Link: https://www.clubvita.us/news-and-insights/mega-trend-10-the-democratization-of-longevity

Graphic:

Excerpt:

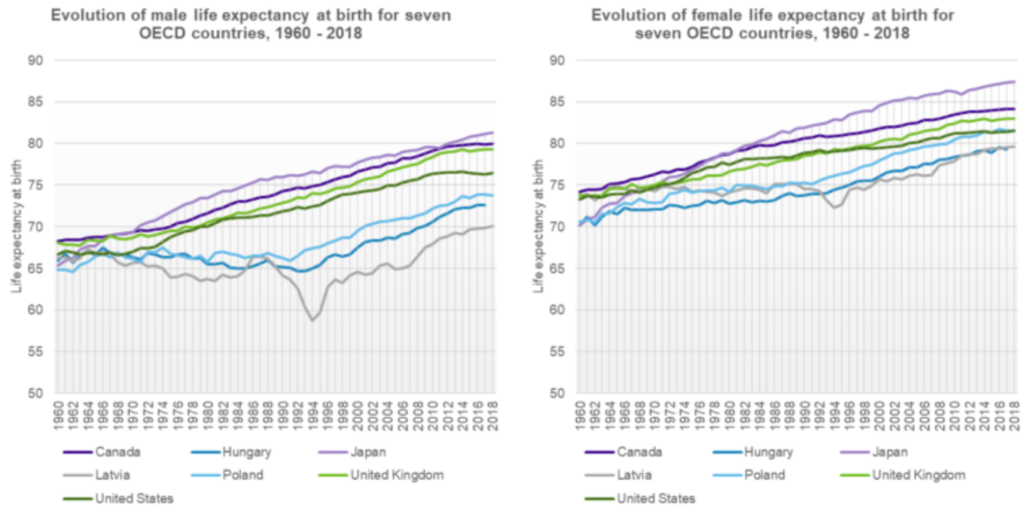

Illustrated below is the evolution of life expectancy at birth for seven Organization for Economic Co-operation and Development (OECD) countries: Canada, Hungary, Japan, Latvia, Poland, the United Kingdom, and the United States. Across the seven countries, male life expectancy at birth ranged from 64.8 years to 68.2 years in 1960, and 69.8 years to 81.1 years in 2017, demonstrating an increase in the inequality of life expectancy of almost eight years between these countries over the period. For females, the increase was approximately four years. The inequality in life expectancy is more apparent and unsettling if we consider, for example, developing countries in Africa, averaging a life expectancy of around 63 years in 2019.

….

Altogether, I believe greater democratization of longevity is achievable with the adoption of health technologies, while ensuring they are accessible and affordable. I am hopeful but I see several challenges ahead. Such a reality will be reliant on governments, health care professionals, and patients’ acceptance and reliance on what the future of health holds. It will also require global partnerships to build out ecosystems that will facilitate inclusive innovation.

Author(s): Shantel Aris

Publication Date: 22 Sept 2021

Publication Site: Club Vita