Graphic:

Excerpt:

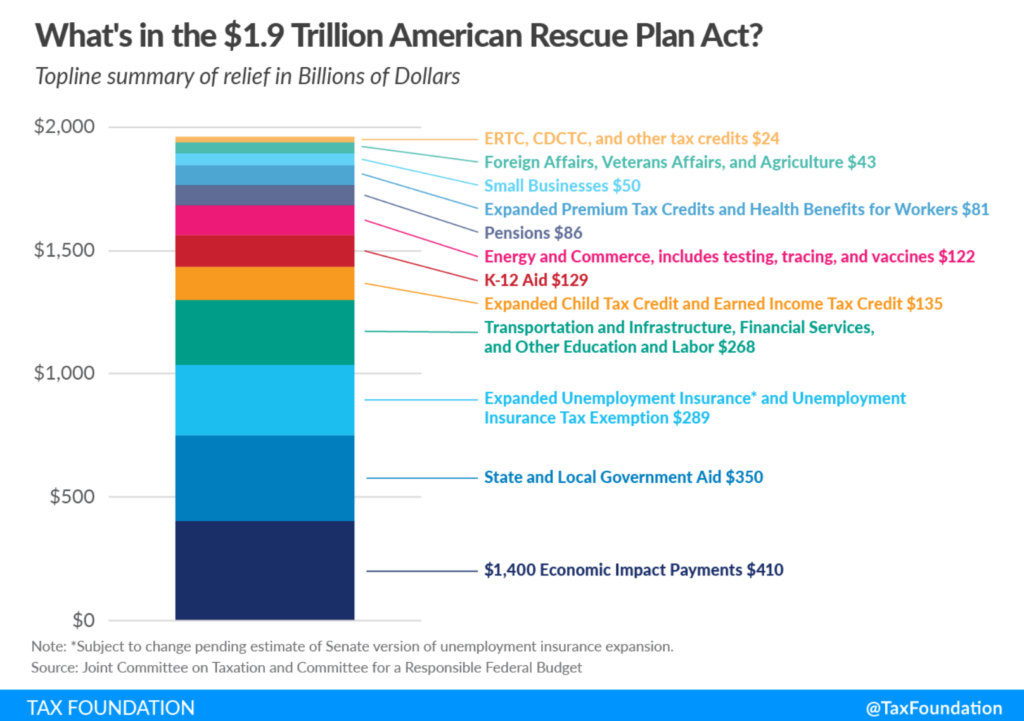

The United States has provided about $6 trillion in total economic relief to the American people during the coronavirus pandemic, including the $1.9 trillion that was approved when President Biden signed the American Rescue Plan (ARP) Act into law on Thursday, amounting to about 27 percent of gross domestic product (GDP). Much of the economic relief in the American Rescue Plan is administered through the tax code in the form of direct payments (stimulus checks) and expanded Child Tax Credit (CTC) in 2021. The size and method of relief will revive debates over the proper role of spending in the tax code and whether the temporary benefits should become permanent after the economy has recovered.

Policymakers will need to determine if the tax code is the proper vehicle to disburse such cash benefits and if the IRS can handle the additional responsibilities. Over the course of many years, the IRS has been tasked with an ever-growing list of administrative duties that go well beyond simple revenue collection—everything from poverty alleviation to education, housing, and health-care benefits. The American Rescue Plan, in addition to other pandemic response measures, would now require the IRS to administer additional benefits on a recurring monthly basis, much as a traditional spending agency, all while processing upwards of 160 million tax returns.

Author(s): Erica York, Garrett Watson

Publication Date: 12 March 2021

Publication Site: Tax Foundation