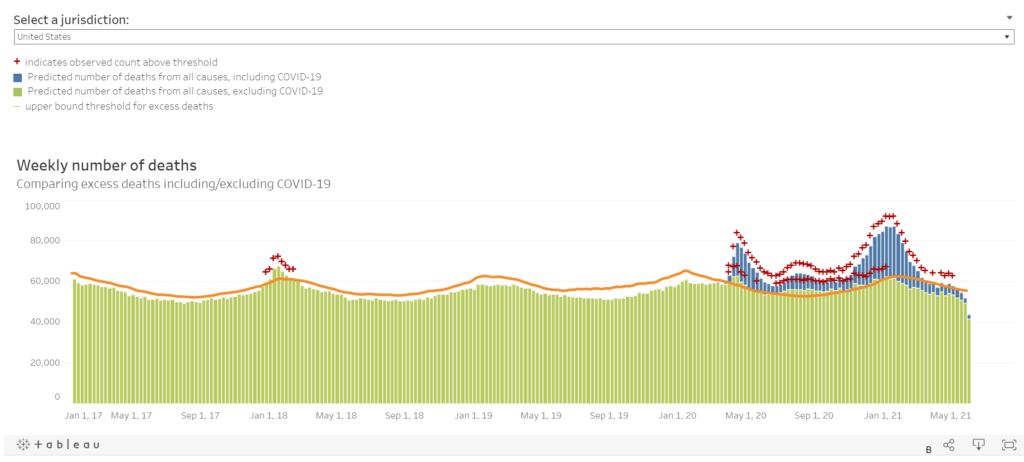

I want you to notice something — the blue bars are the “with COVID” portion of deaths, and the chartreuse bars are the ones “without COVID”. The bars are weekly counts of deaths when they occurred. Ignore the most recent weeks because they don’t have full data reported yet.

The red pluses indicate excess mortality, defined as exceeding the 95th percentile for expected mortality for that week (so it includes seaonality). You can see the excess mortality from the 2017-2018 flu season, which was bad for a flu season.

The non-COVID mortality has been in excessive mortality range for almost all 2020 after March. But since the beginning of 2021, it has dropped off…. and COVID mortality has also dropped off.

I think we may be almost in “normal” range soon. We shall see!

The Labor Department’s consumer price index surged 5% year-over-year in May, the largest increase since August 2008 when oil was $140 a barrel. But don’t worry, Americans. The Federal Reserve says inflation is “transitory” and that it has the tools to control prices if they start to spiral out of control. Let us pray.

Nobody should be surprised that prices are increasing everywhere from the grocery store to the car dealership. Demand is soaring as the pandemic recedes while supply constraints linger, especially in labor and transportation. As always, this is a price shock largely made by government. Congress has shovelled out trillions of dollars in transfer payments over the past year, and the Fed has rates at zero while the economy may be growing at a 10% annual rate.

The personal savings rate in April was 14.9%, double what it was before the pandemic. Record low mortgage interest rates have enabled homeowners to lower their monthly payments to burn more cash on other things. Congress’s $300 unemployment bonus and other welfare payments for not working have contributed to an enormous worker shortage, which is magnifying supply shortages.

All of this is showing up in higher prices. Over the last 12 months, core inflation excluding food and energy is up 3.8% and much more for used cars (29.7%), airline fares (24.1%), jewelry (14.7%), bikes (10.1%) and footwear (7.1%). Commodity prices from oil to copper to lumber have surged. Higher lumber prices are adding $36,000 to the price of a new home.

The Fed has embarked on a massive expansionary quest in recent years. In 2020, total Reserve Bank assets rose from $4.2 trillion to $7.4 trillion amidst the pandemic and related government lockdown and fiscal “stimulus” policies. That was roughly three times the extraordinary growth in the consolidated balance sheet for the Reserve Banks in the 2008-2009 financial crisis. And in the latest weekly “H.4.1” release, total assets were up to $7.8 trillion – rising about a hundred billions dollars a month so far this year.

….

Today, short and long-term interest rates on government bonds rest near historic lows, important in part because the Fed massively expanded its purchases of government bonds. But low interest rates can’t be taken for granted, particularly if we get significantly higher inflationary expectations — which appear to have begun to sprout in recent weeks.

If we get significantly higher interest rates for that reason, the Reserve Bank balance sheet impact from losses on securities assets would arrive if the losses become “realized” – a realistic prospect if the Federal Reserve reverses course and starts selling off securities as a means of conducting monetary policy amidst higher inflationary expectations.

According to The Senior Citizens League, the sleight of hand behind it is a formula for calculating the Cost of Living Adjustment (COLA) that has robbed seniors of 33% of their buying power since 2010.

Since then, annual COLA increases have averaged a meager 1.375%. That means the average recipient has received a COLA increase of less than $20 a month. For many, the con job is even more vexing because much of that gain is taken back with increases in Medicare premiums.

These annual COLA adjustments are based by the U.S. Bureau of Labor Statistics (BLS) on a formula that uses the Consumer Price Index for All Urban Wage Earners and Clerical Workers — a lengthy descriptor that’s usually abbreviated as CPI-W. Therein lies the problem — this index does not accurately reflect the rising costs that most affect seniors — such as medical care and drugs, food/staples and rent. Even the most modest estimates suggest these costs are increasing at a rate of somewhere between 5% and 10% annually.

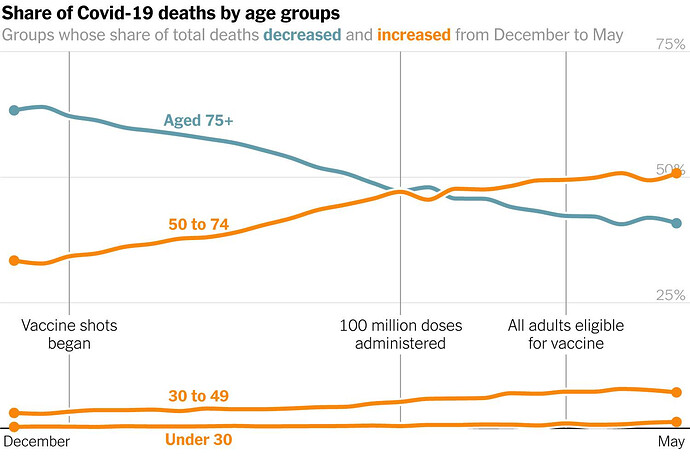

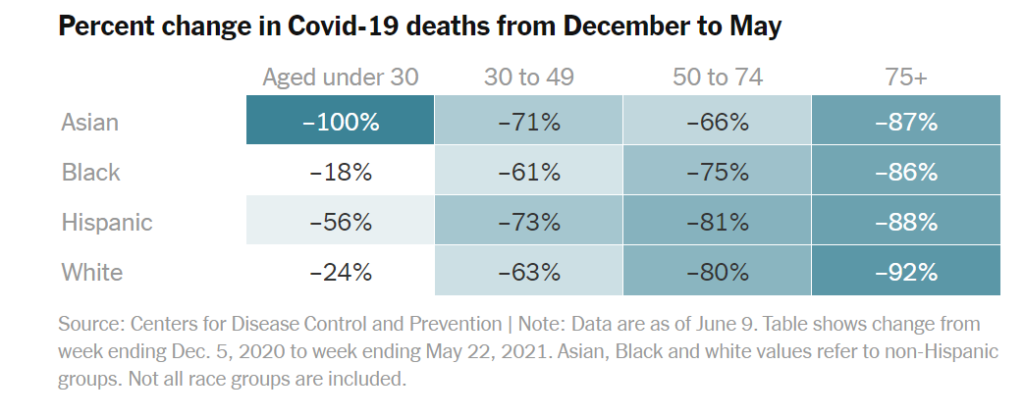

Looking at the NYT article “Which Groups Are Still Dying of Covid in the U.S.?” — online interactive data visualization related to COVID deaths and demographic groups in the U.S. I thought one key graph was misleading

Welcome to another episode of Positivity with Paul, where I find Fellow Actuaries – pun intended – for a conversational Q&A on their life. The focus is on their journey along the actuarial exam path and beyond, some of the challenges they faced, and how those challenges helped shape them to become who they are today.

To give some brief context on becoming an Actuary, there’s a number of actuarial exams that one has to go through. These exams are very rigorous and typically, only the top 40% pass at each sitting, They cover complex mathematical topics like statistics and financial modelling but also insurance, investments, regulatory and accounting. Candidates can study up to 5 months per sitting and they will take 7 to 10 years on average to earn their Fellowship degree. To that end, I launched this series of podcasts because I was curious about what drove my guests to surmount trials and tribulations to get to the end goal of becoming an Actuary.

My guest in this interview is Mary Pat Campbell. Mary Pat is an actuary working in Connecticut, investigating life insurance and annuity industry trends. She has been interested in exploring mortality trends, public finance and public pensions as an avocation. Some of these explorations can be found at her blog: stump.marypat.org. Mary Pat is a fellow of the Society of Actuaries and a member of the American Academy of Actuaries. She has been working in the life/annuity industry since 2003. She holds a master’s degree in math from New York University and undergraduate degrees in math and physics from North Carolina State University. In this podcast, Mary Pat discusses similarities in concepts between physics and actuarial science, the current low interest rate environment and lessons learnt in the insurance sector from the financial crisis in 2008-2009. Hope you enjoy this all-inclusive interview! Paul Kandola

“Previously, at the start of the pandemic, we were seeing people who were over the age of 60, who have numerous comorbidities,” said Dr. Krutika Kuppalli, an infectious disease expert at the Medical University of South Carolina. “I’m not seeing that as much anymore.” Instead, she said, hospitalizations have lately been skewing toward “people who are younger, people who have not been vaccinated.”

More than 80 percent of those 65 and older have received at least one dose of a Covid-19 vaccine, compared with about half of those aged 25 to 64 who have received one dose. Data collected by the C.D.C. on so-called breakthrough infections — those that happen to vaccinated people — suggest an exceedingly low rate of death among people who had received a Covid-19 vaccine.

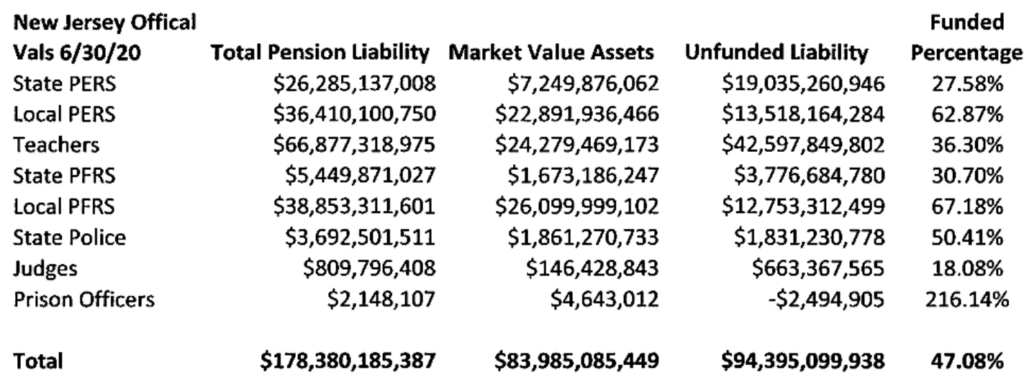

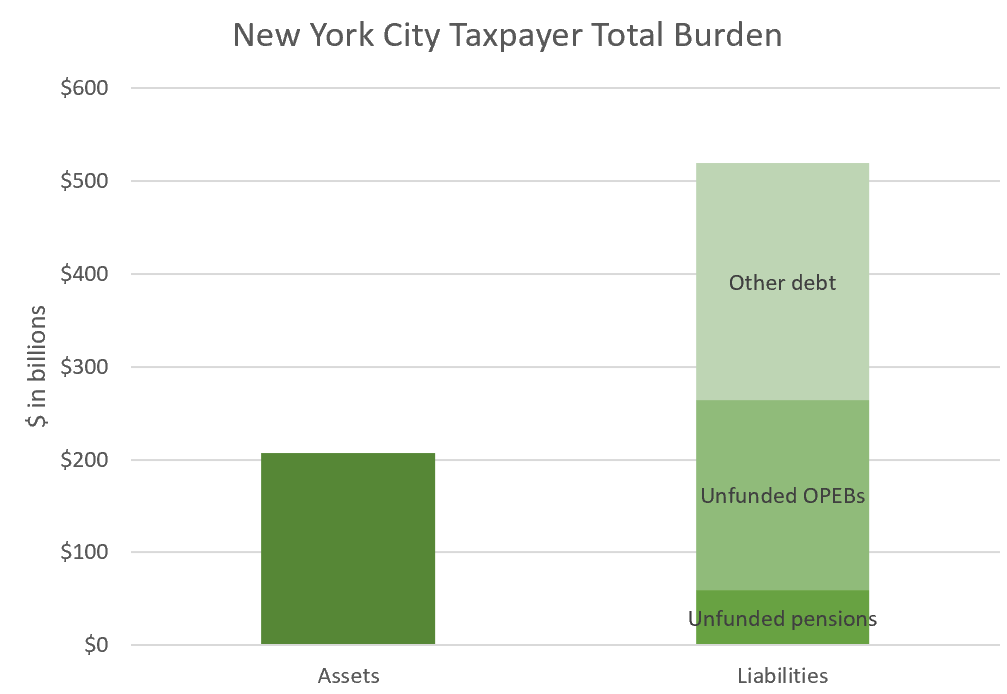

NPPC, I recommend you think through what will actually inform and protect your members. The TIA folks are not distorting the message, except to the extent that state and local governments are undervaluing their pension and OPEB promises.

Complaining about TIA will not make the pensions better-funded. Complaining about TIA will not prevent the worst-funded pensions from running out of assets, which will not be supportable as pay-as-you-go, as the asset death spiral before that will show that the cash flows were unaffordable for the local tax base.

And don’t look to the federal government to save your hash. So far bailout amounts have been puny compared to the size of the promises.

A proposed mandate to shutter the $5 billion Prairie State coal energy campus and a Springfield, Illinois? plant by 2035 would hit local ratepayers with the double burden of funding new energy sources while still paying down project bonds, a bipartisan group of state lawmakers warn.

Gov. J.B. Pritzker backs a state mandate to end coal generation by 2035 to meet de-carbonation targets included in pending energy legislation. The package stalled during the General Assembly?s spring session that ended last week, but Pritzker said he expects lawmakers will return in the coming weeks for a vote.

…..

Retiring Prairie State early would mark the latest headache for some of the nine public utilities in Illinois, Indiana, Kentucky, Missouri, and Ohio that issued $4.5 billion of debt, some it under the federal Build America Bond program, to finance their ownership in project.

Peabody Energy Inc. initially sponsored the project in Washington County promoting it as an affordable source of energy with an adjacent mine and a cleaner one given its state-of-the-art technology at the time. Bechtel Power Corp. built it. It initially carried a $2 billion price tag that rose to a $4 billion fixed cost under the 2010 contract with utilities but cost overruns drove the price tag up to $5 billion.

The Chicago Park District pension funding overhaul approved by lawmakers moves the fund off a path to insolvency to a full funding target in 35 years, with bonding authority.

State lawmakers approved the statutory changes laid out in House Bill 0417 on Memorial Day before adjourning their spring session and Gov. J.B. Pritzker is expected to sign it. It puts the district?s contributions on a ramp to an actuarially based payment, shifting from a formula based on a multiplier of employee contributions. The statutory multiplier formula is blamed for the city and state?s underfunded pension quagmires.

“There are number of things here that are really, really good,? Sen. Robert Martwick, D-Chicago, told fellow lawmakers during a recent Senate Pension Committee hearing. Martwick is a co-sponsor of the legislation and also heads the committee.

?This is a measure that puts the district on to a path to full funding over the course of 35 years,” he said. “It is responsible. There is no opposition to it. This is exactly more of what we should be doing.”

The district will ramp up to an actuarially based contribution beginning this year when 25% of the actuarially determined contribution is owed, then half in 2022, and three-quarters in 2023 before full funding is required in 2024. To help keep the fund from sliding backwards during the ramp period the district will deposit an upfront $40 million supplemental contribution.

The 35-year clock will start last December 31 to reach the 100% funded target by 2055.

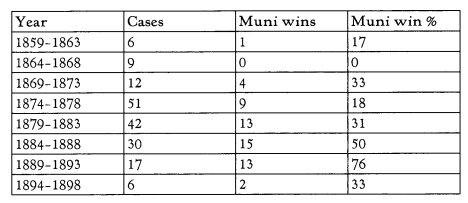

The invocation of ultra vires to escape bond obligations is nothing new, though. In the second half of the nineteenth century, municipal debtors frequently welched on their debts. In the 1850s and 1860s, cities, towns, and counties across the Midwest and West issued bonds to finance the construction of railroads and other infrastructure. Many ultimately defaulted. Rather than simply announce that they couldn’t or wouldn’t pay, however, they often contended that they needn’t pay: for one or another reason, the relevant bonds had been issued ultra vires and so were no obligation of the municipality at all. Litigation in the federal courts was common. Several hundred repudiation disputes made their way to the Supreme Court in the forty years starting 1859.

With an eye to the modern cases, we set out to understand how the Court reckoned with repudiation. We read every one of the 196 cases in which the Justices opined on bond validity (i.e. the enforceability of a bond in the hands of innocent purchasers). In a recently published article, we correct received wisdom about the cases and remark on the logical structure of the Court’s reasoning.

To the extent the municipal bond cases are remembered, modern scholars usually think of them as exemplary instances of a political model of judging. The caricature has the Court siding with bondholders even when the law called on them to rule for the repudiating municipalities. The Justices—or a majority of them—are imagined as staunch political allies of the capitalist class, set against the institutions of state government and their regard for agricultural interests. We find that this picture is inconsistent with reality. In fact, the Court ruled for the repudiating municipality in a third of all the validity cases. As importantly, the Court’s decisions reflected a readily articulable formal logic, a logic the Justices seem, to our eyes, to have applied soundly.

Citation: Buccola, Allison and Buccola, Vincent S.J., The Municipal Bond Cases Revisited (September 25, 2020). 94 American Bankruptcy Law Journal 591 (2020), Available at SSRN: https://ssrn.com/abstract=3699633

Abstract

Recent high-profile attempts to repudiate municipal bonds break from what had become a stable American norm of honoring public debt. In the nineteenth century, though, hundreds of cities, towns, and counties walked away from their bonds. The Supreme Court’s handling of repudiation in the so-called municipal bond cases conjured intense animus at the time. But the years as well as the archaic prose and sheer volume of the opinions have obscured the cases’ significance.

This article reconstructs the bond cases with an eye to modern disputes. It reports the results of our reading all 203 cases, decided 1859–1899, in which the Justices opined on bond validity. At a high level, our findings correct a stock narrative in the literature. The standard account paints the Court as a reliable champion of northeastern capitalists in what resembled regional or class politics more than law. That story does not withstand scrutiny, however. We find, for example, that the Court ruled for the repudiating municipality about a third of the time. Moreover, the decisions had a readily articulable logic at the heart of which lay a familiar law/fact distinction. Estoppel barred issuers in most instances from denying factual predicates of bond validity, but it did not prevent scrutiny of legal predicates. The Justices were willing to hold bonds void on even highly technical legal grounds.

Author(s): Allison Buccola (Independent) and Vince Buccola (Assistant Professor, The Wharton School)

Publication Date: 1 June 2021

Publication Site: Harvard Law School, Bankruptcy Roundtable