Asset Value (Market) @ 5/1/19: $523,604 Value of liabilities using RPA rate (3.09%) @ 5/1/19: $5,108,203 including: Retirees: $4,213,315 Separated but entitled to benefits: $820,490 Still working: $74,398

Private equity investments lack transparency and are difficult to value. As opposed to publicly traded securities, limited partnerships used by private equity managers can’t provide frequent performance updates and, as a result, advise stakeholders after the end of each fiscal year. This leads to a lag in reporting important details. Moreover, shares of companies owned by private equity funds are not publicly traded, meaning that their values can only be estimated, which is subject to potential bias. Private equity firms are also not obligated by the law to publish their lists of assets in accordance with Securities and Exchange Commission rules. While this information can be found on Bloomberg Professional Terminal, it is not available to the general public. This lack of transparency should be concerning to employees and retirees who rely on these funds and taxpayers who contribute to them.

For the Pennsylvania teacher system, the management fees associated with private equity investments that the plan had to pay over the past four years ($4.3 billion) are more than the total amount members paid into the plan during the same time ($4.2 billion). The pension plan recently announced that member contributions will have to be raised going forward because of long-term investment results below the plan’s benchmark. As a point of comparison, the New York State Teachers’ Retirement System, which has double the assets of PSERS, reported 36% less in total investment fees and expenses than PSERS.

Let’s investigate the claim that the gender pay gap is a result of discrimination by looking at some of the data on wages and hours worked by gender and by marital status and age in the BLS report for 2020:

….

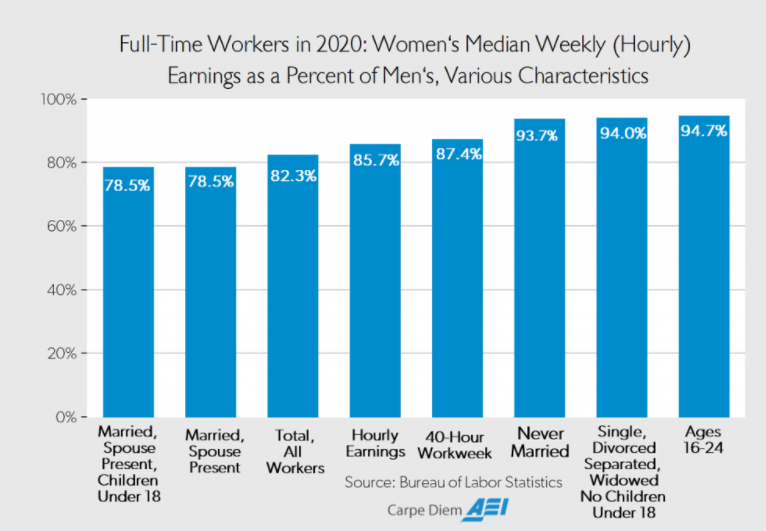

Comment: Because men work more hours on average than women, some of the raw earnings gap naturally disappears just by simply controlling for the number of hours worked per week, an important factor not even mentioned by groups like the National Committee on Pay Equity. For example, women earned 82.3% of median male earnings for all workers working 35 hours per week or more in 2020, for a raw, unadjusted pay gap of 17.7% for all full-time workers. But for those workers with a 40-hour workweek (more than three-quarters of all full-time female workers), women earned 87.4% of median male earnings, for a smaller pay gap of only 12.6% (see chart and Table 1). Therefore, once we control only for one variable – hours worked – and compare men and women both working 40-hours per week in 2020, almost one-third (5.1 percentage points) of the raw 17.7% pay gap reported by the BLS for full-time workers disappears.

….

Bottom Line: When the BLS reports that women working full-time in 2020 earned 82.3% of what men earned working full-time, that is very much different from saying that women earned 82.3% of what men earned for doing exactly the same work while working the exact same number of hours in the same occupation, with exactly the same educational background and exactly the same years of continuous, uninterrupted work experience, and with exactly the same marital and family (e.g., number of children) status. As shown above, once we start controlling individually for the many relevant factors that affect earnings, e.g., hours worked, age, marital status, and having children, most of the raw earnings differential disappears. In a more comprehensive study that controlled for all of the relevant variables simultaneously, we would likely find that those variables would account for nearly 100% of the unadjusted, raw earnings differential of 17.7% for women’s earnings compared to men as reported by the BLS. Discrimination, to the extent that it does exist, would likely account for a very small portion of the raw 17.7% gender earnings gap.

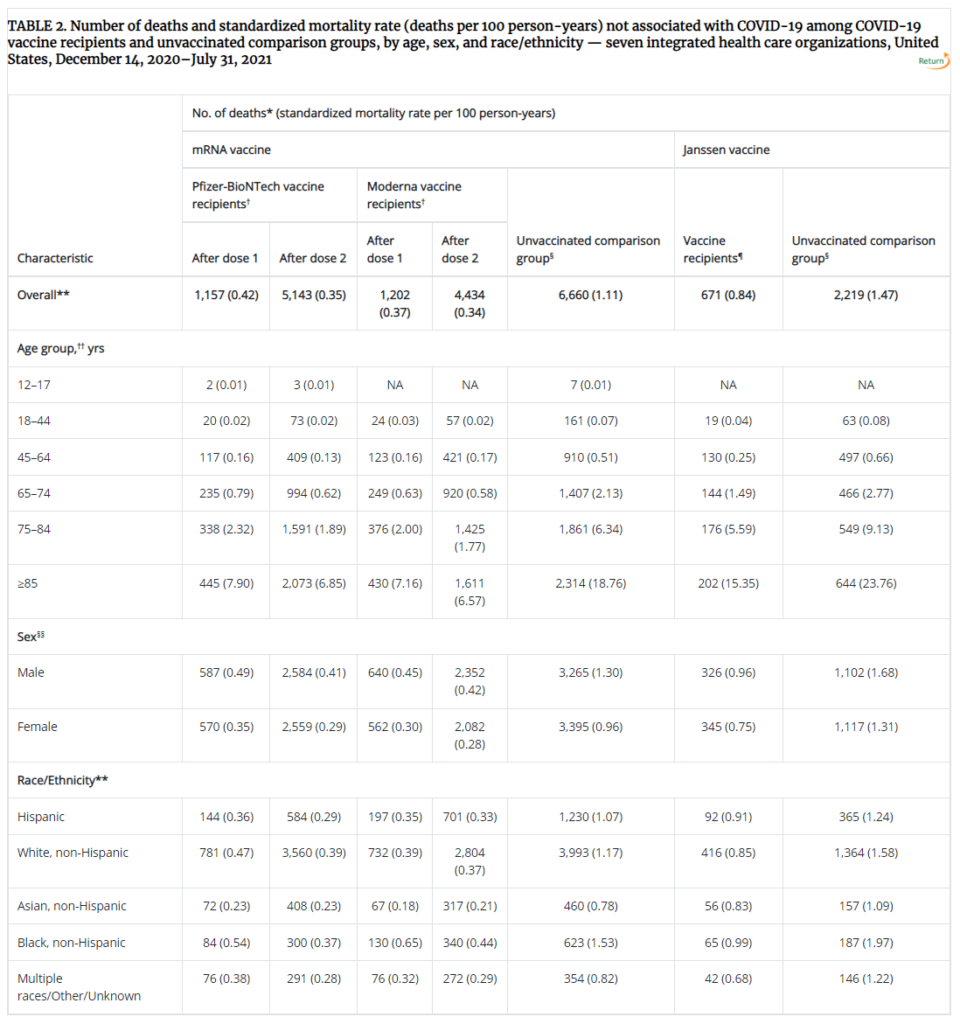

Although deaths after COVID-19 vaccination have been reported to the Vaccine Adverse Events Reporting System, few studies have been conducted to evaluate mortality not associated with COVID-19 among vaccinated and unvaccinated groups.

What is added by this report?

During December 2020–July 2021, COVID-19 vaccine recipients had lower rates of non–COVID-19 mortality than did unvaccinated persons after adjusting for age, sex, race and ethnicity, and study site.

What are the implications for public health practice?

There is no increased risk for mortality among COVID-19 vaccine recipients. This finding reinforces the safety profile of currently approved COVID-19 vaccines in the United States. All persons aged ≥12 years should receive a COVID-19 vaccine.

Author(s): Stanley Xu, PhD1; Runxin Huang, MS1; Lina S. Sy, MPH1; Sungching C. Glenn, MS1; Denison S. Ryan, MPH1; Kerresa Morrissette, MPH1; David K. Shay, MD2; Gabriela Vazquez-Benitez, PhD3; Jason M. Glanz, PhD4; Nicola P. Klein, MD, PhD5; David McClure, PhD6; Elizabeth G. Liles, MD7; Eric S. Weintraub, MPH8; Hung-Fu Tseng, MPH, PhD1; Lei Qian, PhD1

The lawsuit notes the difficult position the retirement system was in, saying that “there was no prudent investment strategy that would allow KRS to invest its way to significantly improved funded status,” and that “the trustees were trapped in a demographic/financial vise.” However, while acknowledging there was no prudent investment strategy for KRS to get out of the hole it was in, the plaintiffs are simultaneously critical of Carlson and the other defendants for taking what they consider to be “longshot imprudent risks.”

The lawsuit also criticizes the hedge funds of funds for not providing high enough returns for the entire KRS portfolio to meet or exceed its 7.75% assumed rate of return. However, the same could be said for fixed income and many other assets in the KRS portfolio. Broad hedge fund portfolios are generally created to reduce risk, not beat equity markets.

“The Black Boxes did not provide the investment returns trustees needed for KRS to return to or exceed on the average its AARIR [assumed annual rate of investment return] of 7.75%,” says the lawsuit, which is targeting approximately 3% of KRS’ overall investments, while saying they should carry the entire portfolio to meet or outperform a rate of return the state acknowledged as “unrealistic and unachievable.”

The lawsuit also claims the investments “lost millions of dollars in 2015 to 2016,” which was more than two years after Carlson left, and which was a particularly bad time period for the entire hedge fund industry. The lawsuit criticized one of the investments, known as the Henry Clay Fund, for providing “exceptionally large fees for Blackstone”; however, the suit also states that “the amount of the fees could not be calculated and were not disclosed.”

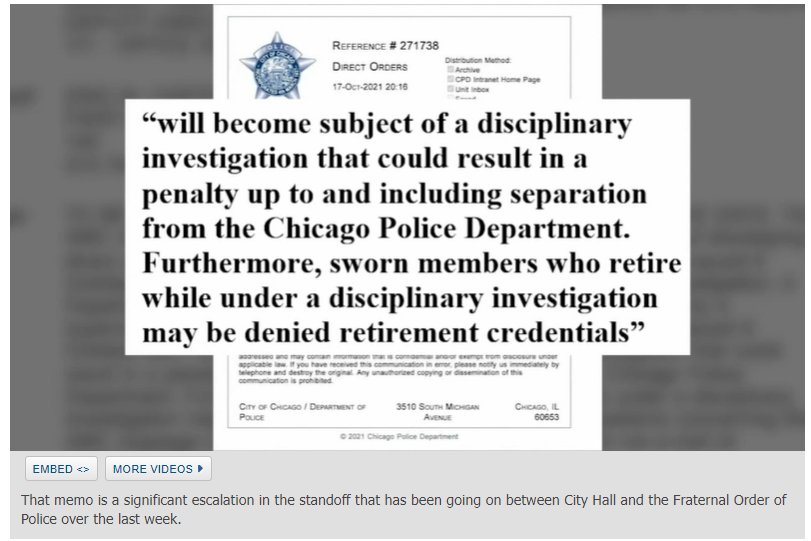

A second memo, obtained by the I-Team, was distributed throughout CPD Sunday. The latest memo threatens the firing of officers who do not follow the city’s vaccine policy and orders it be communicated to officers at all police roll calls.

“TO BE READ AT ALL ROLL CALLS FOR SEVEN (7) CONSECUTIVE DAYS. This AMC message informs Department members of consequences of disobeying a direct order to comply with the City of Chicago’s Vaccination POlice issued 8 October 2021 and being the subject of the resulting disciplinary investigation. A Department member, civilian or sworn, who disobeys a direct order by a supervisor to comply with the City of Chicago’s Vaccination Police issued 8 October 2021 will become the subject of a disciplinary investigation that could result in a penalty up to and including separation from the Chicago Police Department. Furthermore, sworn members who retire while under disciplinary investigations may be denied retirement credentials. Any questions concerning this AMC message may be directed to the Legal Affairs Division via e-mail,” the memo said.

…..

“Roughly 38% of the sworn officers on this job, almost 40% can lock in a pension and walk away today,” Fraternal Order of Police President John Catanzara, Jr. said.

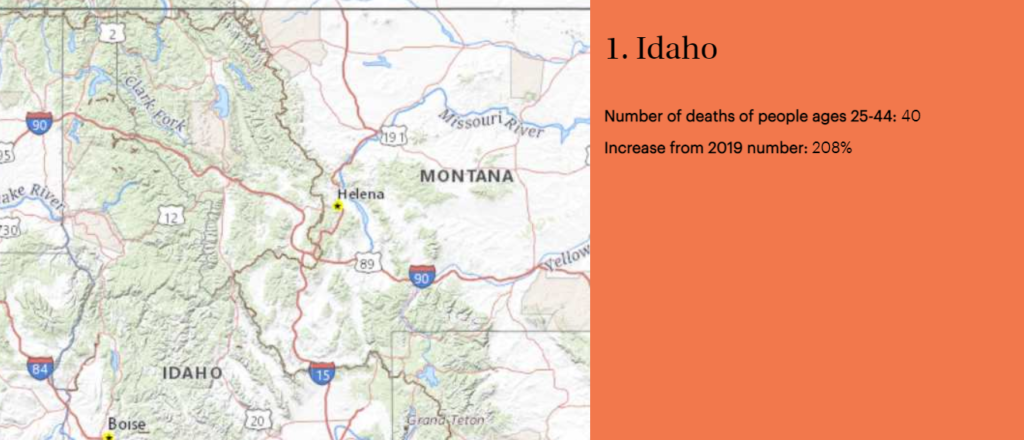

In the first two weeks ending in September, the number of deaths of U.S. residents in the 25-44 age group spiked to 8,604.

The number of deaths of people in that age group was 22% higher than it was during the comparable period, and 57% higher than it was during the comparable period in 2019 — before the COVID-19 pandemic began.

In the first half of 2021, which included the January spike, the number of deaths of people in the 25-44 age group was 38% higher than in the first half of 2019.

There are about 87.4 million people in the 25-44 age group in the United States, according to the Census Bureau.

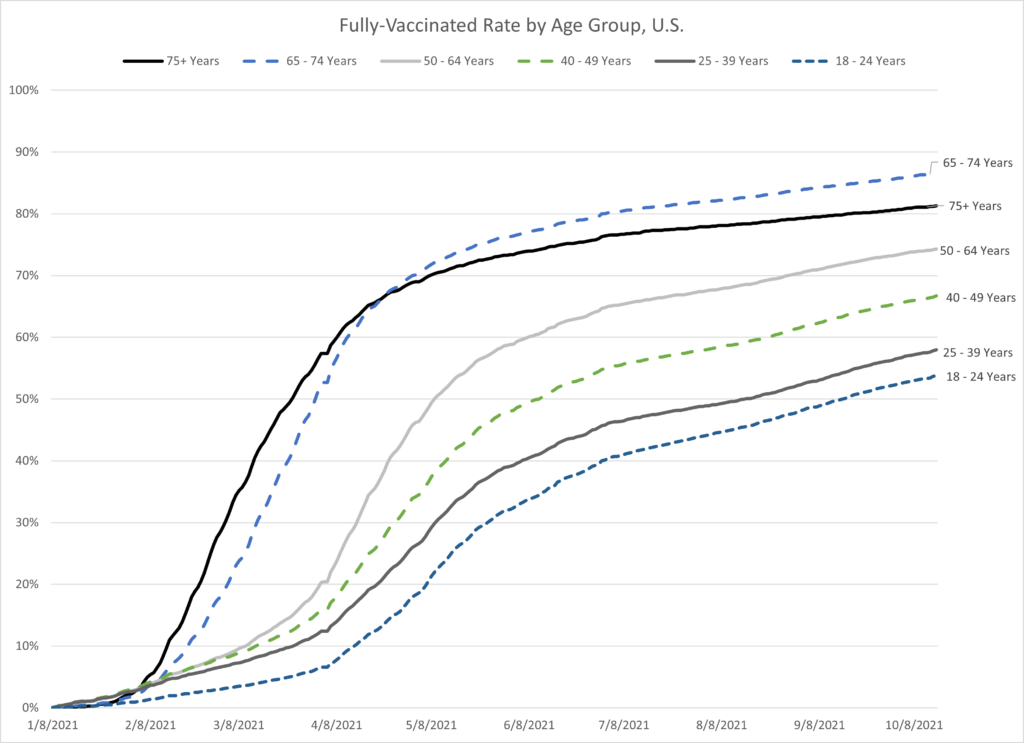

Trends in vaccinations and cases by age group, at the US national level. Data is stratified by at least one dose and fully vaccinated. Data also represents all vaccine partners including jurisdictional partner clinics, retail pharmacies, long-term care facilities, dialysis centers, Federal Emergency Management Agency and Health Resources and Services Administration partner sites, and federal entity facilities.

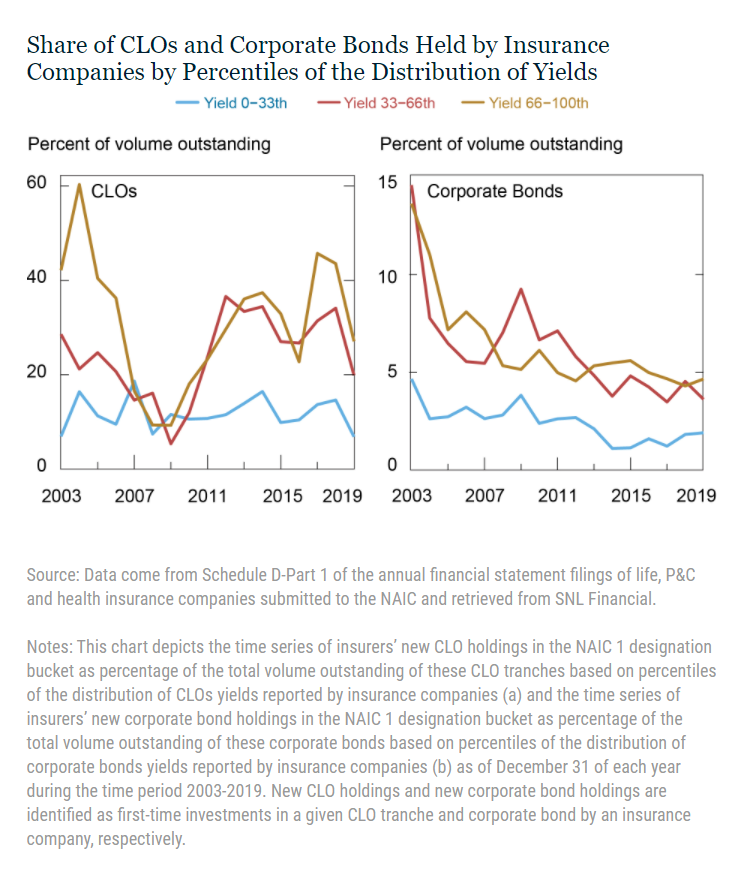

The rating-based mapping was partially altered in 2010, when the NAIC enacted a regulatory change that essentially allowed insurance companies to report CLO tranches that were purchased at a discount, or highly impaired, in a lower NAIC category than that implied by the rating-based mapping. The new capital regime for CLO investments likely increased insurance companies’ incentives to invest in higher-yielding CLO tranches.

The following chart presents some evidence consistent with reach-for-yield behavior, particularly since the regulatory reforms of 2010. The left panel shows the time series of insurers’ new CLO holdings falling into the NAIC 1 designation as a percentage of the total volume outstanding of these tranches based on percentiles of the distribution of CLOs yields for each year. As expected, there is a clear preference for the riskiest tranches within NAIC 1 (those with yields above the 66th percentile) throughout the sample period, with the exception of the financial crisis, when all yields are squeezed at their minimum levels. Interestingly, the market shares of CLO tranches with yields above the 33rd percentile experience a sharp increase in the two years following the 2010 regulatory reform, then register a significant drop in 2019, when the reform was repealed. We do not find similar evidence in insurance companies’ corporate bond investments (right panel).

Author(s): Fulvia Fringuellotti, João A. C. Santos

Publication Date: 13 Oct 2021

Publication Site: Federal Reserve Bank of New York

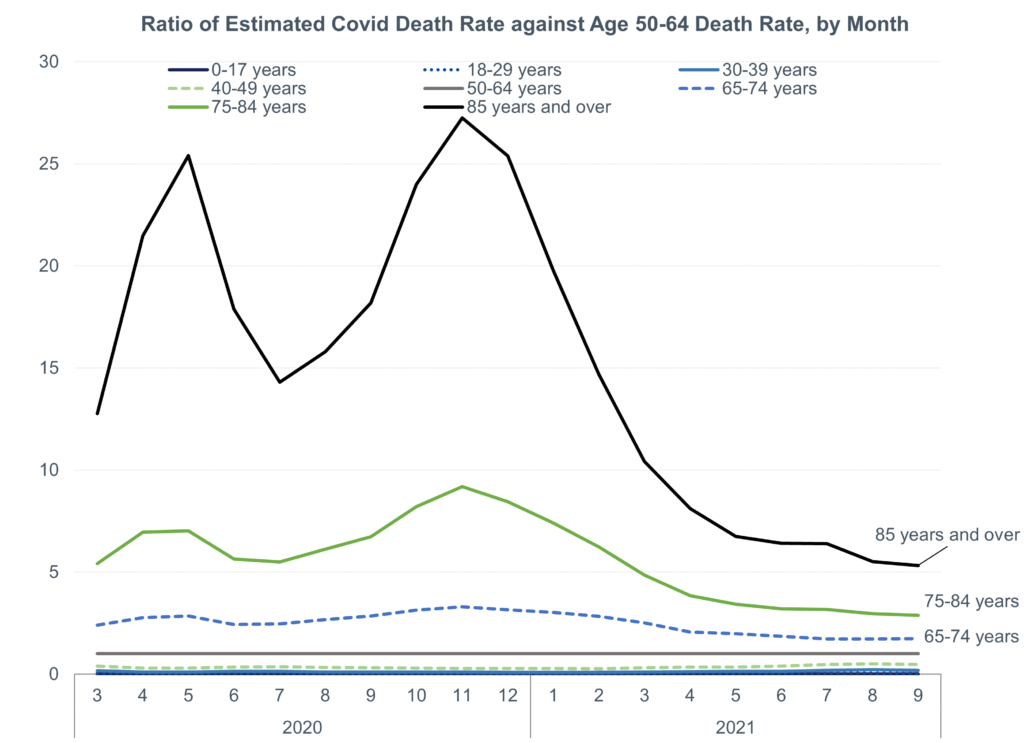

I will put a few facts in front of you, and you think it through: – The population age 85+ in the U.S. in 2020 was 6.3 million – Through July 2021, there were a little over 180K COVID deaths for that group – That’s about 3% of the age 85+ population

Do you think only 3% of the age 85+ population is vulnerable to COVID?

Pretty much all of them are “vulnerable”. The mortality rate for people age 85 (much less older) was 7.3% for females and 9.5% for males in the most recently available tables. It only goes up from there.

There is a huge difference in mortality by age for just non-pandemic years, and it’s also true for COVID.

There may be a few hardy souls with a base risk similar to the middle-aged without vaccines, but the percentage is not high.

The vaccines have been having an effect in cutting risk.

The inaugural coffee chat of my YouTube channel features two research scholars from scientific community who shared their perspectives on how data plays a crucial role in research area.

By watching this video you will gather information on the following topics:

a) the importance of data in scientific research,

b) valuable insights about the data handling practices in research areas related to molecular biology, genetics, organic chemistry, radiology and biomedical imaging,

c) future of AI and machine learning in scientific research.

Author(s):

Efrosini Tsouko, PhD from Baylor College of Medicine; Mausam Kalita, PhD from Stanford University; Soumava Dey

Publication Date: 26 Sept 2021

Publication Site: Data Science with Sam at YouTube