nevertheless, the motivations for outsourcing IMHO are not properly understood. In the auto business, which is typical of a lot of US industry, direct factory labor cost is 11% to 13% of product cost. The offsets against that are greater supervisory and coordination costs (longer shipping times and financing costs, and with that, greater risk of being stuck with inventories related to products that aren’t selling well) and just plain old screw ups due to having more moving parts.

In other words, outsourcing is better understood as a transfer from factory labor to managers and executives, at the cost of greater operational risk.