Link: https://crr.bc.edu/wp-content/uploads/2021/04/IB-21-8.pdf

Graphic:

Excerpt:

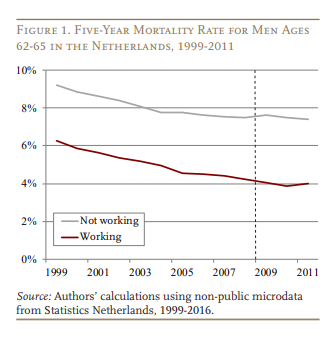

As expected, the raw data show that Dutch men who worked at ages 62-65 were less likely to die over the subsequent five years than men who were not working (see Figure 1). Importantly, Figure 1 shows that mortality decreased at nearly identical rates for working and non-working men between 1999 and 2008, before the policy became available. The fact that these trends are parallel provides more confidence in the policy experiment, indicating that whatever was happening to working men prior to the DWB was also happening to non-working men. In contrast, the mortality rate in 2009-2011 continued to improve somewhat for working men, who were benefiting from the DWB, while the mortality rate for non-working men plateaued.

Author(s): Alice Zulkarnain, Matthew S. Rutledge

Publication Date: May 2021

Publication Site: Center for Retirement Research at Boston College